Palladium jumped 3.8% to $1,767 per ounce on February 16, delivering its strongest single-day performance in weeks despite the electric vehicle revolution threatening its primary market. This counterintuitive rally raises critical questions about industrial demand patterns as the automotive industry undergoes its most dramatic transformation in a century.

The surge comes at a time when Tesla deliveries hit record highs and major automakers accelerate EV production timelines. Yet palladium, heavily dependent on gasoline engine catalytic converters, is climbing rather than collapsing. Understanding this paradox requires examining shifting industrial applications beyond traditional automotive uses and recognizing emerging demand sectors that could reshape the palladium market fundamentally.

Understanding Palladium's Industrial Foundation

Palladium's industrial profile differs dramatically from gold and silver, with over 80% of annual supply flowing into specific manufacturing applications. According to World Gold Council automotive catalyst data, internal combustion engines consume approximately 82% of global palladium production, making it the most industrially concentrated precious metal.

This concentration creates vulnerability as EV adoption accelerates, but also generates supply-demand imbalances when industrial users compete for limited supplies. Current global palladium production stands at roughly 6.8 million ounces annually, sourced primarily from Russian and South African mines. Unlike gold's diversified demand base spanning jewelry, investment, and central banks, palladium's fate hinges on specific industrial trends.

The metal's unique properties make it irreplaceable in certain applications. Palladium catalysts excel at converting harmful emissions in gasoline engines, while its hydrogen absorption capacity proves valuable in fuel cell technology. These characteristics explain why the 3.8% price surge reflects more than speculative trading—it signals genuine industrial demand evolution.

EV Growth Paradox: Why Palladium Is Rising

Electric vehicle sales expanded 35% globally in 2025, yet palladium prices climbed rather than crashed. This counterintuitive performance stems from several industrial factors that offset declining automotive catalyst demand. Understanding these dynamics requires examining both immediate supply constraints and emerging application growth.

Hybrid vehicle production provides a crucial bridge between traditional and electric powertrains. These vehicles require both electric motors and internal combustion engines, maintaining palladium catalyst demand while automakers transition manufacturing capacity. Silver Institute industrial metals analysis shows hybrid production increased 28% in 2025, partially offsetting pure EV growth impact on palladium consumption.

Electronics manufacturing represents palladium's fastest-growing application segment. Semiconductor production, particularly for EV control systems, requires palladium compounds for specialized processes. The irony is evident: electric vehicles reducing automotive palladium demand simultaneously drive electronics palladium consumption through advanced battery management systems and power electronics.

Hydrogen fuel cell development creates another demand vector. Fuel cell vehicles, considered complementary to battery EVs for heavy-duty applications, require significant palladium quantities for catalyst systems. As detailed in our analysis of mining sector challenges, supply constraints amplify price sensitivity to even modest demand increases.

Emerging Industrial Applications Beyond Automotive

Electronics miniaturization drives palladium consumption in unexpected areas. Multilayer ceramic capacitors (MLCCs), essential components in smartphones and automotive electronics, increasingly specify palladium electrodes for high-performance applications. The smartphone industry alone consumes approximately 400,000 ounces annually, with 5G infrastructure adding incremental demand.

Dental and medical applications provide steady demand growth. Palladium alloys offer biocompatibility advantages in dental crowns and surgical instruments, markets growing at 6% annually according to industry data. While representing smaller volumes than automotive applications, medical demand proves price-insensitive and recession-resistant.

Chemical processing industries utilize palladium catalysts for hydrogenation reactions in pharmaceuticals and fine chemicals. This demand segment correlates with global economic activity rather than automotive production, providing diversification benefits as transportation electrifies. Our coverage of platinum group metals dynamics explores how industrial catalyst applications create price support across multiple metals.

Investment demand occasionally influences palladium prices despite limited ETF structures. Physical palladium purchases by institutional investors seeking portfolio diversification can affect spot prices, particularly given the metal's smaller market size compared to gold and silver.

