The BRICS nations—Brazil, Russia, India, China, and South Africa—have been quietly accumulating gold reserves at unprecedented rates while simultaneously reducing their dependence on US dollar-denominated assets. With gold trading at $5,063.80 as of February 2026, these strategic moves have intensified speculation about a potential BRICS gold standard or gold-backed currency that could fundamentally reshape the global monetary system.

This comprehensive analysis examines the evidence behind BRICS gold accumulation, the mechanics of implementing a gold-backed currency, and what such a development would mean for precious metals investors and the broader financial system.

Understanding BRICS Gold Accumulation Patterns

The BRICS coalition has been systematically increasing gold reserves for over a decade, with particularly aggressive buying since 2020. According to the World Gold Council, central banks purchased over 1,100 tonnes of gold in 2022 alone, with BRICS nations accounting for approximately 70% of these purchases.

Source: SilverOfTruth COMEX data, February 2026

China leads the pack with officially reported reserves exceeding 2,100 tonnes, though many analysts believe actual holdings could be substantially higher due to state-controlled mining production and unreported purchases. Russia maintained approximately 2,300 tonnes before sanctions, while India holds over 750 tonnes. Brazil and South Africa, despite being gold producers, have maintained more modest official reserves of around 130 and 125 tonnes respectively.

The timing of these purchases coincides with increasing tensions in the global monetary system, including sanctions on Russia, concerns about US debt sustainability, and growing calls for alternatives to dollar-based trade settlement. As our analysis of physical vs paper silver demonstrates, the distinction between physical ownership and paper claims becomes crucial during monetary transitions.

Historical Context of Gold Accumulation

The current BRICS gold buying spree mirrors patterns seen before major monetary system changes. Prior to the breakdown of the Bretton Woods system in 1971, France famously demanded physical gold from the US Treasury, recognizing the unsustainability of dollar convertibility. Similarly, BRICS nations appear to be positioning for potential monetary system instability by securing hard assets.

This strategy extends beyond mere diversification. By accumulating gold while simultaneously reducing dollar reserves, BRICS countries are creating optionality—the ability to back new monetary arrangements with physical assets rather than promises. The gold/silver ratio analysis shows similar preparation patterns among precious metals investors seeking alternatives to fiat currency exposure.

Mechanics of a BRICS Gold Currency

Creating a gold-backed currency involves complex technical and political challenges that go far beyond simply holding gold reserves. The mechanics would require establishing exchange rates, determining gold backing ratios, creating clearing mechanisms, and managing the practical aspects of international settlement.

