Palladium surged 4.36% to $1,729 per ounce today, breaking out of a sustained decline that has characterized the metal throughout 2026. However, this rally masks deeper structural challenges emanating from China's evolving industrial landscape and global economic realignments. The world's second-largest economy continues to reshape precious metals demand patterns, creating ripple effects that extend far beyond traditional automotive applications.

China's influence on palladium markets represents a critical intersection of industrial demand, geopolitical tensions, and supply chain vulnerabilities. As Beijing pivots toward electric vehicle dominance and implements new environmental policies, the implications for platinum group metals (PGMs) demand are profound. Understanding these dynamics is essential for investors navigating an increasingly volatile metals landscape shaped by our comprehensive gold investing fundamentals and broader market analysis.

Quick Answer: China's economic slowdown and EV transition are reducing automotive palladium demand, while geopolitical tensions with Russia create supply uncertainty. This combination drives extreme volatility as markets balance weakening industrial demand against potential supply disruptions.

What Is Driving China's Changing Palladium Demand?

China's automotive sector consumes approximately 30% of global palladium demand, primarily for catalytic converters in internal combustion engines. However, Beijing's aggressive push toward electric vehicle adoption is fundamentally altering this equation. The Chinese government's mandate that new energy vehicles (NEVs) comprise 40% of all auto sales by 2030 represents a structural headwind for palladium demand.

Recent data from the China Association of Automobile Manufacturers shows NEV sales jumped 37.9% year-over-year in January 2026, reaching 789,000 units. This acceleration in EV adoption directly translates to reduced palladium consumption, as electric vehicles require minimal precious metals compared to traditional internal combustion engines.

The shift extends beyond automotive applications. China's industrial palladium demand, historically driven by electronics and chemical processing, faces pressure from economic deceleration. The National Bureau of Statistics reported manufacturing PMI readings below 50 for three consecutive months, signaling contraction in industrial activity that typically drives metals consumption.

Moreover, China's property sector crisis continues to weigh on broader economic growth. With construction activity remaining subdued, the demand for industrial metals including palladium for catalytic applications in industrial equipment has weakened substantially. This creates a feedback loop where reduced economic activity further diminishes palladium consumption across multiple sectors.

How Do Global Economic Shifts Impact Palladium Volatility?

The interconnected nature of global supply chains means that economic shifts in major economies create cascading effects across metals markets. Palladium's unique supply-demand dynamics make it particularly susceptible to geopolitical and economic disruptions.

Russia supplies approximately 40% of global palladium production, primarily from Norilsk Nickel's operations in Siberia. Ongoing geopolitical tensions and sanctions related to the conflict in Ukraine continue to create uncertainty around Russian palladium exports. While direct sanctions on Russian palladium have been limited, the broader financial restrictions and insurance challenges for Russian commodity flows contribute to market uncertainty.

This supply concentration risk amplifies volatility when combined with demand fluctuations from major consuming regions. The European Union's accelerated transition away from Russian energy has broader implications for trade relationships, potentially affecting metals flows. Similarly, Japan's automotive sector, another major palladium consumer, faces supply chain challenges as it reduces dependence on Russian commodities.

Central bank monetary policies across major economies also influence palladium through currency effects and investment demand. The Federal Reserve's interest rate trajectory affects dollar strength, which inversely correlates with commodity prices denominated in USD. Higher rates strengthen the dollar, making palladium more expensive for international buyers and reducing investment appeal.

The combination of these factors creates a volatile environment where palladium prices can swing dramatically based on seemingly unrelated developments. Today's 4.36% surge to $1,729 reflects this dynamic, as markets respond to shifting expectations around Chinese demand recovery and Russian supply availability.

What Role Does Automotive Industry Transformation Play?

The global automotive industry's transformation toward electrification represents perhaps the most significant long-term challenge for palladium demand. Traditional internal combustion engines require approximately 2-7 grams of palladium per vehicle for catalytic converters, depending on engine size and emissions standards.

China's automotive market, the world's largest, is leading this transition. BYD, Tesla's main competitor in China, reported record quarterly deliveries of 944,000 vehicles in Q4 2025, with pure electric vehicles comprising 72% of sales. This shift pattern is accelerating across Chinese automakers, with traditional manufacturers like Geely and SAIC rapidly expanding EV production capacity.

The transformation isn't limited to China. The European Union's ban on internal combustion engine sales starting in 2035 creates a definitive timeline for reduced palladium demand in the region. Similarly, California's Advanced Clean Cars II regulation mandates that 100% of new passenger car sales be zero-emission by 2035, with other states following similar timelines.

However, the transition isn't uniform across all markets. Developing economies with less robust charging infrastructure continue to rely heavily on internal combustion engines. India, Southeast Asia, and parts of Africa represent growth markets for traditional automotive technology, providing some support for palladium demand in the near term.

The hybrid vehicle segment presents a nuanced picture. While hybrids still require catalytic converters, their smaller engines typically use less palladium than conventional vehicles. As manufacturers use hybrids as a bridge technology during the EV transition, palladium demand patterns become more complex and region-specific.

How Do Geopolitical Factors Influence Metal Price Dynamics?

