Palladium's Supply Chain Crisis: Mining Vulnerabilities Exposed

Despite recent gains bringing palladium to $1,729 per ounce (up 4.36% in 24 hours according to current SilverOfTruth data), the platinum group metal (PGM) sector faces mounting structural challenges that threaten long-term price stability. The recent volatility in palladium markets has exposed critical vulnerabilities in global mining supply chains, from South African production bottlenecks to Russian geopolitical risks. Understanding these supply chain dynamics is crucial for investors navigating the complex landscape of precious metals mining, as detailed in our comprehensive mining stocks analysis hub.

Quick Answer: Palladium's price volatility reflects deeper structural problems in mining supply chains, including rising production costs, geopolitical risks concentrated in Russia and South Africa, and shifting automotive demand patterns. These vulnerabilities create both risks and opportunities for mining sector investors.

What Are the Primary Drivers Behind Palladium's Supply Chain Vulnerabilities?

The palladium market's instability stems from a highly concentrated supply base that makes the metal exceptionally vulnerable to disruptions. Russia and South Africa account for approximately 80% of global palladium production, creating a geographic concentration risk that has intensified since 2022's geopolitical tensions.

Production Cost Inflation represents the most immediate threat to mining profitability. According to recent industry data from Johnson Matthey's PGM Market Report, all-in sustaining costs (AISC) for palladium production have increased by 35-40% over the past two years. Energy costs, which represent 15-20% of total mining expenses, have surged alongside diesel fuel prices and electricity tariffs in South Africa.

Labor Market Pressures compound these challenges. South African mining companies face persistent strike risks and wage inflation pressures. The Association of Mineworkers and Construction Union (AMCU) has negotiated wage increases averaging 7-8% annually, outpacing productivity gains. This labor cost escalation directly impacts the economics of existing mines and raises the bar for new project development.

Infrastructure Bottlenecks further constrain supply chain efficiency. South Africa's state-owned power utility Eskom continues to implement rolling blackouts ("load shedding"), forcing mines to invest heavily in backup power generation. These infrastructure investments represent dead capital that doesn't increase production capacity but merely maintains operational continuity.

How Do Rising Mining Costs Impact Palladium Price Dynamics?

The relationship between mining costs and palladium prices creates a complex feedback loop that amplifies market volatility. Unlike gold or silver mines that can reduce production during price downturns, palladium extraction typically occurs as a byproduct of platinum or nickel mining, limiting operational flexibility.