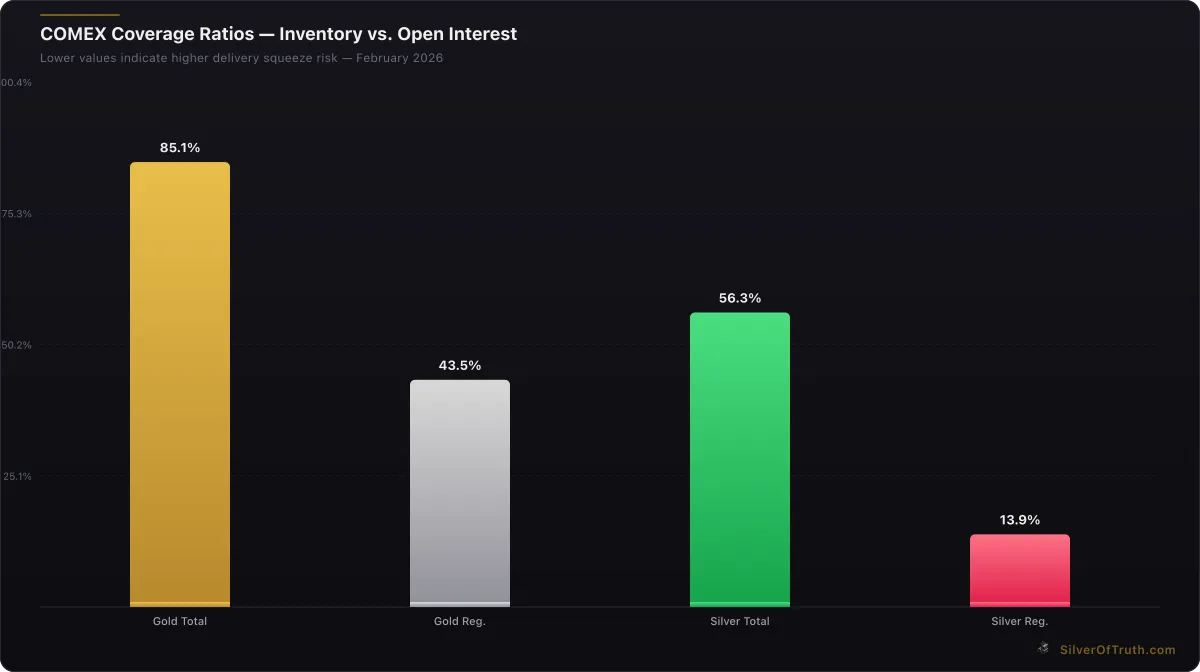

COMEX coverage ratios — lower values indicate higher delivery squeeze risk. Source: SilverOfTruth, February 2026

Exchange Rate Mechanisms

A BRICS gold currency would need to establish fixed or floating exchange rates against member currencies and potentially against gold itself. Historical precedent suggests several approaches: the classical gold standard with fixed convertibility, a gold exchange standard where only central banks convert, or a more flexible system where gold backing provides credibility without strict convertibility.

The choice impacts monetary policy autonomy—fixed convertibility constrains domestic policy but provides maximum credibility, while flexible backing allows policy space but may face credibility questions during stress periods. Given the diverse economic conditions across BRICS nations, a hybrid approach seems most likely.

Reserve Requirements and Backing Ratios

Determining how much gold would back the currency represents another critical decision. Full 100% backing maximizes credibility but severely constrains money supply growth. Partial backing (perhaps 25-40%) provides operational flexibility while maintaining gold anchor credibility.

The current COMEX inventory situation, with registered gold at 17.6 million ounces and a coverage ratio of 43.5%, illustrates the importance of adequate reserves relative to outstanding claims. A BRICS currency would need sufficient gold reserves to maintain credibility even during adverse conditions, as we analyze in our guide to COMEX inventory dynamics.

Settlement Infrastructure

Perhaps the most complex aspect involves creating settlement infrastructure for international trade. This would require:

- Physical gold storage and verification systems

- Digital clearing mechanisms for trade settlement

- Integration with existing SWIFT alternatives like China's CIPS system

- Legal frameworks for dispute resolution

- Standardized gold purity and measurement protocols

The infrastructure investment would be substantial, but BRICS nations have been building these capabilities through institutions like the New Development Bank and various bilateral swap agreements.

Evidence Supporting BRICS Gold Currency Development

Several concrete developments suggest BRICS nations are moving beyond theoretical discussions toward practical implementation of gold-backed trade mechanisms.

