Central banks worldwide are orchestrating a historic shift away from dollar reserves while simultaneously building their largest gold stockpiles in decades—a dual strategy that challenges the greenback's seven-decade monetary dominance. This de-dollarization movement positions gold as the primary alternative reserve asset, fundamentally reshaping how nations store wealth and conduct international trade. As geopolitical tensions accelerate this trend, understanding the mechanics behind central bank reserve rebalancing and gold's emerging role as a dollar hedge has become essential for investors navigating this unprecedented monetary transition.

De-Dollarization and Gold: Central Banks' Strategic Shift

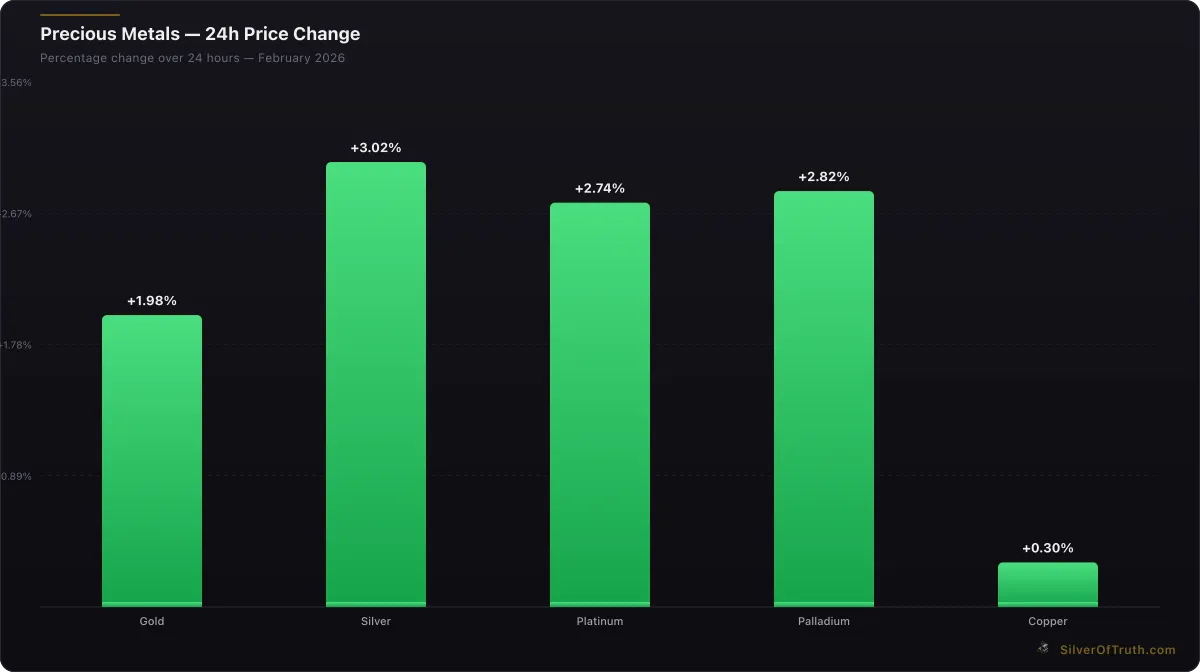

The global monetary landscape faces a seismic shift as de-dollarization gold demand reaches unprecedented levels. With gold trading at $5,063.80 per ounce—up 2.33% in just 24 hours—central banks worldwide are reducing dollar reserves while building the largest gold stockpiles in decades. This fundamental restructuring of global reserve assets signals a profound challenge to the dollar's seven-decade dominance and positions gold as the ultimate dollar alternative.

The acceleration of this trend isn't coincidental. As geopolitical tensions reshape international finance and monetary sovereignty becomes paramount, understanding the de-dollarization movement and gold's pivotal role has never been more critical for investors navigating this historic transition.

