Palladium's recent volatility masks deeper structural challenges plaguing the mining sector, where production costs have surged 15-20% annually across major operations. As palladium trades at $1,729 per ounce today—up 4.36% in the past 24 hours—mining companies face an increasingly complex landscape of rising operational expenses, supply chain disruptions, and resource depletion that threatens long-term production sustainability. This comprehensive analysis examines how escalating mining costs are reshaping palladium supply dynamics and what investors need to understand about the sector's evolving challenges. For broader mining sector fundamentals, explore our Mining Stock Analysis hub.

Quick Answer: Mining costs for palladium have increased 15-20% annually due to labor shortages, energy price inflation, and supply chain disruptions. These rising costs are forcing mine closures, reducing production capacity, and creating structural supply deficits that could support higher palladium prices despite short-term volatility.

What Are the Primary Cost Pressures Facing Palladium Miners?

Palladium mining operations face unprecedented cost inflation across multiple operational categories, fundamentally altering the economics of production. Labor costs represent the largest challenge, with skilled underground miners commanding 25-30% wage premiums compared to 2024 levels, according to Mining.com labor market reports. The palladium-rich Bushveld Complex in South Africa, which produces approximately 70% of global supply, has experienced particularly acute labor shortages as experienced miners retire faster than new workers enter the field.

Energy costs have emerged as the second-largest expense driver, with electricity rates in South Africa rising 18% year-over-year while diesel fuel for mining equipment has increased 22% globally. Anglo American Platinum reported that energy now represents 35% of total operating costs, compared to 28% in 2023. These increases directly impact All-In Sustaining Costs (AISC), the critical metric for mining profitability that includes not just extraction but also capital expenditures for maintaining operations.

Supply chain disruptions continue to plague equipment procurement and maintenance schedules. Critical mining components like conveyor belts, pumps, and safety equipment face 12-16 week delivery delays, compared to 4-6 weeks pre-pandemic. Norilsk Nickel, the world's largest palladium producer, recently disclosed that equipment delays contributed to a 3% production shortfall in Q4 2025.

The convergence of these factors has pushed average AISC levels for primary palladium producers to $1,850-$1,950 per ounce, compared to current spot prices near $1,729—creating margin pressure that threatens production sustainability.

How Do Rising Costs Impact Global Palladium Production?

The escalating cost structure is forcing fundamental changes in global palladium production patterns, with immediate implications for supply security. Mine closure decisions have accelerated, particularly among smaller operations with higher cost profiles. In 2025, 12 palladium-producing mines closed permanently due to cost pressures, removing approximately 185,000 ounces of annual capacity from global supply.

Production deferrals represent another critical impact, as companies postpone expansion projects and delay mine development. Sibanye-Stillwater announced a 6-month delay for its K4 shaft project in South Africa, citing construction cost overruns of 35% above original estimates. These delays compound supply tightness as older mines reach depletion without adequate replacement capacity.

The ore grade decline phenomenon exacerbates cost pressures, requiring miners to process larger volumes of rock to extract equivalent palladium content. Data from the USGS Mineral Commodity Summaries shows that average palladium ore grades have declined 8% since 2022, forcing higher extraction volumes and proportionally higher costs per ounce of refined metal.

Geographic concentration intensifies these challenges, with South Africa's political and economic instability adding additional risk premiums to production costs. Rolling electricity outages (load shedding) cost the South African platinum sector an estimated $1.2 billion in lost production during 2025, according to the Chamber of Mines.

What Role Do Supply Chain Disruptions Play in Cost Inflation?

Supply chain bottlenecks have evolved from temporary pandemic impacts to structural challenges that persistently inflate mining costs. Equipment availability remains severely constrained, with specialized underground mining machinery facing 20-24 week lead times compared to historical 8-12 week standards. This forces mining companies to maintain larger inventories of spare parts, tying up capital and increasing carrying costs.

Logistics costs have stabilized from pandemic peaks but remain 40-50% above pre-2020 levels due to fuel price inflation and driver shortages. Transporting palladium concentrate from remote mine sites to refineries now costs $280-320 per ton, compared to $195-220 per ton in 2022. These seemingly modest increases compound significantly given the tonnage volumes required for palladium extraction.