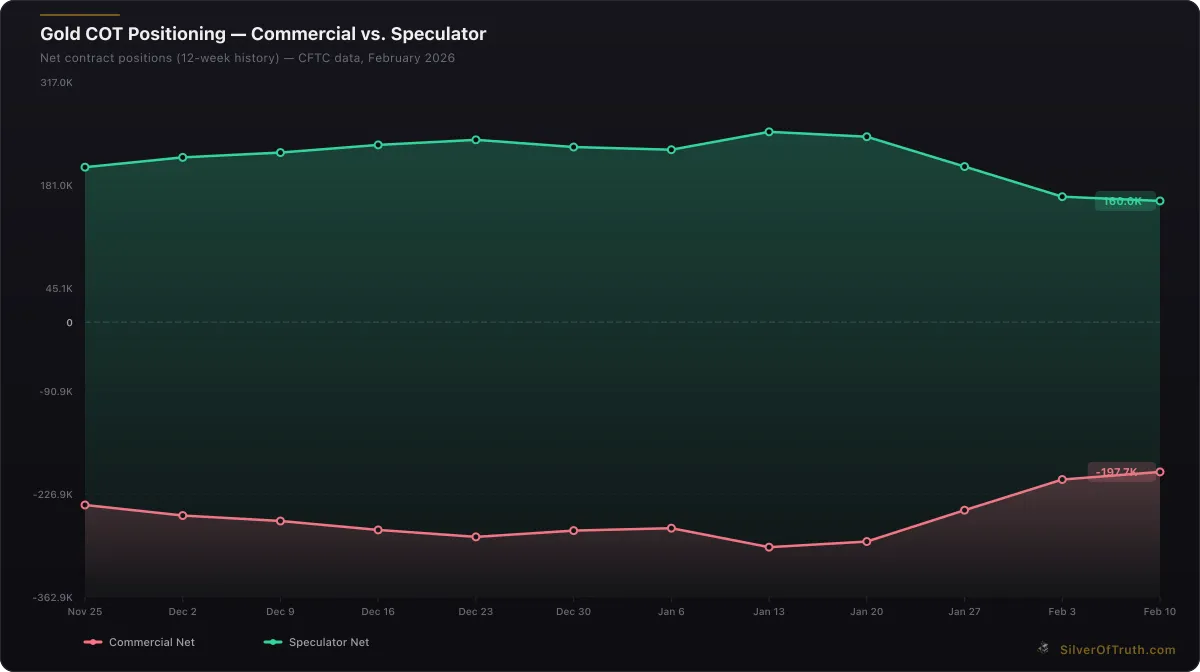

Gold COT positioning: commercial hedgers (red) vs. speculators (green). Source: CFTC via SilverOfTruth, February 2026

Institutional Development

The New Development Bank, established in 2014, has grown its balance sheet to over $30 billion and begun issuing bonds in local currencies rather than dollars. This institution could serve as a prototype for managing a gold-backed currency, having already demonstrated the ability to coordinate monetary policy across diverse economies.

Recent BRICS summits have included explicit discussions of payment systems alternatives, with Russia and China leading initiatives to reduce dollar dependence. The timing correlation between sanctions on Russia and accelerated de-dollarization efforts is not coincidental—geopolitical pressure is accelerating monetary system evolution.

Bilateral Gold Trade Agreements

China and Russia have implemented direct gold trading mechanisms, bypassing dollar settlement for bilateral trade. India has begun accepting gold for oil payments from certain suppliers, while Brazil has explored gold-backed trade finance facilities. These bilateral experiments provide building blocks for broader multilateral arrangements.

The Shanghai Gold Exchange has become the world's largest physical gold trading platform, providing infrastructure that could support broader Asian gold trade settlement. Combined with Russia's gold production capabilities and China's manufacturing exports, the foundation exists for gold-backed trade within the BRICS framework.

Central Bank Policy Coordination

BRICS central banks have increased policy coordination, including currency swap agreements exceeding $240 billion. These swaps provide the operational experience needed to manage a common settlement currency, while reducing immediate dollar dependence for bilateral trade.

The Federal Reserve's interest rate policies have created additional incentives for alternatives, as dollar strength pressures emerging market currencies and debt sustainability.

Challenges to BRICS Gold Standard Implementation

Despite mounting evidence of preparation, significant obstacles remain before any BRICS gold currency becomes operational reality.