Understanding De-Dollarization: Beyond Political Headlines

De-dollarization represents the systematic reduction of U.S. dollar usage in international trade, central bank reserves, and global financial transactions. This process encompasses three primary dimensions: trade settlement diversification, reserve currency rebalancing, and financial infrastructure development outside dollar-dominated systems.

Source: SilverOfTruth COMEX data, February 2026

The movement gained momentum following the 2008 financial crisis, when countries questioned the stability of dollar-centric systems. However, recent geopolitical events have accelerated this trend dramatically. According to the World Gold Council, central bank gold purchases reached 1,136 tonnes in 2022—the highest level since 1967—with emerging market central banks leading the charge.

Traditional dollar alternatives face inherent limitations. The euro carries European political risk and remains vulnerable to regional crises. The Chinese yuan lacks full convertibility and transparency. Cryptocurrency adoption remains limited for sovereign reserves due to volatility and regulatory uncertainty. This reality makes gold's unique properties—no counterparty risk, universal acceptance, and 4,000-year track record—increasingly attractive to central bankers seeking true monetary independence.

The de-dollarization gold connection reflects a fundamental principle: when trust in paper currencies erodes, hard assets become essential. Gold's role transcends simple portfolio diversification; it serves as monetary insurance against currency instability and geopolitical weaponization of finance.

Central Bank Gold Accumulation: The Data Behind the Headlines

Global central bank gold reserves have expanded dramatically over the past decade, with official sector purchases totaling over 4,500 tonnes since 2010. This accumulation pattern reveals strategic intent rather than opportunistic buying.

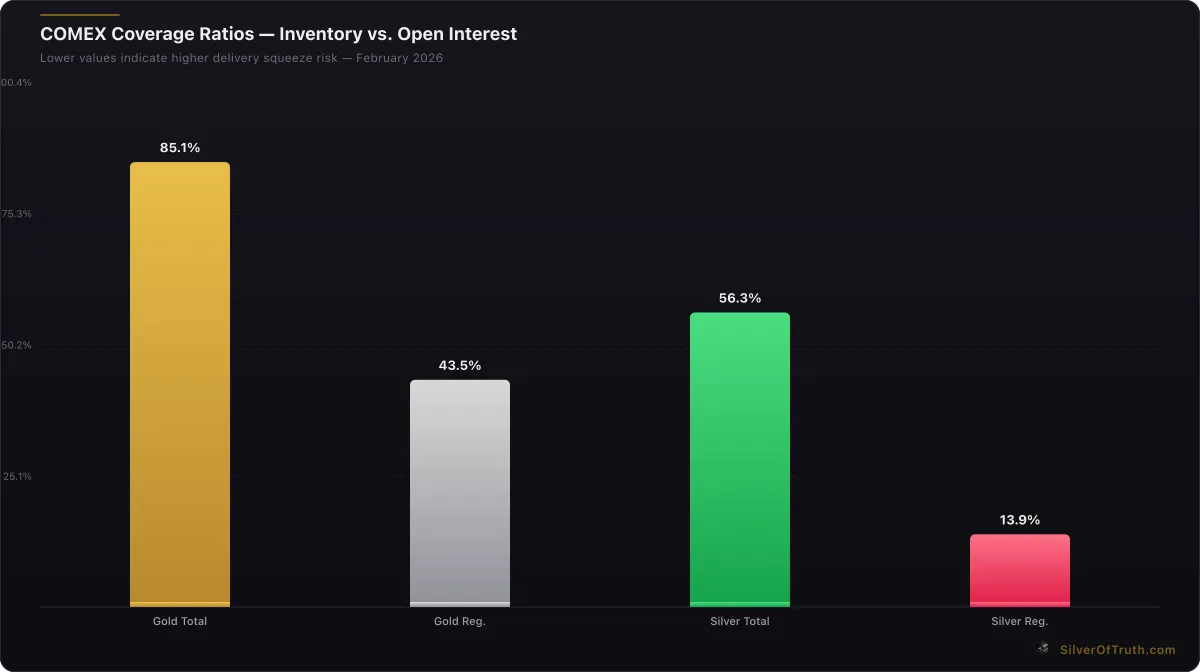

COMEX coverage ratios — lower values indicate higher delivery squeeze risk. Source: SilverOfTruth, February 2026