Chemical reagents essential for palladium refining have experienced severe price inflation, with critical processing chemicals increasing 25-35% in cost. Sodium cyanide, hydrochloric acid, and other specialized chemicals face supply constraints as chemical manufacturers prioritize higher-margin pharmaceutical and technology applications over mining sector contracts.

The semiconductor shortage has indirectly impacted palladium mining through equipment delays and control system upgrades. Modern mining operations depend heavily on automated systems and computerized equipment that require semiconductor components facing persistent shortages.

How Are Energy Costs Reshaping Mining Economics?

Energy represents the fastest-growing component of palladium mining costs, fundamentally altering project economics and operational decisions. Electricity consumption in underground palladium mines typically ranges 450-600 kWh per ounce of production, making operations extremely sensitive to power price fluctuations. South African electricity tariffs increased 18.65% in 2025, adding approximately $285 per ounce to production costs for typical operations.

Renewable energy transitions offer potential cost mitigation but require substantial capital investment that many mining companies cannot afford given current margin pressures. Anglo American Platinum's renewable energy initiative requires $1.8 billion in upfront investment to achieve 20% cost reduction in electricity expenses—a payback period of 8-12 years that exceeds many mine life cycles.

Fuel costs for mobile equipment and transportation add another layer of expense inflation. Diesel fuel prices averaging $1.45 per liter in South African mining regions represent a 22% increase from 2024 levels, directly impacting ore transport, equipment operation, and concentrate shipping costs.

Alternative energy sources like natural gas face similar inflation pressures, with industrial gas contracts increasing 28% year-over-year. This eliminates easy substitution strategies and forces mining companies to accept higher baseline energy costs as a structural reality.

Track real-time palladium pricing and mining sector developments with our Precious Metals Converter to understand current market dynamics.

What Are the Labor Market Challenges in Palladium Mining?

The palladium mining workforce faces severe structural imbalances that drive wage inflation and operational disruptions. Skilled labor shortages are most acute in underground mining positions, where safety requirements and technical complexity demand years of training and experience. The average age of underground miners in South African platinum operations is 47 years, with retirement outpacing new hires by a 3:1 ratio.

Safety regulations have tightened significantly following recent mining accidents, requiring additional safety personnel and equipment that increase operational costs. New safety protocols mandate additional ventilation systems, emergency response teams, and monitoring equipment that add $150-200 per ounce to production costs according to industry estimates.

Training costs for new miners have escalated as operations become more technically sophisticated. Companies now invest $35,000-45,000 per new hire in training programs, compared to $18,000-22,000 in 2022. The extended training periods reduce immediate productivity while front-loading expenses, creating cash flow challenges for operations.

Geographic isolation of many palladium mines complicates recruitment and retention, as workers demand premium compensation for remote locations with limited infrastructure. Housing, transportation, and family support costs add significant overhead to direct wage expenses.

How Do Environmental Regulations Increase Production Costs?

Environmental compliance costs represent a rapidly expanding component of palladium mining expenses, driven by stricter regulations and increased scrutiny of mining environmental impacts. Water treatment facilities now require sophisticated filtration and monitoring systems that cost $25-40 million to construct and $3-5 million annually to operate for typical underground operations.

Tailings management has become exponentially more expensive following recent dam failures in other mining sectors. New tailings facility designs require advanced engineering, continuous monitoring, and enhanced safety margins that increase construction costs by 60-80% compared to older standards. These facilities must operate for decades after mine closure, creating long-term financial liabilities.

Air quality monitoring and emission reduction systems add ongoing operational expenses, particularly for smelting and refining operations. Platinum group metal refineries must install scrubbing systems, particulate filters, and continuous emission monitoring that cost $15-25 million per facility upgrade.

Carbon taxation and offset requirements are emerging as additional cost factors, with South African carbon tax rates projected to increase 12% annually through 2030. Mining companies must either reduce emissions through expensive equipment upgrades or purchase carbon credits at current rates of $18-25 per ton of CO2 equivalent.

What Impact Do Geopolitical Factors Have on Mining Costs?