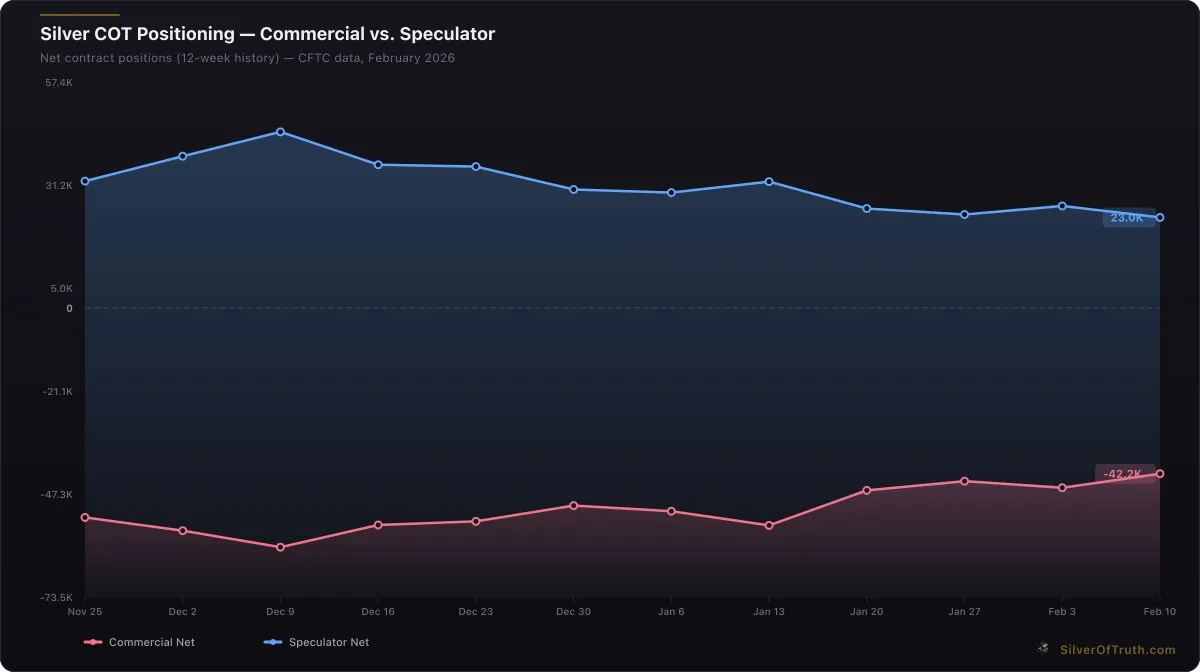

Silver COT positioning: commercial hedgers (red) vs. speculators (blue). Source: CFTC via SilverOfTruth, February 2026

Economic Heterogeneity

BRICS economies operate at vastly different development levels with distinct monetary policy needs. Brazil faces inflation pressures requiring tight policy, while China manages growth slowdown requiring stimulus. Russia deals with sanctions-induced isolation, India balances growth and inflation, and South Africa confronts structural unemployment. Synchronizing monetary policy across such diverse conditions presents enormous challenges.

A gold-backed currency would constrain individual countries' monetary policy flexibility, potentially creating domestic political pressure during economic stress. The eurozone experience demonstrates how shared currency without fiscal integration can create instability during asymmetric shocks.

Technical Implementation Barriers

Creating a gold-backed currency requires resolving numerous technical issues:

- Gold purity and measurement standards: Different national standards would need harmonization

- Storage and transportation: Physical gold movement for settlement creates logistical complexity

- Digital verification: Blockchain or similar technology would need development for trade settlement

- Legal frameworks: International law governing the currency would require extensive negotiation

The complexity mirrors challenges facing the mining sector's evaluation methodologies, where standardizing metrics across jurisdictions remains difficult despite decades of effort.

Geopolitical Resistance

A BRICS gold currency would directly challenge US dollar hegemony, likely triggering substantial resistance from dollar-dependent institutions and countries. This could include:

- Enhanced sanctions on participating countries

- Exclusion from dollar-based clearing systems

- Trade restrictions on gold and related commodities

- Diplomatic pressure on smaller countries considering adoption

The response magnitude would depend on adoption scope and timeline, but historical precedent suggests significant pushback against challenges to reserve currency status.

Market Implications for Precious Metals

The emergence of a BRICS gold currency would create profound implications for precious metals markets, potentially driving structural changes in demand, pricing mechanisms, and investment flows.