24-hour precious metals price changes. Source: SilverOfTruth, February 2026

Russia exemplified this strategy before 2022, increasing gold reserves from 600 tonnes to over 2,300 tonnes while simultaneously reducing dollar holdings from 40% to under 10% of total reserves. China's People's Bank has quietly accumulated gold for over a decade, with official holdings exceeding 2,000 tonnes—though many analysts believe actual holdings are significantly higher due to state-controlled purchases through commercial banks.

Turkey's central bank increased gold reserves by 440% between 2017 and 2022, while India, Thailand, and Singapore have all expanded holdings substantially. Even traditional Western allies like Poland have dramatically increased gold allocations, with the National Bank of Poland growing reserves from 103 tonnes to over 250 tonnes.

Regional Patterns in Gold Accumulation

| Region | 2010 Holdings | 2023 Holdings | Increase % | |--------|---------------|---------------|-----------| | Asia-Pacific | 3,847 tonnes | 5,234 tonnes | +36% | | Middle East | 1,156 tonnes | 1,789 tonnes | +55% | | Eastern Europe | 1,423 tonnes | 2,167 tonnes | +52% | | Latin America | 456 tonnes | 623 tonnes | +37% |

This data reveals systematic diversification away from dollar-denominated assets toward gold across multiple regions and political systems. The consistency of this trend across diverse economies suggests fundamental monetary calculations rather than temporary tactical adjustments.

Central bankers cite several factors driving gold accumulation: protection against currency devaluation, hedge against geopolitical risks, diversification from dollar concentration risk, and insurance against financial system disruptions. These motivations align perfectly with de-dollarization objectives.

The BRICS Factor: Coordinated De-Dollarization Strategy

The BRICS nations (Brazil, Russia, India, China, South Africa) have emerged as the coordinated vanguard of de-dollarization efforts, with gold playing a central role in their alternative monetary framework. Combined BRICS gold reserves exceed 4,000 tonnes, representing substantial monetary power outside Western financial systems.

Our comprehensive analysis in BRICS and Gold explores how these nations are building parallel financial infrastructure designed to bypass dollar-dominated systems. The New Development Bank, BRICS payment systems, and bilateral trade agreements increasingly emphasize gold's role as settlement mechanism and reserve asset.

China's Belt and Road Initiative incorporates gold financing elements, while Russia has linked oil and gas sales to gold-backed currencies. India's sovereign gold bonds and Thailand's gold-backed savings certificates demonstrate how governments are institutionalizing gold ownership among citizens—building domestic demand that supports broader de-dollarization objectives.

The expansion of BRICS membership to include Saudi Arabia, UAE, Egypt, Ethiopia, Iran, and Argentina creates a resource-rich bloc controlling significant global oil, gas, and mineral production. These nations increasingly discuss gold-backed trade settlements and reserve arrangements that could fundamentally alter global monetary flows.

BRICS central banks coordinate gold purchases through mechanisms that avoid Western financial systems, including direct bilateral arrangements and Shanghai Gold Exchange transactions. This coordination amplifies individual national policies into a collective challenge to dollar hegemony.

Dollar Dominance Under Pressure: Structural Vulnerabilities

The U.S. dollar's reserve currency status, established at Bretton Woods in 1944, faces unprecedented structural challenges that make de-dollarization gold strategies increasingly rational for central banks worldwide.

Dollar share of global reserves has declined from over 70% in 2000 to approximately 60% today, according to IMF data. This erosion accelerated following the 2008 financial crisis and recent geopolitical weaponization of dollar-based financial systems.