Geopolitical instability in key palladium-producing regions adds risk premiums and operational complications that increase effective production costs. South African political uncertainty surrounding mining rights, nationalization discussions, and regulatory changes forces companies to maintain higher cash reserves and pay premium insurance rates for political risk coverage.

Russian sanctions have eliminated a major global supplier from Western markets, reducing competition and increasing pressure on remaining producers. While this theoretically benefits non-Russian miners through higher prices, it also creates supply chain complications as replacement equipment sources must be identified and qualified.

Currency volatility between the U.S. dollar and local mining currencies creates hedging costs and planning complications. The South African rand's 12% depreciation against the dollar in 2025 provided some cost relief for dollar-denominated commodity sales, but volatile exchange rates force mining companies to maintain expensive hedging programs.

Export restrictions and licensing requirements add administrative costs and potential delays to palladium shipments. New export permit requirements in several African nations add 2-4 weeks to shipping schedules and require legal compliance expenses of $50,000-75,000 annually per operation.

How Are Mining Companies Adapting to Rising Costs?

Palladium mining companies are implementing diverse strategies to manage cost inflation, though many approaches require substantial capital investment with uncertain returns. Operational efficiency improvements focus on automation and digitization, with companies investing in autonomous mining equipment, AI-powered ore sorting, and predictive maintenance systems to reduce labor dependency and improve productivity.

Joint ventures and consolidation have accelerated as smaller operators seek economies of scale to spread fixed costs across larger production bases. The proposed merger between Impala Platinum and Royal Bafokeng Platinum aims to reduce combined operating costs by 8-12% through elimination of duplicate functions and shared infrastructure.

Technology adoption includes advanced metallurgical processes that improve recovery rates from existing ore bodies. New flotation and refining techniques can increase palladium recovery by 3-7%, effectively expanding reserves without additional mining costs. However, these technologies require $50-100 million in upfront investment per facility.

Strategic partnerships with automotive manufacturers—palladium's primary end users—provide price stability through long-term supply contracts, reducing exposure to spot price volatility. These agreements typically include inflation adjustment clauses that help offset rising production costs.

Monitor mining sector developments and operational efficiency metrics with our Mining Stock Screener to track how companies are adapting to cost pressures.

What Are the Long-Term Supply Implications?

The sustained cost inflation in palladium mining creates structural supply constraints that extend beyond current production challenges. Reserve replacement has become increasingly expensive, with new deposits requiring higher capital investment per ounce of recoverable palladium. Exploration budgets have declined 18% industry-wide as companies prioritize maintaining existing operations over developing new resources.

Mine life extensions face economic hurdles as deeper mining levels require additional infrastructure investment and higher operating costs. Many operations approaching end-of-life cannot justify the capital expenditure needed to access remaining resources at current cost levels and price volatility.

Secondary supply from recycling automotive catalysts provides approximately 25% of global palladium supply, but collection and processing costs have also increased significantly. Catalyst recycling facilities report 12-15% higher processing costs due to labor and chemical price inflation.

Substitution pressures from automotive manufacturers seeking alternatives to palladium in catalytic converters could reduce long-term demand, making high-cost mining investments less attractive. However, technical challenges in substitution ensure continued palladium demand for specialized applications.

How Do Current Market Conditions Affect Mining Investment Decisions?

Current palladium market dynamics create challenging conditions for mining investment decisions, as price volatility conflicts with long-term capital planning requirements. Capital allocation has shifted toward maintaining existing operations rather than expanding production capacity, with industry capital expenditure down 23% year-over-year despite rising costs.

Risk assessment methodologies now incorporate climate change impacts, regulatory uncertainty, and supply chain resilience as core factors in project evaluation. These expanded risk criteria have increased required rates of return for new projects from 12-15% to 18-22%, making fewer developments economically viable.

Financing costs for mining projects have increased substantially as lenders demand higher risk premiums for commodities perceived as vulnerable to substitution and technological disruption. Project debt financing costs have increased 200-300 basis points above risk-free rates compared to historical 100-150 basis point spreads.

Asset valuation methodologies increasingly emphasize operational flexibility and cost adaptability over pure resource quantity, recognizing that fixed-cost operations face higher risk in volatile commodity markets. This shift favors mechanized surface operations over labor-intensive underground mines, though palladium deposits predominantly require underground extraction.