Supply Chain Vulnerabilities Amplifying Price Moves

Russian palladium production represents approximately 42% of global supply, creating geopolitical supply risks that amplify price volatility. Sanctions and export restrictions can quickly tighten physical markets, as witnessed during previous diplomatic tensions. This concentration risk becomes more pronounced as EV growth reduces alternative demand flexibility.

South African mining operations face ongoing challenges from power shortages and labor disputes. Anglo American Platinum and other major producers operate at reduced capacity, limiting supply growth potential. Mining cost inflation, detailed in our mining production analysis, pressures profitability and expansion planning.

Recycling rates remain lower for palladium than other precious metals. Automotive catalyst recycling recovers approximately 35% of palladium content, but electronics recycling proves more challenging due to lower concentrations and complex extraction processes. This recycling gap maintains pressure on primary supply sources.

Chinese industrial demand creates additional supply chain complexities. China's manufacturing growth drives electronics palladium consumption while domestic production remains minimal. Trade relationships and currency fluctuations influence Chinese buying patterns, affecting global price dynamics as explored in our geopolitical analysis.

Price Performance Analysis and Technical Factors

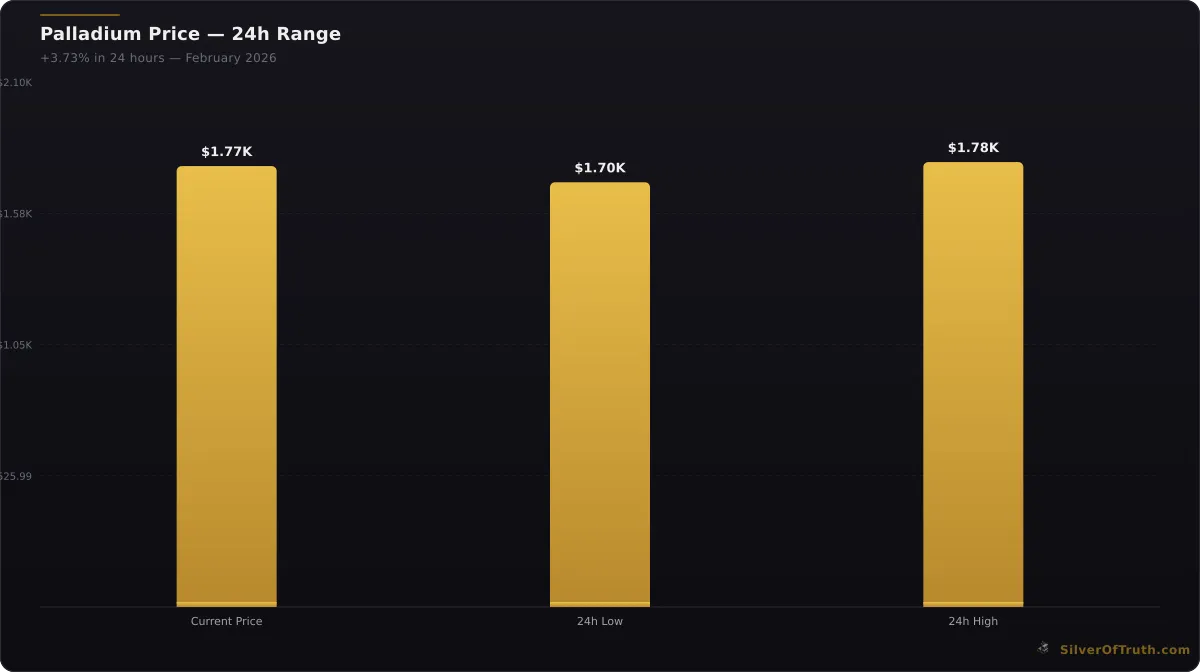

At $1,767 per ounce following the 3.8% daily gain, palladium trades within a complex technical environment. The metal reached daily highs of $1,783 before settling, suggesting profit-taking activity around resistance levels. Daily trading ranges from $1,702 to $1,783 indicate significant volatility and active speculative interest.

Palladium at $1767.00 — up 3.73% in 24h. Source: SilverOfTruth, February 2026

24-hour precious metals price changes. Source: SilverOfTruth, February 2026

Relative to other precious metals, palladium's performance stands out. While gold declined 0.66% and silver fell 1.96% on the same day, palladium's surge suggests metal-specific factors rather than broad precious metals sentiment. This divergence typically indicates industrial demand influences rather than monetary or investment flows.

