Gold as an inflation hedge represents one of the most enduring investment narratives in modern finance, yet the relationship between gold prices and inflation proves far more complex than conventional wisdom suggests. With gold trading at $5,063.80 as of February 2026, investors face critical questions about whether the yellow metal truly protects purchasing power during inflationary periods.

This comprehensive analysis examines decades of data to determine when gold functions as an effective inflation hedge, when it fails spectacularly, and what factors drive these divergent outcomes. Understanding these dynamics becomes essential as central banks navigate monetary policy shifts and investors seek protection against currency debasement.

Understanding Inflation and Real Returns

Inflation erodes the purchasing power of currency over time, making assets that maintain or increase their value relative to rising prices particularly valuable. A true inflation hedge should deliver returns that match or exceed the inflation rate, preserving real wealth rather than merely nominal gains.

The challenge lies in measuring inflation accurately and understanding different inflationary environments. The Consumer Price Index (CPI), tracked by the Bureau of Labor Statistics, represents the most commonly referenced inflation measure, though critics argue it understates true price increases through substitution effects and hedonic adjustments.

Real returns equal nominal returns minus the inflation rate. If gold rises 10% while inflation runs at 8%, the real return equals 2%. However, if gold gains 5% during a 12% inflationary surge, real wealth actually declines by 7% despite positive nominal performance.

Historical analysis reveals that gold's effectiveness as an inflation hedge varies dramatically across different time periods, inflation rates, and underlying economic conditions. The metal performed exceptionally during the stagflationary 1970s but lagged significantly during other inflationary episodes.

Historical Gold Performance During Inflationary Periods

The 1970s: Gold's Inflation Hedge Glory Days

The period from 1970-1980 represents gold's strongest case as an inflation hedge. Gold prices soared from $35 per ounce to over $850, representing a 2,300% nominal gain. Meanwhile, CPI inflation averaged 7.4% annually, with peak rates exceeding 14% in 1979-1980.

During this decade, gold delivered real returns well above inflation, driven by multiple factors: Nixon's 1971 decision to end dollar-gold convertibility, oil price shocks that sparked cost-push inflation, declining confidence in fiat currencies, and geopolitical tensions including the Iran hostage crisis.

The 1970s established gold's reputation as the ultimate inflation hedge, creating expectations that many investors still hold today. However, this exceptional performance occurred during unique circumstances that haven't been replicated since.

The 1980s-1990s: When Gold Failed as Inflation Hedge

Following its 1980 peak, gold entered a prolonged bear market despite continued inflation. From 1980-2000, gold fell from $850 to approximately $280, losing nearly 70% of its nominal value. During the same period, CPI inflation averaged 3.9% annually, meaning gold's real returns were deeply negative.

This two-decade period severely challenged gold's inflation hedge credentials. Rising real interest rates, implemented by Federal Reserve Chairman Paul Volcker to combat inflation, made non-yielding assets like gold less attractive compared to interest-bearing investments. Strong economic growth and technological productivity gains also reduced inflation fears.

The World Gold Council data shows that gold's purchasing power in the late 1990s had fallen below 1970 levels, demonstrating how dramatically the inflation hedge thesis can fail during certain periods.

Post-2000: Mixed Results in Low Inflation Environment

The 21st century has produced mixed results for gold as an inflation hedge. From 2000-2011, gold rose from $280 to over $1,900, outpacing inflation significantly. However, this rally occurred primarily during a low-inflation environment, suggesting factors beyond inflation drove performance.

The 2008 financial crisis highlighted gold's role as a store of value during currency debasement fears, as central banks implemented unprecedented quantitative easing programs. Investors sought gold protection not against current inflation, which remained subdued, but against potential future inflation from monetary expansion.

From 2011-2015, gold declined sharply despite continued QE programs and moderate inflation, once again challenging its hedge effectiveness. The metal's performance seemed more correlated with real interest rates and currency movements than consumer price inflation.