The "exorbitant privilege" of printing the world's reserve currency enabled massive U.S. fiscal deficits without traditional balance of payments constraints. However, this advantage creates vulnerabilities: foreign creditors hold trillions in dollar-denominated debt, creating potential for coordinated selling if confidence erodes.

Federal Reserve monetary policy impacts global liquidity, creating boom-bust cycles in emerging markets dependent on dollar flows. When the Fed tightens, dollar strength can devastate economies holding dollar debt, incentivizing diversification into assets like gold that aren't subject to another nation's monetary policy.

Key Dollar Vulnerability Indicators

Fiscal Position: U.S. federal debt exceeds $33 trillion, requiring continuous foreign financing through bond sales. Any reduction in foreign demand for Treasuries could force higher interest rates and currency instability.

Trade Balance: Persistent current account deficits require continuous capital inflows to maintain dollar stability. As trade partners diversify away from dollar transactions, this financing becomes more challenging.

Political Risk: Financial sanctions and asset freezes have demonstrated how dollar dependence creates vulnerabilities. Even allied nations now question the safety of holding reserves in systems subject to U.S. political decisions.

Inflation History: The dollar has lost over 95% of its purchasing power since 1913, while gold has maintained its value across millennia. Central bankers increasingly recognize this fundamental difference when making generational reserve decisions.

These structural vulnerabilities make gold accumulation a rational insurance policy against dollar instability, regardless of short-term price movements.

Trade Settlement Evolution: From Petrodollars to Gold-Backed Systems

International trade settlement patterns are evolving rapidly as countries develop alternatives to dollar-based payment systems. This transformation directly drives demand for gold as both settlement medium and reserve backing for new monetary arrangements.

The petrodollar system, established in the 1970s, required oil purchases in U.S. dollars, creating artificial dollar demand and supporting American fiscal deficits. However, major oil producers now accept yuan, rubles, and even discuss gold-backed payment systems for energy transactions.

Russia's requirement that "unfriendly nations" pay for gas in rubles represents a direct challenge to dollar hegemony in energy markets. While implementation remains complex, the precedent establishes that major commodity producers can successfully demand payment in their preferred currencies.

China's Cross-Border Interbank Payment System (CIPS) processed over $12 trillion in transactions in 2022, providing an alternative to SWIFT for yuan-denominated trade. As this system expands, gold serves as the ultimate settlement asset for large bilateral transactions between participating nations.

Bilateral trade agreements increasingly incorporate local currency settlements. India-Russia oil transactions, China-Saudi energy deals, and Latin American trade pacts bypass dollar systems entirely. Gold provides the neutral reserve asset that backs these arrangements when direct currency exchanges prove impractical.

Gold in Modern Trade Settlement

Gold's role in contemporary trade settlement differs from the classical gold standard. Rather than fixed exchange rates, gold serves as:

- Neutral Reserve Asset: Neither party controls gold supply, unlike national currencies

- Final Settlement Medium: Ultimate backstop when bilateral currency arrangements face stress

- Value Preservation: Maintains purchasing power across long-term trade relationships

- Political Independence: Cannot be frozen or weaponized by third-party nations

Central banks accumulating gold position their economies to participate in these emerging trade arrangements while maintaining monetary sovereignty.

Technical Analysis: Gold's Performance During Dollar Weakness

Historical analysis reveals strong negative correlation between dollar strength and gold performance, supporting the thesis that systematic dollar decline would benefit gold investments significantly. Current market conditions, with gold at $5,063.80 and showing 2.33% daily gains, reflect this dynamic in real-time.

The Dollar Index (DXY) peaked at over 114 in late 2022 before declining to current levels around 104. During this period, gold advanced from approximately $1,600 to current levels above $5,000—demonstrating the inverse relationship that makes gold an effective dollar alternative.