Geopolitical tensions create supply uncertainty that often overshadows fundamental demand factors in palladium pricing. The metal's concentrated supply base makes it particularly vulnerable to political disruptions, trade restrictions, and financial sanctions.

Recent developments in US-China trade relations add another layer of complexity. While direct tariffs on palladium are minimal, broader trade tensions affect industrial demand patterns and supply chain configurations. Chinese manufacturers increasingly seek to reduce dependence on Western supply chains, potentially altering traditional metals trading flows.

The BRICS alliance's expansion and discussions of alternative payment systems for commodity trade could reshape palladium markets over time. As explored in our analysis of BRICS gold standard implications, these initiatives aim to reduce dollar dependence in international trade, potentially affecting how palladium transactions are conducted and settled.

Sanctions enforcement creates additional uncertainty. While palladium itself may not be directly sanctioned, the complex web of financial restrictions, shipping limitations, and insurance challenges affects market liquidity and pricing mechanisms. These factors contribute to the extreme volatility observed in recent months.

Mining companies also face geopolitical pressures. South African platinum group metals producers, which supply significant palladium as a byproduct of platinum mining, deal with ongoing power supply challenges and labor relations issues. These operational disruptions add supply-side volatility to an already complex market.

What Are the Investment Implications for Precious Metals Portfolios?

The evolving palladium landscape presents both challenges and opportunities for precious metals investors. Traditional portfolio allocation models may need adjustment as the fundamental drivers of palladium demand shift from automotive applications toward more specialized industrial uses.

Palladium's correlation with other precious metals has weakened in recent years, reflecting its distinct supply-demand fundamentals. While gold and silver often move together based on monetary factors, palladium increasingly trades on industrial and automotive-specific news. This divergence can provide portfolio diversification benefits but requires more specialized analysis.

The current market environment suggests increased attention to supply chain resilience and alternative sourcing strategies. Mining companies with diversified geographic exposure or alternative production methods may outperform those heavily dependent on traditional supply regions. Our mining stock analysis tools can help identify companies with favorable risk profiles.

Investment timing becomes crucial in such a volatile environment. While today's 4.36% surge might suggest momentum, the underlying bearish fundamentals from reduced Chinese demand and automotive transition suggest caution. Dollar-cost averaging strategies may be more appropriate than large position sizing in current conditions.

Physical palladium investment faces practical challenges due to the metal's specialized applications and limited retail market infrastructure. Unlike gold and silver, palladium lacks widespread coin and bar programs, making ETFs or mining stocks more accessible options for most investors.

How Does Current Market Positioning Compare to Historical Patterns?

Current palladium positioning reflects the market's struggle to balance competing factors. Today's price of $1,729 represents a recovery from recent lows but remains well below the $3,000+ peaks reached in early 2021 during supply disruption concerns.

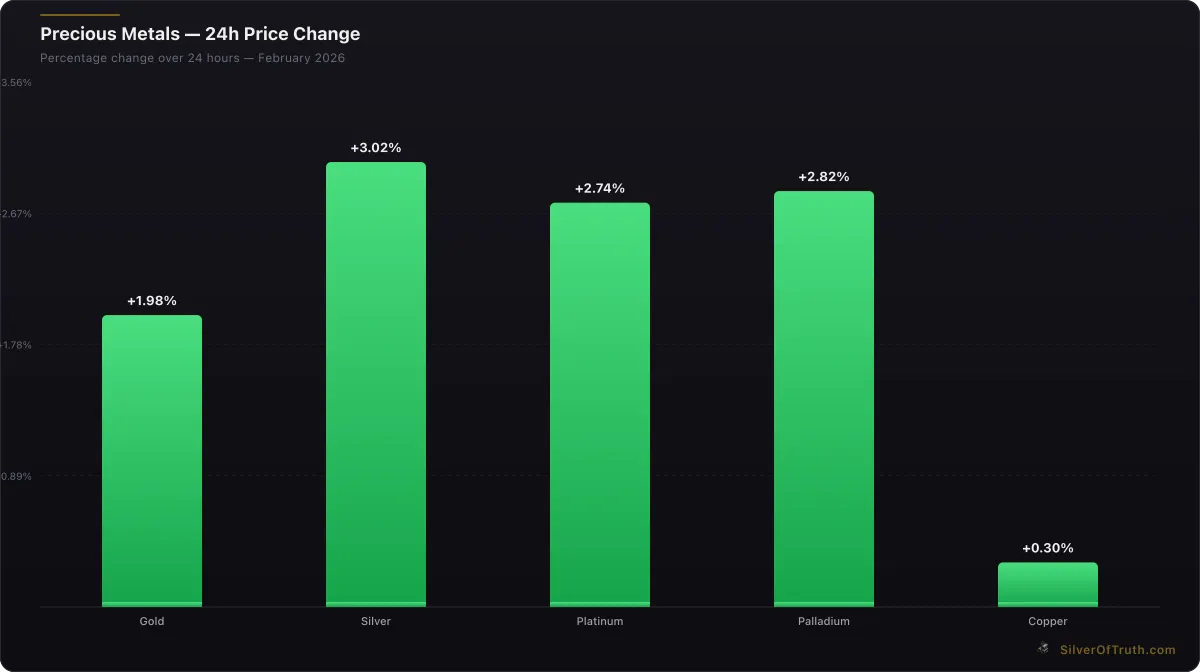

24-hour precious metals price changes. Source: SilverOfTruth, February 2026

Historical analysis shows palladium tends to be more volatile than gold or silver due to its smaller market size and concentrated supply base. The current volatility patterns align with periods of significant automotive industry disruption, such as the 2008-2009 financial crisis when auto sales collapsed globally.

