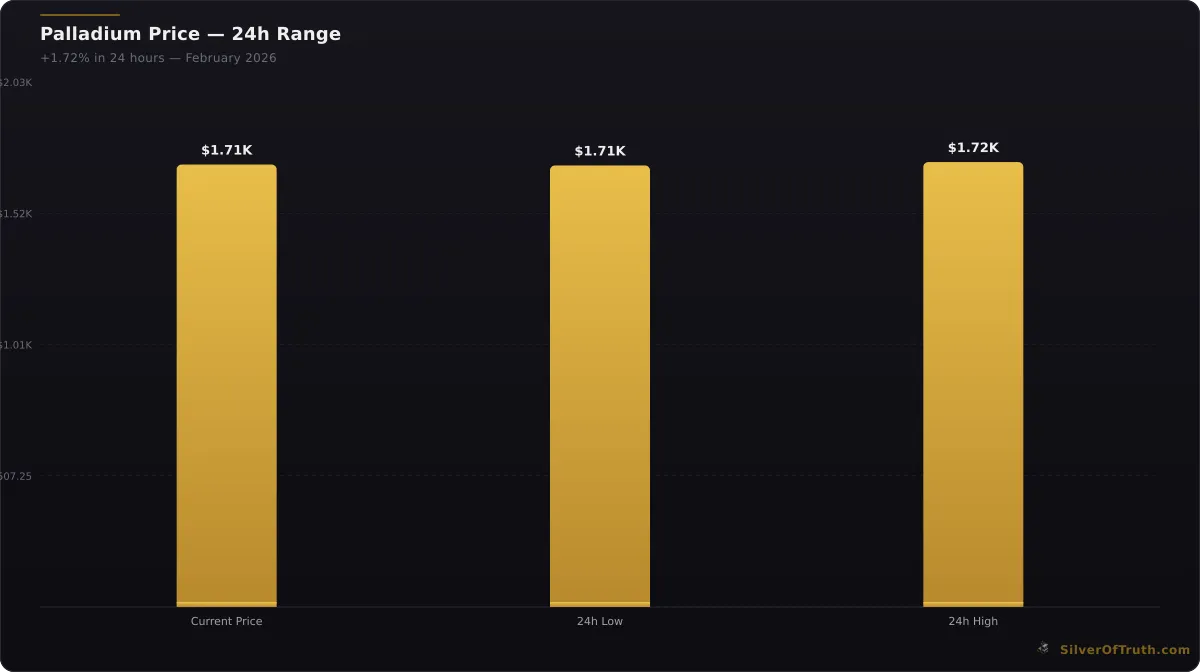

Rising trade tensions across critical supply corridors have pushed palladium 1.72% higher to $1,710 per ounce, signaling market awareness of potential supply disruptions. Unlike previous rallies driven by automotive demand or EV sector dynamics, this surge reflects growing concern over geopolitical risks threatening palladium's concentrated production base in Russia and South Africa.

The metal's reaction to trade uncertainty reveals deeper structural vulnerabilities in global precious metals supply chains. With palladium's unique industrial applications making it less substitutable than other metals, investors are recognizing its potential as both a hedge against supply disruption and a diversification tool within precious metals portfolios.

Trade Tensions Reshaping Palladium Dynamics

Current trade tensions affecting palladium extend beyond traditional tariff disputes to encompass sanctions, shipping route disruptions, and strategic resource controls. Russia produces approximately 40% of global palladium supply, while South Africa contributes another 37%. This concentration creates vulnerability when geopolitical conflicts threaten either region's export capacity.

Recent developments suggest escalating friction between major economic blocs, with potential implications for commodity flows. Understanding how mining sector hurdles impact production becomes crucial as investors assess supply security. Unlike gold or silver with more distributed production, palladium's geographic concentration amplifies trade tension impacts.

The metal's 1.72% daily gain to $1,710 represents market participants pricing in higher probability of supply constraints. This differs markedly from demand-driven rallies, where automotive sector growth or industrial expansion drives prices. Instead, current dynamics reflect risk premium expansion as traders hedge against potential production or shipping disruptions.