What Are the Investment Implications for Palladium Exposure?

Rising mining costs create complex investment implications that favor different types of palladium exposure under different scenarios. Physical palladium benefits from supply constraints and production challenges, though storage costs and liquidity limitations complicate individual investment strategies. Professional storage and insurance add $35-50 per ounce annually in carrying costs.

Palladium ETFs provide market exposure without storage complications, though expense ratios of 0.60-0.95% annually and potential tracking errors reduce total returns. The PALL and PDBC ETFs hold physical palladium and palladium futures respectively, offering different risk-return profiles.

Mining stock selection becomes increasingly critical as cost structures vary dramatically between operators. Companies with lower-cost operations, strong balance sheets, and operational flexibility will outperform higher-cost producers facing margin compression. Key metrics include AISC trends, debt levels, operational efficiency improvements, and geographic diversification.

Royalty and streaming companies offer leveraged exposure to palladium prices while avoiding direct operational risks. These companies provide upfront capital to mining operations in exchange for future metal deliveries at predetermined prices, capturing upside from higher commodity prices without bearing production costs.

For detailed mining stock analysis and evaluation criteria, reference our comprehensive guide to evaluating mining stocks and understand the importance of AISC metrics in mining operations.

How Do Palladium Production Costs Compare to Other Precious Metals?

Palladium's production cost structure differs significantly from gold and silver mining, creating unique supply-demand dynamics. Extraction complexity for platinum group metals requires more sophisticated processing techniques compared to gold or silver, resulting in higher baseline costs. Typical palladium operations require 12-18 months from ore extraction to refined metal, compared to 3-6 months for gold.

By-product relationships complicate cost allocation, as most palladium comes from platinum or nickel mining operations where palladium represents 20-40% of total revenue. This makes pure-play cost analysis challenging and creates supply inflexibility—palladium production cannot easily respond to price signals independent of platinum and nickel market conditions.

Processing infrastructure for palladium requires specialized refineries with capabilities for separating platinum group metals, limiting the number of qualified facilities globally. This concentration increases processing costs and creates potential bottlenecks during maintenance periods or operational disruptions.

Quality specifications for automotive-grade palladium demand 99.95% purity levels, requiring additional refining steps that increase costs compared to investment-grade gold or silver products. These stringent specifications eliminate lower-cost refining alternatives and maintain processing expense at elevated levels.

What Are the Regional Production Cost Variations?

Regional cost differences significantly impact global palladium supply patterns and mining company competitiveness. South African operations face the highest cost structure due to deep underground mining requirements, labor-intensive extraction methods, and infrastructure challenges. Average AISC levels reach $1,850-$1,950 per ounce for Bushveld Complex operations.

Russian production from Norilsk Nickel historically enjoyed lower costs due to by-product economics from nickel mining and state-controlled energy pricing. However, sanctions and export restrictions have complicated cost comparisons and market access for Russian palladium.

Canadian operations benefit from political stability and advanced mining infrastructure but face higher labor costs and environmental compliance expenses. Stillwater Mining in the United States operates the only significant primary palladium mine outside Russia and South Africa, with AISC levels around $1,650-$1,750 per ounce.

Recycling operations concentrated in developed markets face different cost pressures, primarily from collection logistics and processing facility compliance. Automotive catalyst recycling costs have increased 12% annually due to sorting technology requirements and environmental regulations.

How Do Cost Pressures Affect Mining Company Profitability?

Rising costs are compressing profit margins across the palladium mining sector, forcing companies to optimize operations or face potential losses. Margin analysis reveals that primary palladium producers require sustained prices above $1,800 per ounce to generate positive free cash flow, compared to $1,400-$1,500 per ounce break-even levels in 2022.

Cash flow generation has deteriorated significantly, with many operations shifting from cash-generative to cash-consuming despite stable or higher palladium prices. This forces companies to rely increasingly on debt financing or equity raises to maintain operations, diluting shareholder returns.

Capital investment decisions now require higher hurdle rates to justify expansion or modernization projects. Companies demand 20-25% internal rates of return compared to historical 15-18% requirements, making fewer projects economically viable and constraining future supply growth.