Technical indicators support continued gold strength as dollar weakness persists. COMEX gold inventory shows registered reserves of 17.58 million ounces against open interest of 404,391 contracts, creating a coverage ratio of 43.5%. This moderate tightness suggests physical demand supports technical price momentum.

Understanding COMEX inventory dynamics reveals how physical demand from central banks and investors translates into futures market stress. As coverage ratios decline, price volatility typically increases, favoring long-term holders over short-term speculators.

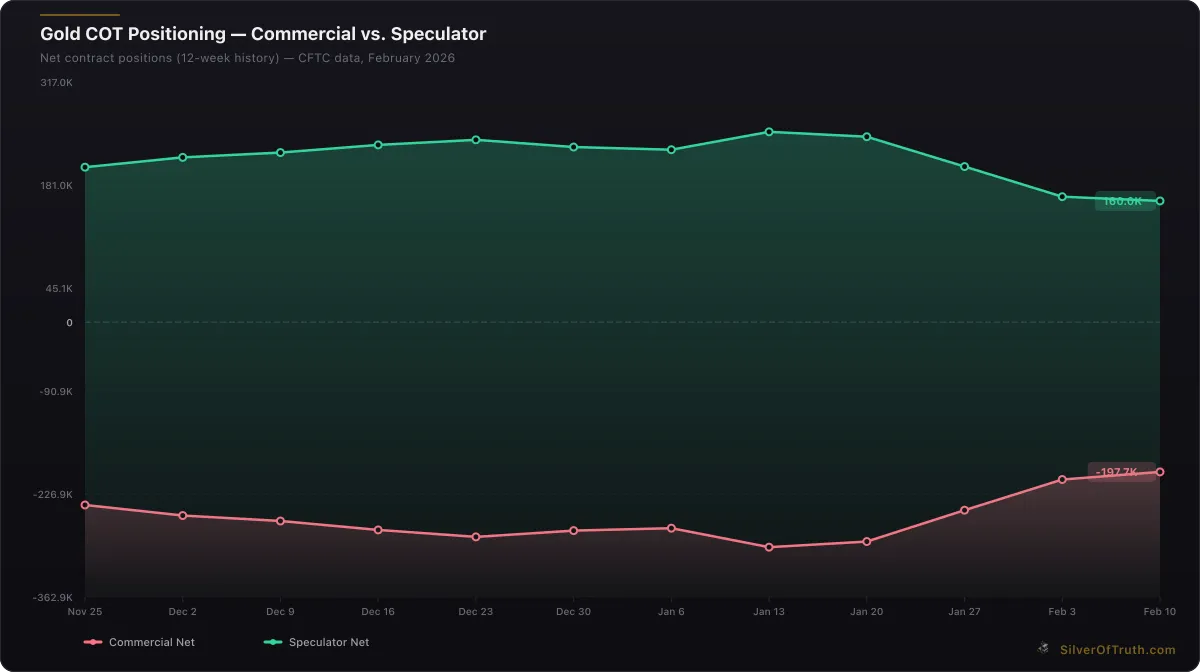

Current COT positioning data shows commercials net short 197,738 contracts while speculators maintain net long positions of 160,012 contracts. This configuration historically precedes significant price moves when physical demand overwhelms paper market positioning.

The gold-silver ratio at 65.53 remains elevated compared to historical averages, suggesting either gold strength or silver weakness. For investors considering precious metals exposure during de-dollarization trends, understanding gold-silver ratio dynamics helps optimize allocation strategies.

Investment Implications: Positioning for Monetary Transition

The de-dollarization trend creates both opportunities and risks for precious metals investors. As central banks systematically reduce dollar exposure while building gold reserves, understanding optimal positioning strategies becomes crucial for long-term wealth preservation.