Historical price patterns show palladium's tendency toward sharp moves during supply-demand imbalances. Previous rallies coincided with Russian export disruptions or automotive production surges, creating precedent for rapid price adjustment when physical markets tighten. The current 3.8% move, while significant, remains within normal volatility ranges for this metal.

Technical indicators suggest potential for continued strength if industrial demand materializes. However, palladium's historically volatile nature requires careful risk management, as downside moves can prove equally dramatic when industrial demand softens.

Investment Implications and Portfolio Considerations

Palladium's unique industrial characteristics create both opportunities and risks for precious metals investors. The metal's concentration in specific applications generates price sensitivity to technological shifts, but also creates potential for supply-demand imbalances during transition periods. Understanding these dynamics becomes crucial for portfolio allocation decisions.

Direct palladium investment options remain limited compared to gold and silver. Physical palladium purchases face higher premiums and storage costs, while ETF options provide more limited liquidity. These constraints may actually support price premiums during demand surges, as institutional buyers compete for available supplies.

The EV transition timeline affects palladium's investment thesis significantly. Accelerated electrification could pressure automotive demand sooner than expected, while delayed adoption extends traditional catalyst requirements. Investors must balance these opposing scenarios when considering palladium exposure.

As detailed in our comprehensive precious metals portfolio guide, diversification across multiple precious metals can provide exposure to different economic drivers while managing concentration risks inherent in single-metal investments.

Future Demand Scenarios and Market Outlook

Three primary scenarios emerge for palladium's industrial demand evolution. The base case assumes gradual EV adoption with hybrid vehicles maintaining catalyst demand through 2030, while emerging electronics applications offset some automotive decline. This scenario supports current price levels with modest volatility.

An accelerated electrification scenario could pressure palladium prices as automotive demand collapses faster than alternative applications develop. However, supply response limitations might prevent dramatic price declines, particularly if Russian production faces continued restrictions.

The breakthrough scenario involves significant hydrogen fuel cell adoption or new industrial applications that offset automotive demand losses. Recent developments in hydrogen infrastructure and electronics miniaturization suggest potential for demand surprises that could support higher price levels.

Market participants increasingly recognize palladium's supply-demand fundamentals differ from traditional precious metals. This recognition may reduce correlation with gold and silver during industrial demand cycles, creating unique investment characteristics within precious metals portfolios.

FAQ

Q: Why is palladium rising despite EV growth threatening its main market? A: Palladium benefits from hybrid vehicle production, electronics demand growth, and supply constraints that offset declining traditional automotive catalyst demand. The transition period creates complex demand patterns rather than simple decline.

Q: What industrial applications drive palladium demand beyond automotive catalysts? A: Electronics manufacturing (especially semiconductors and MLCCs), dental and medical devices, chemical processing catalysts, and emerging hydrogen fuel cell applications provide diversified demand sources.

Q: How do supply chain vulnerabilities affect palladium prices? A: Russian supply concentration (42% of global production) and South African mining challenges create supply risks that amplify price moves during demand changes or geopolitical tensions.

Q: Is palladium a good investment during the EV transition? A: Palladium offers unique exposure to industrial demand evolution but requires careful consideration of transition timelines and supply-demand balances. Limited investment options and high volatility demand risk management.

Q: How does palladium compare to other precious metals for portfolio diversification? A: Palladium's industrial concentration provides different economic exposure than gold's monetary characteristics or silver's dual investment-industrial nature, but creates higher volatility and concentration risks.

Track industrial palladium demand shifts and precious metals market dynamics in real-time with the SilverOfTruth app — available on the App Store. Get comprehensive coverage ratios, supply chain analysis, and price alerts for strategic positioning during market transitions.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, investment, or trading advice. Past performance is not indicative of future results. Always conduct your own research and consult with a qualified financial advisor before making investment decisions. SilverOfTruth provides market data and analysis tools. It does not provide personalized financial advice.