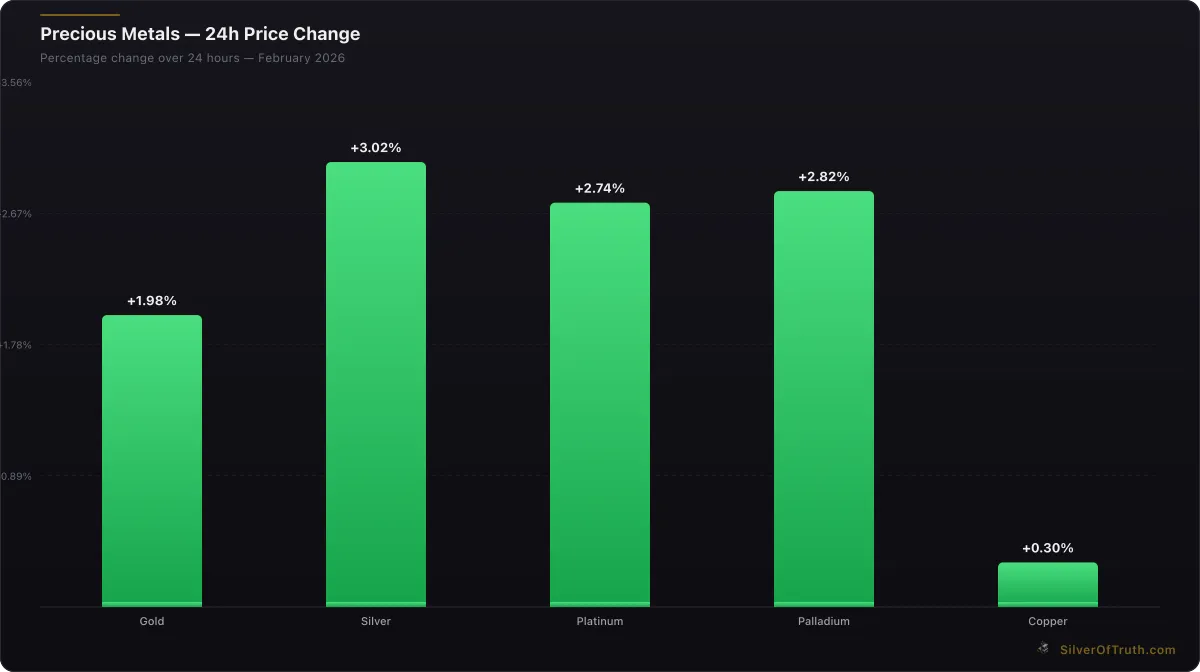

24-hour precious metals price changes. Source: SilverOfTruth, February 2026

Gold Demand Fundamentals

A functioning gold-backed currency would create new structural demand beyond traditional investment and jewelry sectors. Currency backing could require hundreds or thousands of tonnes annually, fundamentally altering supply-demand balance. Current annual mine production of approximately 3,500 tonnes would face competition from monetary demand, potentially creating sustained price pressure.

This demand would be relatively price-inelastic—governments need gold for currency backing regardless of price level, unlike discretionary investment or jewelry demand. The effect would be similar to central bank reserve accumulation but potentially larger and more sustained.

Silver Market Spillover Effects

Silver markets would likely benefit through the traditional gold-silver relationship, though the mechanism might evolve. If a BRICS currency achieved significant adoption, precious metals generally would gain credibility as monetary assets. The current gold-silver ratio at 65.5 suggests silver remains historically undervalued relative to gold, potentially creating opportunity during any broader precious metals re-monetization.

Our silver supply deficit analysis shows industrial demand already straining available supply. Adding monetary demand could create more acute shortages, particularly given silver's smaller market size and limited above-ground stockpiles compared to gold.

Impact on Western Precious Metals Markets

COMEX and LBMA markets could face reduced relevance if Eastern gold trade bypasses Western clearing systems. This might create price discovery fragmentation, with Shanghai prices potentially deviating from London/New York pricing during stress periods.

The current COMEX inventory situation, with silver at high delivery risk and gold at medium risk, could intensify if Eastern demand increases while Western inventory remains constrained. Physical metal availability in Western markets might tighten as more gold flows toward currency backing applications.

Timeline and Probability Assessment

Evaluating the likelihood and timing of BRICS gold currency implementation requires balancing political momentum against technical challenges.

Near-term Developments (2026-2028)

Most likely developments include expanded bilateral gold trade mechanisms, continued central bank gold accumulation, and infrastructure development through existing institutions. Full currency launch appears unlikely during this period due to technical complexity and political coordination requirements.

However, crisis scenarios could accelerate timelines. Major dollar system stress, additional sanctions, or financial market disruption could push BRICS toward faster implementation of alternative arrangements, even if technically suboptimal.

Medium-term Prospects (2028-2032)

This timeframe appears most realistic for limited gold-backed settlement mechanisms, possibly starting with commodity trade between specific country pairs before expanding. Technical infrastructure development and legal framework negotiation would likely occur during this period.

Success of initial implementations would determine broader adoption scope. Positive results might encourage expansion, while technical difficulties or political resistance could delay or modify approaches.

Long-term Structural Change (2032+)

Full-scale BRICS gold currency implementation would likely require this extended timeframe, allowing for infrastructure development, legal framework completion, and gradual transition from current systems.

Even partial implementation could create lasting effects on precious metals markets and global monetary arrangements, regardless of complete success or failure of broader currency ambitions.

Investment Strategy Implications

The possibility of BRICS gold currency development creates several strategic considerations for precious metals investors and portfolio managers.