Factors Beyond Inflation That Drive Gold Prices

Real Interest Rates: The Primary Driver

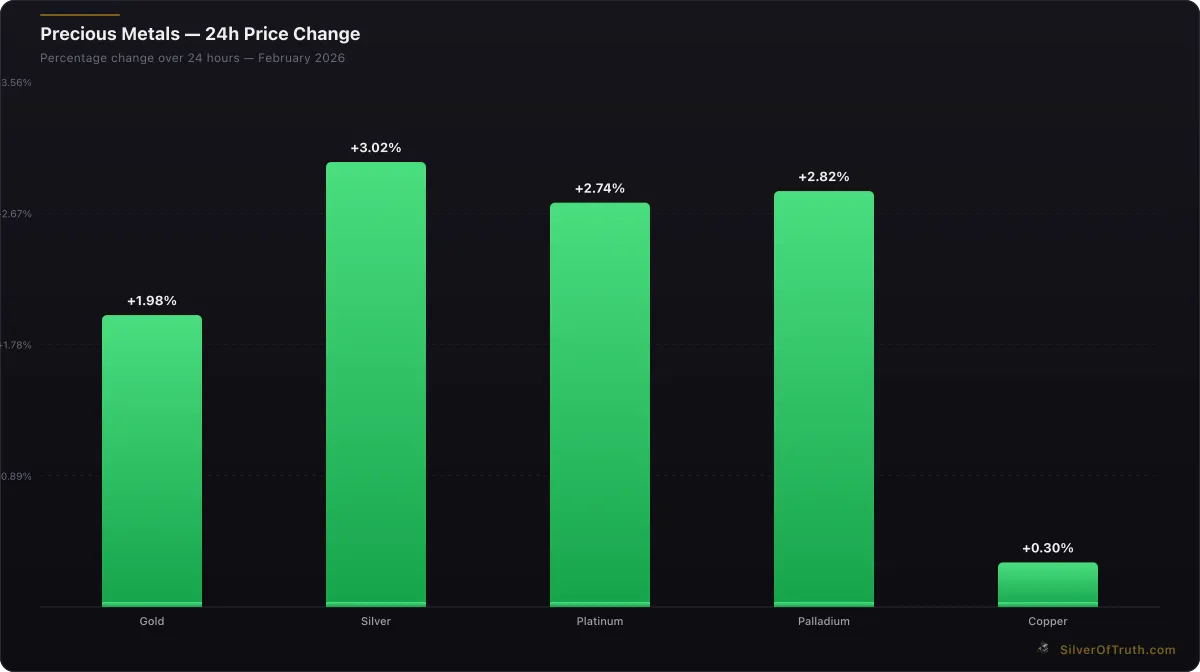

24-hour precious metals price changes. Source: SilverOfTruth, February 2026

Academic research consistently identifies real interest rates as gold's most significant price driver. When real rates (nominal rates minus expected inflation) rise, gold typically falls, as investors can earn positive returns from risk-free assets. When real rates turn negative, gold becomes more attractive as a store of value.

The Federal Reserve's current monetary policy stance influences real rates directly through federal funds rate decisions and indirectly through inflation expectations. Our analysis of COT positioning data shows that commercial traders, who often represent institutional money, frequently position based on real rate expectations rather than simple inflation forecasts.

Current COMEX gold positioning shows commercials holding 286,476 short contracts against 88,738 longs, creating a net short position of 197,738 contracts. This positioning suggests professional traders remain cautious about gold's near-term prospects, potentially reflecting expectations for higher real rates.

Currency Debasement vs. Consumer Price Inflation

Gold often performs better as a hedge against currency debasement than consumer price inflation. Currency debasement occurs when governments expand money supply faster than economic growth, potentially leading to future inflation even if current prices remain stable.

The distinction proves crucial for investors. During 2020-2021, massive fiscal and monetary stimulus created currency debasement concerns while consumer prices initially remained subdued due to economic disruption. Gold rallied significantly during this period, anticipating rather than responding to inflation.

Understanding this difference helps explain why gold sometimes moves independently of CPI readings. Investors purchasing gold as an inflation hedge may actually be seeking protection against monetary policy excess rather than current price increases.

Geopolitical Risk and Safe Haven Demand

Geopolitical tensions often drive gold demand independently of inflation concerns. During periods of international uncertainty, investors seek safe-haven assets regardless of inflation rates. The metal's performance during various crises—from the Cuban Missile Crisis to recent tensions with China—demonstrates this dynamic.

Current geopolitical factors including BRICS nations' gold accumulation and potential de-dollarization trends create additional demand drivers beyond traditional inflation hedging. Central banks' record gold purchases in recent years reflect these broader monetary system concerns.

Gold vs. Alternative Inflation Hedges

Treasury Inflation-Protected Securities (TIPS)

TIPS provide direct inflation protection by adjusting principal value based on CPI changes. Unlike gold, TIPS offer guaranteed real returns (assuming no default risk) and pay interest. However, TIPS face interest rate risk and provide no protection against currency debasement beyond measured inflation.