According to data from the London Bullion Market Association, palladium inventories in major trading hubs remain relatively tight, providing limited buffer against supply shocks. This inventory structure creates additional sensitivity to trade-related supply concerns.

Supply Chain Vulnerability Analysis

Palladium's supply chain faces multiple choke points that trade tensions could exploit. Primary production concentrates in regions experiencing varying degrees of political instability or international sanctions. Secondary supply from recycling provides some cushion but typically accounts for only 25-30% of annual demand.

Global market shifts affecting palladium and copper demonstrate how interconnected modern commodity markets have become. Trade disruptions in one region cascade through global supply networks, affecting pricing and availability worldwide.

Mining operations in both Russia and South Africa face infrastructure challenges that trade tensions could exacerbate. Transportation bottlenecks, financial system restrictions, and technology access limitations all create potential pressure points. The automotive industry's just-in-time manufacturing approach leaves little room for supply interruptions, potentially amplifying price volatility during disruption periods.

Processing and refining capabilities add another layer of complexity. Even if raw materials remain available, restrictions on processing technology or intermediate products could constrain finished palladium supply. This multi-stage vulnerability explains why relatively modest trade friction can generate outsized market reactions.

Diversification Opportunities in Precious Metals

Palladium's trade tension sensitivity creates unique portfolio diversification opportunities within the precious metals complex. While gold serves as traditional safe haven against currency debasement and inflation, palladium offers exposure to supply disruption risks and industrial demand growth.

The metal's correlation with other precious metals varies significantly during stress periods. Gold and silver often move together during monetary uncertainty, but palladium can diverge based on industrial supply factors. This divergence potential makes it valuable for portfolio construction seeking reduced correlation among precious metals holdings.

Investment approaches to palladium diversification include physical metal exposure, mining company equities, and ETF products. Each carries different risk profiles and trade tension sensitivities. Physical metal provides direct commodity exposure but faces storage and liquidity challenges. Mining stock valuation considerations become critical when evaluating equity exposure to palladium producers.

Professional portfolio managers increasingly view palladium as complement rather than substitute for traditional gold and silver allocations. Its industrial demand base provides different fundamental drivers while maintaining precious metals characteristics during broader market stress.

Geopolitical Risk Premium Development

Current palladium pricing incorporates expanding geopolitical risk premium reflecting trade tension escalation. This premium component represents additional value above fundamental supply-demand equilibrium, compensating holders for potential disruption risks.

Risk premium development in commodities typically occurs gradually, then accelerates during crisis periods. Geopolitical tensions and LBMA flows illustrate how market structure responds to political developments. Early premium expansion often provides better risk-adjusted returns than crisis-period investing.

Historical analysis shows palladium risk premiums can persist for extended periods once established. Unlike temporary supply disruptions that resolve relatively quickly, trade tensions create ongoing uncertainty requiring sustained risk compensation. This dynamic supports structural price elevation until tension resolution becomes clear.

Market participants monitor several indicators for risk premium evolution: futures curve steepening, volatility expansion, and inventory draw-down acceleration. Current data suggests premium establishment rather than mature development, potentially indicating further expansion opportunity.

Industrial Demand Resilience Factors

Palladium's industrial applications provide demand floor supporting prices during trade tension periods. Automotive catalytic converters account for approximately 80% of annual consumption, with electronics and dental applications comprising most remaining demand.

Unlike precious metals valued primarily for monetary properties, palladium maintains strong fundamental demand regardless of investment flows. This industrial base creates price support during periods when financial demand might weaken. Trade tensions can actually strengthen this support by constraining supply while demand remains relatively stable.

Substitution possibilities exist but require significant time and investment. Platinum can replace palladium in some applications, but performance differences and existing infrastructure create switching costs. Understanding how platinum advances affect the broader market helps assess competitive dynamics.

Recycling rates for palladium remain relatively low compared to other precious metals, meaning primary supply disruptions cannot be easily offset through secondary sources. This recycling gap amplifies supply constraint impacts when trade tensions affect primary producers.

Market Structure and Trading Implications

Palladium trading occurs across multiple markets with varying exposure to trade tension impacts. London and New York markets dominate price discovery, but regional markets in Asia and Europe can develop premiums during supply stress periods.