Dividend sustainability faces pressure as mining companies prioritize cash conservation over shareholder distributions. Several palladium-focused miners have suspended or reduced dividends to maintain operational flexibility amid cost inflation.

Use our Stack Calculator to evaluate palladium investment sizing relative to other precious metals in your portfolio allocation strategy.

What Cost Mitigation Strategies Are Proving Effective?

Mining companies are implementing various cost mitigation strategies with mixed success rates and different implementation timelines. Automation investments show the most promise for long-term cost reduction, with autonomous haulage systems reducing labor costs by 15-20% while improving safety metrics. However, initial capital requirements of $50-80 million per system limit adoption to larger operations.

Energy efficiency programs focus on waste heat recovery, optimized ventilation systems, and equipment timing to reduce power consumption during peak rate periods. These initiatives typically achieve 8-12% energy cost reductions with payback periods of 18-36 months.

Predictive maintenance using AI and sensor networks reduces unplanned equipment downtime and extends asset life cycles. Companies report 20-30% reduction in maintenance costs through early problem detection, though system implementation requires 12-18 months and significant technical expertise.

Supply chain optimization includes strategic inventory management, alternative supplier development, and group purchasing agreements. Joint procurement initiatives among mining companies have achieved 5-8% cost savings on major equipment categories through increased buying power.

How Do Market Price Fluctuations Impact Mining Decisions?

Palladium's inherent price volatility complicates mining investment decisions and operational planning, especially when combined with rising cost pressures. Price risk management has become increasingly sophisticated, with companies using complex hedging strategies to secure minimum revenue levels while maintaining upside exposure.

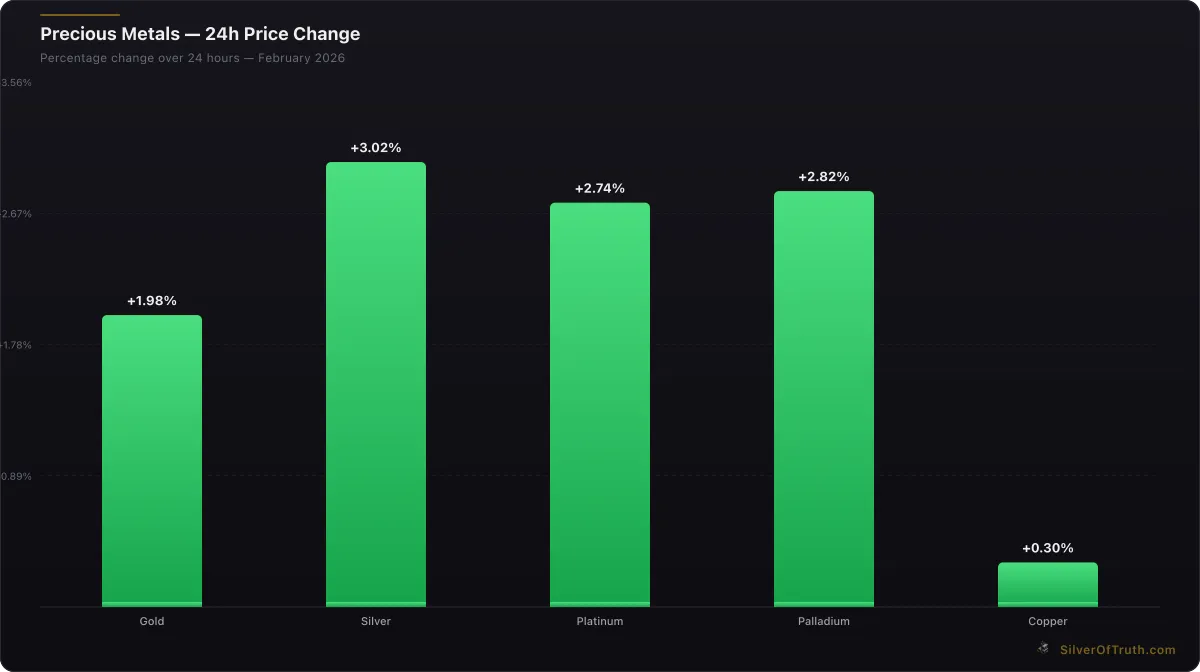

24-hour precious metals price changes. Source: SilverOfTruth, February 2026

Production flexibility becomes valuable as companies seek to adjust output based on real-time profitability calculations. Operations with lower fixed costs and modular production capabilities can reduce output during unprofitable periods and increase production when margins improve.