However, the current situation differs from past cycles due to the structural nature of demand destruction from the EV transition. Previous palladium bear markets typically resulted from cyclical economic downturns that eventually reversed. The shift toward electric vehicles represents a permanent reduction in automotive palladium demand, making recovery more challenging.

Comparative analysis with our gold/silver ratio tracking shows palladium's divergent behavior. While gold and silver respond to monetary factors and maintain historical relationships, palladium's industrial focus creates different price drivers and correlation patterns.

Market concentration remains a key risk factor. The limited number of major palladium producers and the dominance of Russian supply create conditions where relatively small supply or demand changes can cause dramatic price movements. This concentration risk distinguishes palladium from more diversified precious metals markets.

What Does the Future Hold for China's Metal Demand?

China's economic trajectory will largely determine global metals demand patterns over the next decade. The country's shift toward a consumption-based economy, combined with environmental priorities and technological advancement goals, creates a complex outlook for industrial metals including palladium.

Beijing's 14th Five-Year Plan emphasizes high-quality development and carbon neutrality by 2060. This policy framework suggests continued support for electric vehicle adoption and renewable energy infrastructure, both of which reduce traditional palladium demand while potentially increasing demand for other metals like lithium, cobalt, and rare earth elements.

However, China's near-term economic challenges, including property sector deleveraging and demographic pressures, may limit overall metals consumption growth. The recent manufacturing PMI readings below 50 suggest continued industrial weakness that affects broad-based metals demand.

Technological developments in catalytic converter efficiency and recycling could also influence demand patterns. Improved catalyst designs that use less palladium per vehicle, combined with better recycling systems, could reduce primary demand even in markets that continue using internal combustion engines.

The timeline for automotive transition remains uncertain and region-dependent. While Chinese and European markets accelerate toward electrification, other regions may maintain internal combustion engine demand longer, providing some support for palladium markets during the transition period.

Frequently Asked Questions

Q: How much palladium does China actually consume compared to other countries? A: China consumes approximately 30% of global palladium demand, primarily through automotive catalytic converter production. The country's automotive sector uses roughly 2.2 million ounces annually, making it the second-largest consumer after the European Union's 2.5 million ounces.

Q: Will electric vehicle adoption completely eliminate palladium demand? A: While EV adoption significantly reduces automotive palladium demand, complete elimination is unlikely. Industrial applications including electronics, dental, and chemical processing continue to require palladium. However, automotive applications represent 80% of total demand, so EV transition creates substantial headwinds.

Q: How do Russian sanctions affect palladium availability? A: Direct sanctions on Russian palladium remain limited, but broader financial restrictions create supply chain uncertainty. Russia produces about 40% of global supply, so any disruption to these flows would significantly impact market balance and pricing.

Q: Should investors buy palladium during price volatility? A: Palladium's extreme volatility requires careful consideration of risk tolerance and investment timeline. While short-term trading opportunities exist, the structural headwinds from EV transition suggest caution for long-term positions. Consider position sizing and diversification within broader precious metals portfolios.

Q: What alternative investments capture similar themes to palladium? A: Investors interested in automotive transition themes might consider lithium, cobalt, or rare earth element investments through mining stocks or ETFs. These metals benefit from EV adoption rather than suffering from it. Traditional precious metals like silver also offer industrial exposure with different risk profiles.

The palladium market's evolution reflects broader themes of technological disruption, geopolitical realignment, and economic transition. As China's influence on global metals demand continues to evolve, investors must adapt their strategies to navigate an increasingly complex and volatile landscape. Understanding these dynamics provides essential context for precious metals portfolio management in an era of rapid industrial transformation.

For comprehensive precious metals market tracking, including real-time palladium prices and analysis, the SilverOfTruth app provides institutional-grade data on the App Store. Track these evolving market dynamics with our precious metals converter tool and stay informed about global economic shifts affecting metals markets.

Sources

- China Association of Automobile Manufacturers - Monthly Auto Sales Data: https://www.caam.org.cn

- National Bureau of Statistics of China - Manufacturing PMI: https://www.stats.gov.cn

- CME Group - Palladium Futures Data: https://www.cmegroup.com/markets/metals.html

- World Platinum Investment Council - Market Data: https://platinuminvestment.com

- U.S. Geological Survey - Mineral Commodity Summaries: https://www.usgs.gov/centers/national-minerals-information-center

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, investment, or trading advice. Past performance is not indicative of future results. Always conduct your own research and consult with a qualified financial advisor before making investment decisions. SilverOfTruth provides market data and analysis tools — it does not provide personalized financial advice.