Palladium at $1710.00 — up 1.72% in 24h. Source: SilverOfTruth, February 2026

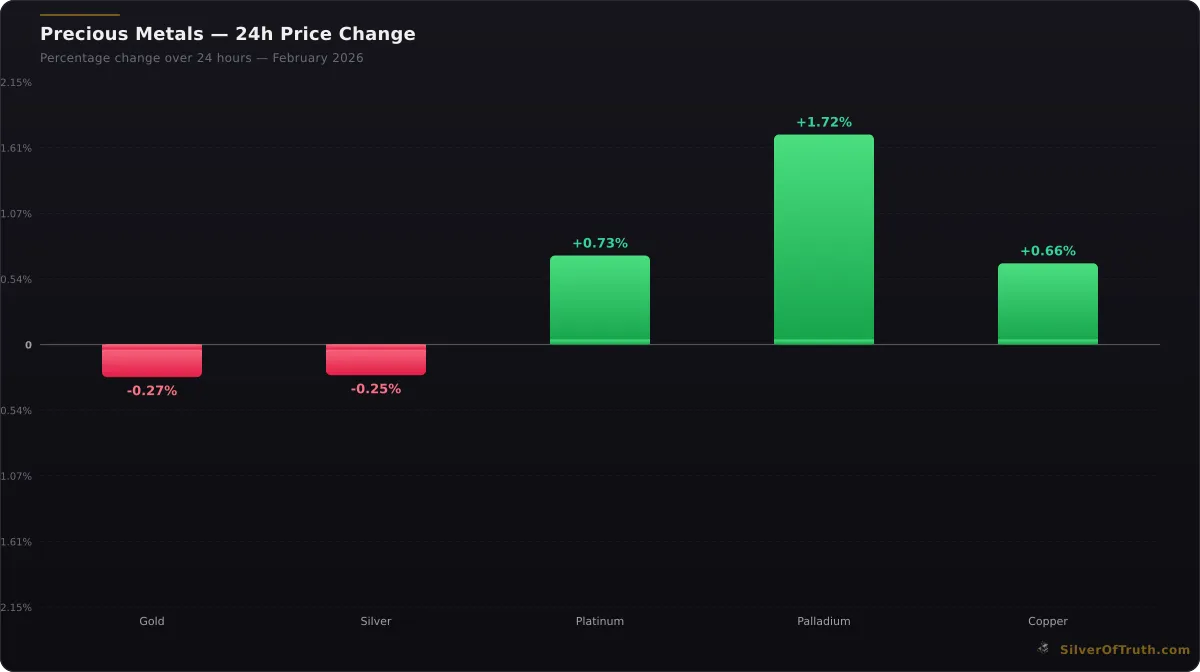

24-hour precious metals price changes. Source: SilverOfTruth, February 2026

Futures markets provide price hedging mechanisms but can experience basis expansion during physical supply concerns. Current futures curves show modest backwardation, suggesting some supply tightness expectations already incorporated in pricing structure.

Exchange-traded products have grown significantly, providing accessible palladium exposure for portfolio diversification. These products typically hold physical metal or futures contracts, creating different risk profiles during supply disruptions. Physical-backed products offer more direct commodity exposure but may face redemption constraints during extreme stress.

Professional traders monitor inventory levels at major depositories as leading indicators of supply stress. According to CME Group data, palladium inventories remain well below historical peaks, providing limited buffer against supply disruptions.

Central Bank and Institutional Perspectives

Central banks maintain minimal palladium reserves compared to gold holdings, but some institutional investors have increased allocations recognizing diversification benefits. Unlike gold's monetary role, palladium appeals primarily for industrial hedge characteristics.

Institutional adoption has accelerated as portfolio managers seek uncorrelated assets within commodity allocations. Palladium's industrial demand base and concentrated supply structure offer different risk-return characteristics compared to traditional precious metals holdings.

Sovereign wealth funds and pension plans increasingly view palladium as strategic resource hedge, particularly for nations heavily dependent on automotive manufacturing. This institutional demand provides additional price support during trade tension periods.