Gold COT positioning: commercial hedgers (red) vs. speculators (green). Source: CFTC via SilverOfTruth, February 2026

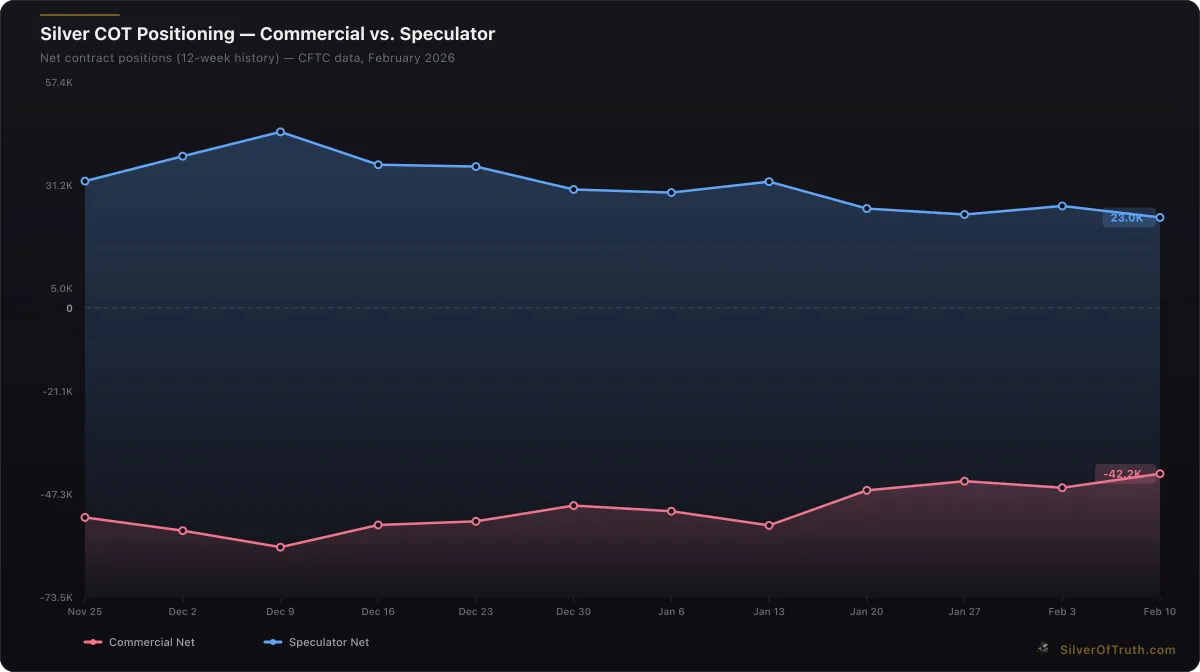

Silver COT positioning: commercial hedgers (red) vs. speculators (blue). Source: CFTC via SilverOfTruth, February 2026

Physical Gold Allocation: Central bank buying patterns suggest 5-20% gold allocation may be appropriate for portfolios seeking dollar alternative exposure. Physical vs paper silver analysis applies equally to gold—physical ownership eliminates counterparty risk that paper alternatives cannot.

Geographic Diversification: Consider gold storage outside traditional Western financial systems. Singapore, Switzerland, and UAE offer secure vaulting facilities beyond the reach of Western sanctions regimes.

Mining Stock Exposure: Gold mining companies provide leveraged exposure to gold price appreciation while generating cash flows in local currencies. Our guide on how to evaluate mining stocks explains key metrics for identifying quality producers positioned to benefit from sustained gold demand.

Currency Hedging: For dollar-based investors, gold positions provide natural hedge against dollar weakness. As de-dollarization accelerates, this hedging function becomes increasingly valuable for preserving purchasing power.

Risk Considerations

Volatility: Gold prices fluctuate significantly over short periods, requiring long-term investment horizon and appropriate position sizing.

Storage Costs: Physical gold ownership involves storage, insurance, and transaction costs that reduce net returns compared to paper alternatives.

Liquidity Constraints: Physical gold markets may face strain during crisis periods when demand spikes exceed available supply.