Physical Precious Metals Allocation

The potential for gold re-monetization argues for maintaining significant physical precious metals allocation, regardless of short-term price volatility. Currency backing demand would be structural rather than cyclical, supporting long-term price trends even during temporary corrections.

Geographic diversification of precious metals storage becomes more important if monetary system fragmentation occurs. Holdings in multiple jurisdictions reduce political risk if currency arrangements create competing monetary blocs with different precious metals access.

Mining Sector Considerations

Gold and silver mining companies could benefit significantly from sustained higher prices driven by currency demand. However, political risk might increase if producing countries prioritize domestic currency needs over export sales.

Companies with diversified geographic operations might prove more resilient than those concentrated in single jurisdictions, as currency arrangements could affect national resource policies.

Portfolio Risk Management

Traditional portfolio diversification assumptions might require revision if monetary system bifurcation occurs. Correlations between assets could change if different regions operate under different monetary arrangements, affecting traditional risk management approaches.

The emergence of competing monetary systems argues for increased allocation to hard assets generally, not limited to precious metals but including real estate, commodities, and other inflation-resistant investments.

Frequently Asked Questions

What is a BRICS gold standard and how would it work?

A BRICS gold standard would be a monetary arrangement where member countries back their currencies or create a new common currency with gold reserves. Unlike historical gold standards with fixed convertibility, a modern version would likely use partial backing (25-40% gold reserves) while maintaining some monetary policy flexibility. Settlement would occur through digital clearing systems backed by physical gold reserves held by participating central banks.

How much gold do BRICS countries currently hold?

BRICS nations collectively hold approximately 5,400 tonnes of official gold reserves, with China at 2,100+ tonnes, Russia at 2,300 tonnes (pre-sanctions), India at 750+ tonnes, and Brazil/South Africa at roughly 125-130 tonnes each. However, actual holdings may be higher due to unreported purchases and state-controlled mining production, particularly in China and Russia.

When could a BRICS gold currency realistically launch?

A limited gold-backed settlement mechanism for bilateral trade could emerge within 5-7 years (2028-2032), while a full-scale currency would likely require 10+ years due to technical complexity and political coordination requirements. Crisis scenarios like major dollar system stress could accelerate these timelines, but sustainable implementation requires substantial infrastructure development and legal framework negotiation.

How would a BRICS gold currency affect gold and silver prices?

Currency backing would create new structural demand for gold, potentially requiring hundreds of tonnes annually beyond current investment and jewelry demand. This relatively price-inelastic demand could create sustained upward pressure on gold prices. Silver would likely benefit through traditional gold-silver correlation and potential inclusion in broader precious metals monetary arrangements, especially given its current supply deficit conditions.

What are the main obstacles to BRICS gold currency implementation?

Primary challenges include economic heterogeneity among member countries requiring different monetary policies, technical complexity of creating gold-backed settlement infrastructure, geopolitical resistance from dollar-dependent institutions, and legal framework negotiation across multiple jurisdictions. The eurozone experience demonstrates how shared currency without fiscal integration can create instability during economic stress periods.

Conclusion

The BRICS gold standard represents one of the most significant potential developments in the global monetary system since the end of Bretton Woods. While technical and political obstacles remain substantial, the consistent pattern of gold accumulation, infrastructure development, and bilateral trading arrangements suggests serious preparation for alternatives to dollar-dominated trade settlement.

For precious metals investors, the implications extend beyond simple price speculation. The potential re-monetization of gold and silver could create structural demand changes that persist regardless of short-term market volatility. Even partial implementation of BRICS gold-backed arrangements would validate precious metals as monetary assets, potentially driving sustained allocation increases across institutional and individual portfolios.

The timeline remains uncertain, with crisis scenarios potentially accelerating development while technical complexity argues for extended implementation periods. However, the direction appears clear: BRICS nations are building capabilities for gold-backed monetary arrangements, creating optionality for future monetary system changes.

Track the latest developments in BRICS gold accumulation and precious metals market dynamics with the SilverOfTruth app — available on the App Store for comprehensive market analysis and portfolio management.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, investment, or trading advice. Past performance is not indicative of future results. Always conduct your own research and consult with a qualified financial advisor before making investment decisions. SilverOfTruth provides market data and analysis tools — it does not provide personalized financial advice.