Investment grade palladium products have expanded availability, making institutional allocation more practical. Physical storage solutions and delivery mechanisms have improved, reducing operational barriers to significant holdings.

Portfolio Construction Considerations

Integrating palladium into precious metals portfolios requires understanding its unique characteristics versus traditional gold and silver allocations. The metal's industrial demand base creates different sensitivity patterns to economic cycles and geopolitical events.

Allocation sizing typically ranges from 5-15% of precious metals holdings, depending on risk tolerance and diversification objectives. Higher allocations increase portfolio volatility but provide greater trade tension hedge potential. When to buy silver vs gold principles apply similarly to palladium allocation decisions.

Correlation analysis shows palladium relationships with other assets vary significantly across different market regimes. During normal periods, industrial metal correlations dominate, but stress periods reveal precious metals characteristics. This regime-dependent behavior requires dynamic allocation approaches.

Tax considerations affect palladium investment structures in many jurisdictions. Physical metal holdings may receive different treatment compared to futures or ETF exposure. Professional tax advice becomes essential for significant allocations.

Risk Management and Monitoring Framework

Effective palladium investment requires robust risk management given the metal's volatility and supply concentration risks. Position sizing, stop-loss levels, and correlation monitoring form essential components of disciplined approaches.

Trade tension monitoring involves tracking geopolitical developments, sanctions implementation, and shipping route disruptions. How global economic shifts influence market dynamics provides framework for systematic assessment.

Supply chain analysis requires ongoing attention to mining operations, processing capacity, and transportation infrastructure in key producing regions. Early warning indicators include production guidance changes, infrastructure investment announcements, and regulatory developments.

Market structure evolution affects palladium trading and investment access. New products, regulatory changes, and institutional adoption patterns create both opportunities and risks requiring active monitoring.

Future Market Development Outlook

Palladium markets face several structural changes potentially affecting long-term investment attractiveness. Electric vehicle adoption could reduce automotive demand over time, but current internal combustion engine production maintains strong consumption levels.

Technology developments in catalytic converter efficiency and recycling recovery rates could affect supply-demand balance. However, these changes typically occur gradually, providing time for market adjustment and investment strategy evolution.

Geopolitical landscape evolution will heavily influence palladium investment appeal. Escalating trade tensions support continued risk premium expansion, while resolution could trigger significant price adjustments. Understanding precious metals performance during various scenarios helps prepare for different outcomes.

New supply sources under development could eventually reduce geographic concentration, but timeline uncertainty and development risks maintain current supply structure vulnerabilities for several years.

Frequently Asked Questions

Q: How does palladium's trade tension sensitivity compare to other precious metals? A: Palladium shows higher sensitivity due to concentrated production in Russia and South Africa, unlike gold and silver with more distributed mining. Trade disruptions can directly impact 75% of global supply from just two countries.

Q: What percentage of a precious metals portfolio should include palladium for diversification? A: Most portfolio managers recommend 5-15% allocation within precious metals holdings, depending on risk tolerance and trade tension hedge objectives. Higher allocations increase volatility but provide greater supply disruption protection.

Q: Can palladium maintain industrial demand if trade tensions escalate? A: Yes, automotive catalytic converter demand remains relatively stable during trade tensions since vehicle production continues. However, supply constraints could force price increases or accelerate substitution research.

Q: How do investors access palladium exposure for portfolio diversification? A: Options include physical metal purchase, ETFs holding palladium, mining company stocks, and futures contracts. Each approach offers different risk profiles, liquidity characteristics, and tax implications.

Q: What early warning signs indicate palladium supply disruptions from trade tensions? A: Key indicators include futures curve steepening, inventory drawdowns at major depositories, shipping route closures, and sanctions announcements affecting major producing countries.

Track palladium's trade tension dynamics and supply chain risks with real-time data in the SilverOfTruth app, available on the App Store. Monitor geopolitical developments, inventory levels, and pricing premiums in one comprehensive precious metals command center.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, investment, or trading advice. Past performance is not indicative of future results. Always conduct your own research and consult with a qualified financial advisor before making investment decisions. SilverOfTruth provides market data and analysis tools. It does not provide personalized financial advice.