Regulatory Risk: Governments historically confiscated gold during monetary crises. Diversified storage and legal structures help mitigate this risk.

Opportunity Cost: Gold produces no cash flows, unlike dividend-paying stocks or interest-bearing bonds.

These risks must be balanced against gold's unique properties as monetary asset immune to currency debasement and political weaponization.

Regional Case Studies: De-Dollarization in Practice

Russia: Comprehensive Dollar Exit Strategy

Russia's approach to de-dollarization provides the most comprehensive real-world example of coordinated gold accumulation and dollar reduction. Before 2022 sanctions, Russia had systematically reduced dollar reserves from 40% to under 10% while increasing gold holdings to over 2,300 tonnes.

The Central Bank of Russia linked domestic gold purchases to mining production, creating captive demand for domestically produced metal. Gold-backed bonds and gold savings accounts channeled citizen savings into precious metals, reducing dependence on foreign currency systems.

Sanctions accelerated this process dramatically. Russia now requires unfriendly nations to pay for energy in rubles, effectively forcing currency conversion that bypasses dollar systems. While implementation faces practical challenges, the precedent demonstrates how major commodity exporters can leverage resource advantages to reduce dollar dependence.

China: Patient, Strategic Accumulation

China's de-dollarization strategy emphasizes gradual, systematic progress rather than confrontational policy changes. The People's Bank of China has quietly accumulated gold for over a decade while simultaneously developing yuan internationalization infrastructure.

The Shanghai Gold Exchange serves as both domestic and international trading platform, allowing central banks to purchase gold without accessing Western financial systems. Chinese commercial banks purchase gold on behalf of foreign central banks, obscuring the true extent of global reserve accumulation.

Belt and Road Initiative financing increasingly incorporates gold-backed elements, particularly for transactions with countries lacking hard currency reserves. This creates systematic demand for gold as China's economic influence expands across Asia, Africa, and Latin America.

India: Cultural and Strategic Alignment

India's gold strategy benefits from deep cultural affinity for precious metals combined with strategic monetary objectives. The Reserve Bank of India has steadily increased gold reserves while developing domestic gold financing instruments that reduce dollar dependence.

Gold bonds allow the government to borrow against gold reserves rather than foreign currency markets. Gold savings schemes channel household demand toward officially backed instruments, creating domestic gold ecosystem independent of Western financial systems.

India's large gold import requirements (typically 800-1,000 tonnes annually) provide leverage for negotiating bilateral trade arrangements that bypass dollar systems. Oil-for-gold swaps with producing nations exemplify how India leverages gold demand for strategic trade advantages.

Future Scenarios: Potential Outcomes and Timelines

The trajectory of de-dollarization and gold's role depends on several critical variables whose evolution will determine both timing and ultimate extent of monetary system transformation.

Gradual Transition Scenario (Most Likely)

Timeline: 10-15 years Probability: 60%

Dollar share of global reserves declines gradually from 60% to 40-45% as countries diversify into gold, yuan, euro, and other assets. Gold central bank demand remains elevated at 800-1,200 tonnes annually, supporting steady price appreciation.

Trade settlement diversification accelerates with bilateral arrangements reducing dollar usage in commodity transactions by 30-40%. Gold serves as neutral reserve asset backing these arrangements, creating structural demand floor.

This scenario assumes continued global economic integration despite monetary fragmentation. Gold prices reach $7,000-10,000 per ounce over the decade as systematic central bank buying supports fundamental demand.

Accelerated Crisis Scenario

Timeline: 3-5 years Probability: 25%

Major dollar crisis triggered by fiscal crisis, geopolitical shock, or loss of confidence accelerates de-dollarization timeline dramatically. Gold demand spikes as safe haven during monetary transition.

Emergency central bank gold purchases could reach 2,000+ tonnes annually as countries scramble to reduce dollar exposure. Physical gold shortages emerge as paper markets fail to clear at any price.