Historical comparison shows TIPS generally provide steadier inflation protection than gold, though with lower upside potential during extreme inflationary episodes. For conservative investors seeking inflation protection without volatility, TIPS often represent a superior choice.

Real Estate and Commodities

Real estate historically provides strong inflation protection through rent adjustments and property value appreciation. Unlike gold, real estate generates income and benefits from leverage during inflationary periods. However, real estate requires significant capital, involves transaction costs, and faces regional market risks.

Broad commodity indices often provide better inflation correlation than gold alone, as they include energy and agricultural products that directly impact consumer prices. However, individual commodities face supply-demand disruptions that can overwhelm inflation trends.

Stocks: The Unexpected Inflation Hedge

High-quality stocks with pricing power often provide superior long-term inflation protection compared to gold. Companies can raise prices to maintain margins and typically grow earnings faster than inflation over extended periods. Dividend-paying stocks offer income that can increase with inflation.

However, stocks face valuation risks during inflationary periods if investors demand higher real returns. The 1970s demonstrated how stocks can struggle during stagflationary environments, though this primarily affected growth stocks without pricing power.

Our comparison of gold versus stocks provides detailed analysis of relative performance across different economic environments, showing how each asset class responds to various inflation scenarios.

Modern Monetary Theory and Gold's Evolving Role

Quantitative Easing and Asset Price Inflation

Post-2008 monetary policy introduced new dynamics for gold as an inflation hedge. Quantitative easing programs created asset price inflation while consumer price inflation remained subdued, leading to a disconnect between traditional inflation measures and currency purchasing power.

Gold's performance during various QE phases suggests the metal responds more to monetary policy extremes than measured consumer price inflation. This evolution requires investors to reconsider what "inflation" means in modern financial markets.

Central Bank Digital Currencies (CBDCs)

Emerging CBDC development could influence gold's inflation hedge characteristics. CBDCs provide governments with enhanced monetary control and surveillance capabilities, potentially making physical assets like gold more valuable for privacy-conscious investors.

However, CBDCs also enable more precise monetary policy implementation, potentially reducing inflation volatility and changing gold's demand dynamics. The relationship between digital currencies and precious metals remains evolving and speculative.

Building a Gold Allocation Strategy

Position Sizing for Inflation Protection

Academic research suggests 5-10% gold allocation provides meaningful diversification benefits without excessive volatility drag on portfolio returns. Higher allocations may be justified during periods of extreme monetary policy or geopolitical uncertainty.

Position sizing should consider individual circumstances, including inflation exposure, income sources, and overall portfolio construction. Fixed-income heavy portfolios may benefit from higher gold allocations than equity-heavy portfolios that already provide some inflation protection.

Timing Considerations

Gold's inflation hedge effectiveness varies significantly across time periods, making timing crucial for optimal results. Systematic approaches based on real interest rates, monetary policy stance, and valuation metrics often outperform fixed allocation strategies.

Current market conditions, with COMEX gold inventory at 34.4 million ounces and registered coverage ratios at medium risk levels, suggest adequate supply to meet demand without immediate shortage concerns. This inventory backdrop provides context for position timing decisions.

Physical vs. Paper Gold Considerations

The choice between physical and paper gold exposure affects inflation hedge effectiveness. Physical gold provides direct purchasing power protection but involves storage costs and liquidity challenges. Paper gold through ETFs offers convenience but introduces counterparty risk.

During extreme inflationary scenarios, physical ownership may prove superior due to potential settlement failures or government intervention in paper markets. However, for moderate inflation protection, liquid gold ETFs often provide adequate hedge characteristics with lower transaction costs.

Common Mistakes in Gold Inflation Hedging

Expecting Perfect Correlation

Many investors expect gold prices to track inflation precisely, leading to disappointment during periods of divergent performance. Gold's inflation hedge characteristics emerge over longer time periods and during specific economic conditions rather than providing consistent monthly or yearly correlation.

Understanding gold's cyclical nature and multiple demand drivers helps establish realistic expectations for inflation protection performance. The metal functions better as a long-term purchasing power store than a short-term inflation tracker.

Ignoring Opportunity Cost

Gold produces no income, creating opportunity cost relative to yielding assets. During periods of positive real interest rates, this opportunity cost can outweigh inflation protection benefits. Effective gold allocation strategies consider prevailing yield alternatives.