Contract structures with automotive buyers increasingly include cost adjustment mechanisms that help mining companies manage inflation pressures. These contracts typically reset pricing quarterly based on published cost indices, though implementation requires extensive negotiation and documentation.

Working capital management requires careful coordination of inventory levels, receivables collection, and payables timing to optimize cash flow during price volatility periods. Many companies maintain 60-90 days of operating expenses in cash reserves to manage temporary margin compression.

What Does the Future Hold for Palladium Mining Costs?

Long-term cost trajectories for palladium mining remain concerning, with structural factors supporting continued inflation pressures. Resource depletion in mature mining districts requires accessing deeper, lower-grade ore bodies that inherently cost more to extract. The Bushveld Complex faces increasing depths and geological complexity as surface and near-surface deposits become exhausted.

Environmental compliance costs will likely increase as regulations tighten and climate change mitigation becomes mandatory. Carbon pricing mechanisms, water usage restrictions, and biodiversity protection requirements add ongoing operational expenses that may accelerate over time.

Technology adoption offers potential cost relief but requires substantial upfront investment and operational expertise that many companies lack. The transition to electric mining equipment, autonomous systems, and AI-driven optimization requires transformational capital expenditure and technical capabilities.

Market consolidation among mining companies may provide economies of scale and cost reduction opportunities, though regulatory approval and integration challenges limit the pace of industry restructuring. Larger, well-capitalized operators are likely to acquire distressed assets at favorable valuations, potentially improving overall sector cost efficiency.

For comprehensive analysis of mining sector investment strategies and cost evaluation methodologies, explore our detailed mining stock evaluation guide and learn about royalty company alternatives that provide exposure without direct operational risks.

Frequently Asked Questions

What are the main cost drivers in palladium mining? Labor costs (30-35% of total), energy expenses (25-30%), equipment and maintenance (15-20%), and environmental compliance (10-15%) represent the primary cost categories. Labor shortages and energy inflation are currently driving the fastest cost increases.

How much has palladium mining AISC increased recently? Industry-wide All-In Sustaining Costs have increased 15-20% annually since 2024, reaching $1,850-$1,950 per ounce for primary producers compared to $1,400-$1,500 per ounce in 2022.

Which palladium mining regions face the highest cost pressures? South African operations in the Bushveld Complex face the highest costs due to deep underground mining, labor challenges, and infrastructure limitations. AISC levels reach $1,950 per ounce compared to $1,650-$1,750 in North American operations.

How do rising costs affect palladium prices? Higher production costs create a price floor effect, as marginal producers exit the market when prices fall below break-even levels. This reduces supply and supports higher prices, though demand fluctuations can override supply constraints in the short term.

What investment strategies work best in high-cost mining environments? Focus on low-cost producers with strong balance sheets, consider royalty companies that avoid operational risks, and evaluate companies with operational flexibility to adjust production based on market conditions. Diversification across multiple palladium exposure methods reduces concentration risk.

Sources

- Mining.com labor market analysis: https://www.mining.com

- USGS Mineral Commodity Summaries: https://www.usgs.gov/centers/nmic/mineral-commodity-summaries

- Anglo American Platinum operational reports: https://www.angloamerican.com

- CME Group palladium futures data: https://www.cmegroup.com/markets/metals.html

- World Platinum Investment Council supply data: https://platinuminvestment.com

- South African Chamber of Mines cost studies: https://www.chamberofmines.org.za

Track live palladium pricing, mining sector performance, and operational metrics in the SilverOfTruth app — available on the App Store.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, investment, or trading advice. Past performance is not indicative of future results. Always conduct your own research and consult with a qualified financial advisor before making investment decisions. SilverOfTruth provides market data and analysis tools — it does not provide personalized financial advice.