Gold prices potentially exceed $15,000 per ounce during acute crisis phases, before settling at permanently higher levels reflecting new monetary equilibrium.

Status Quo Maintenance Scenario

Timeline: Indefinite Probability: 15%

Dollar maintains dominance through successful policy reforms, renewed confidence, or failure of alternatives to gain traction. Gold demand moderates as de-dollarization momentum stalls.

Central bank purchases decline to historical averages of 400-600 tonnes annually. Gold prices appreciate modestly with general inflation but lack explosive momentum from monetary transition.

This scenario requires significant U.S. policy changes, resolution of geopolitical tensions, and failure of alternative monetary systems to develop successfully.

Frequently Asked Questions

What exactly is de-dollarization and why is it happening now?

De-dollarization refers to the process of reducing reliance on the U.S. dollar in international trade, central bank reserves, and global financial transactions. It's happening now due to several converging factors: geopolitical tensions that have weaponized dollar-based financial systems, concerns about U.S. fiscal sustainability, and the development of alternative payment and reserve systems by major economies like China and Russia. Central banks are seeking monetary sovereignty and protection against potential sanctions or currency instability.

How does gold benefit from de-dollarization trends?

Gold serves as the ultimate alternative to dollar-based reserve assets because it has no counterparty risk, cannot be frozen or weaponized by any government, and maintains value across different monetary systems. As countries reduce dollar reserves, they need alternatives—and gold's 4,000-year track record as money makes it the most trusted option. Central bank gold purchases have reached their highest levels in decades, creating sustained demand that supports gold prices independent of short-term market sentiment.

Which countries are leading the de-dollarization movement?

The BRICS nations (Brazil, Russia, India, China, South Africa) are at the forefront, along with their expanded membership including Saudi Arabia, UAE, and others. Russia has been the most aggressive, reducing dollar reserves from 40% to under 10% while tripling gold holdings. China has quietly accumulated over 2,000 tonnes of gold while developing yuan payment systems. Even traditional allies like Turkey and Poland have dramatically increased gold reserves while reducing dollar dependence.

Is de-dollarization realistic given the dollar's dominance?

Yes, though it will likely be gradual rather than sudden. The dollar's share of global reserves has already declined from over 70% in 2000 to about 60% today. Major structural changes take time—the British pound's decline as reserve currency took decades. However, the development of alternative payment systems, bilateral trade agreements, and systematic central bank gold purchases suggests the trend is real and accelerating, not merely political rhetoric.

How can investors position for this monetary transition?

Investors can consider several strategies: allocating 5-20% of portfolios to physical gold as insurance against dollar weakness, diversifying gold storage geographically outside traditional Western vaults, investing in quality gold mining companies for leveraged exposure, and understanding that gold serves as a hedge against currency debasement rather than a short-term trading vehicle. The key is viewing gold as monetary asset protection rather than speculative investment, with appropriate time horizons and risk management.

The convergence of geopolitical pressures, fiscal concerns, and technological alternatives is reshaping the global monetary order after seven decades of dollar dominance. Central banks worldwide are responding by systematically building gold reserves while reducing dollar exposure—a trend that creates fundamental demand for precious metals independent of traditional investment cycles.

With gold trading at $5,063.80 and central bank purchases at multi-decade highs, the de-dollarization movement represents more than political posturing. It reflects rational responses to structural vulnerabilities in dollar-centric systems and the search for true monetary sovereignty in an increasingly multipolar world.

For investors seeking to understand and position for this historic transition, gold's role as the ultimate dollar alternative becomes increasingly relevant. Track these developing trends and their market implications with comprehensive precious metals analysis tools available in the SilverOfTruth app on the App Store.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, investment, or trading advice. Past performance is not indicative of future results. Always conduct your own research and consult with a qualified financial advisor before making investment decisions. SilverOfTruth provides market data and analysis tools — it does not provide personalized financial advice.