Current market conditions with elevated yields on risk-free assets increase gold's opportunity cost, requiring stronger inflation expectations to justify significant allocations. This dynamic affects optimal allocation sizing and timing decisions.

Confusing Nominal and Real Returns

Focusing exclusively on nominal gold price appreciation ignores inflation's erosive effect on purchasing power. Real return analysis provides better insight into gold's inflation hedge effectiveness and portfolio contribution.

Historical periods of strong nominal gold performance sometimes coincided with even stronger inflation, resulting in negative real returns despite positive price appreciation. This distinction proves crucial for proper hedge evaluation.

Future Outlook for Gold as Inflation Hedge

Structural Inflation Drivers

Several structural factors could influence future inflation trends and gold's hedge effectiveness. Deglobalization, aging demographics, climate change costs, and infrastructure investment needs suggest potentially higher structural inflation than experienced in recent decades.

These long-term trends could create more favorable conditions for gold as an inflation hedge, similar to the 1970s environment that established the metal's reputation. However, technological productivity gains and demographic trends in developed economies provide counterbalancing deflationary forces.

Central Bank Policy Evolution

Central bank policy frameworks continue evolving, with greater emphasis on employment alongside price stability. Average inflation targeting allows temporary overshoots, potentially creating conditions more favorable for gold's inflation hedge characteristics.

However, improved central bank credibility and communication compared to the 1970s may reduce inflation expectations and gold's role as a monetary uncertainty hedge. The balance between policy flexibility and price stability credibility will influence gold's future hedge effectiveness.

Frequently Asked Questions

Does gold always protect against inflation?

No, gold does not consistently protect against inflation. While gold performed exceptionally during the 1970s stagflationary period, it failed as an inflation hedge during the 1980s-1990s despite continued consumer price increases. Gold's effectiveness depends on underlying economic conditions, real interest rates, and the type of inflationary environment.

What allocation to gold provides optimal inflation protection?

Research suggests 5-10% portfolio allocation to gold provides meaningful inflation protection without excessive volatility. However, optimal allocation varies based on individual circumstances, overall portfolio construction, and current market conditions. Higher allocations may be justified during periods of extreme monetary policy or currency debasement concerns.

Is physical gold better than gold ETFs for inflation hedging?

Both physical gold and gold ETFs can provide inflation hedge characteristics, with trade-offs between security and convenience. Physical gold offers direct ownership and protection against counterparty risk but involves storage costs and liquidity challenges. Gold ETFs provide easier access and lower transaction costs but introduce potential settlement risks during extreme market stress.

How does gold compare to TIPS for inflation protection?

TIPS provide more consistent inflation protection with guaranteed real returns (assuming no default), while gold offers higher upside potential during extreme inflationary episodes but greater volatility. TIPS work better for conservative investors seeking steady inflation adjustment, while gold suits those concerned about currency debasement beyond measured inflation.

What economic indicators suggest when gold will be an effective inflation hedge?

Gold typically functions best as an inflation hedge when real interest rates are negative or falling, currency debasement concerns exist, geopolitical tensions rise, and inflation expectations exceed central bank targets. Monitoring Federal Reserve policy, yield curves, money supply growth, and international monetary developments helps assess optimal timing for gold inflation hedge positioning.

Conclusion

Gold's reputation as an inflation hedge rests primarily on its exceptional 1970s performance, yet historical analysis reveals a far more complex relationship between gold prices and inflation. The metal functions effectively as an inflation hedge under specific conditions—particularly when real interest rates are negative, currency debasement concerns exist, and geopolitical uncertainty rises.

However, gold has failed spectacularly as an inflation hedge during various periods, most notably the 1980s-1990s when the metal lost 70% of its value despite continued consumer price inflation. This inconsistent performance requires investors to understand the nuanced factors driving gold's inflation hedge characteristics rather than assuming automatic protection.

Modern investors benefit from viewing gold as one component of a diversified inflation protection strategy rather than a standalone solution. The metal's role continues evolving as monetary policy frameworks change and new inflation dynamics emerge from deglobalization and technological disruption.

For those considering gold allocation, the SilverOfTruth app provides real-time COMEX inventory tracking and COT analysis to help time precious metals positions effectively. Available on the App Store, the platform offers institutional-grade data for making informed precious metals investment decisions.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, investment, or trading advice. Past performance is not indicative of future results. Always conduct your own research and consult with a qualified financial advisor before making investment decisions. SilverOfTruth provides market data and analysis tools — it does not provide personalized financial advice.