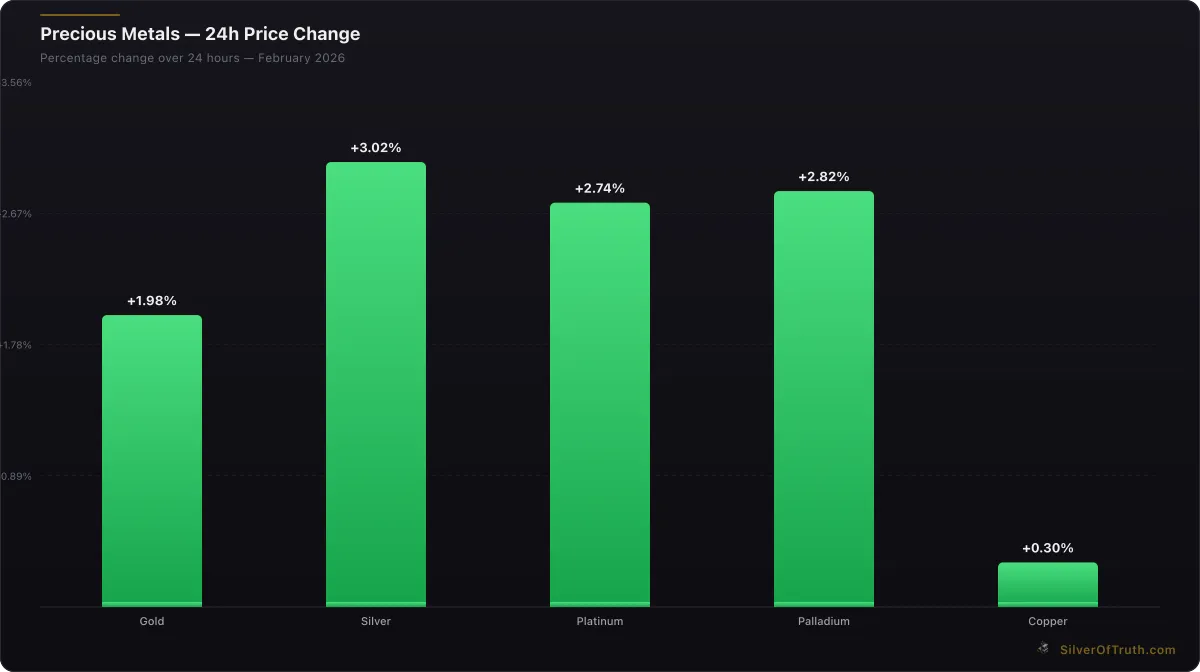

24-hour precious metals price changes. Source: SilverOfTruth, February 2026

Marginal Cost Support provides a theoretical price floor, but this support has proven unreliable during demand shocks. When automotive semiconductor shortages reduced catalyst demand in 2021-2022, palladium prices fell below marginal costs for several months, forcing high-cost producers to curtail operations despite the metal being a byproduct.

Capital Allocation Decisions by mining companies increasingly favor projects with shorter payback periods and lower capital intensity. Major producers like Anglo American Platinum and Sibanye-Stillwater have delayed expansion projects, citing uncertain demand outlook from the automotive sector's transition to electric vehicles.

The Project Pipeline Deficit becomes more pronounced as existing mines mature. New palladium projects require 7-12 years from discovery to production, creating a long lead time that makes supply responses sluggish. Current exploration budgets remain below 2010-2015 levels when adjusted for inflation, suggesting future supply constraints may persist.

Why Is Automotive Demand Shifting Creating Supply Chain Stress?

The automotive industry's evolution toward electrification creates unprecedented uncertainty for palladium demand projections. Traditional internal combustion engines require 2-7 grams of palladium per vehicle for catalytic converters, while electric vehicles eliminate this demand entirely.

Hybrid Vehicle Complexity adds another dimension to demand forecasting. Hybrid vehicles actually require more palladium per unit than conventional vehicles due to their more complex emissions systems and frequent start-stop cycles that stress catalysts. However, plug-in hybrids with larger electric ranges may reduce palladium intensity over time.

Regional Demand Variations reflect different electrification timelines. European markets are advancing faster toward electrification, with EU regulations requiring 55% emissions reductions by 2030. Conversely, markets like India, Brazil, and Southeast Asia may maintain internal combustion engine demand for decades, creating geographic arbitrage opportunities in palladium supply chains.

Inventory Management Challenges plague automotive manufacturers trying to balance just-in-time production with supply security. The 2020-2021 semiconductor shortage taught automakers that lean inventories create vulnerability, but holding excess palladium inventory ties up significant capital given the metal's high unit price.

Mining companies struggle to match production planning with these shifting demand patterns. Long-term sales contracts that once provided revenue certainty now carry execution risk if automotive demand falls short of projections.

What Role Do Geopolitical Risks Play in Mining Supply Chains?

Geopolitical concentration risk represents palladium's Achilles' heel, with Russian production accounting for approximately 40% of global mine supply. The Norilsk Nickel operations in the Krasnoyarsk region produce palladium as a byproduct of nickel mining, creating a single point of failure for nearly half the world's supply.

Sanctions Impact Analysis reveals the complexity of restricting Russian palladium exports. Unlike oil or gas, palladium exports don't directly fund military operations, but they do provide foreign exchange earnings. Western sanctions have focused on technology transfers and equipment exports to Russian mining operations rather than direct purchase restrictions.

Alternative Supply Development faces significant challenges. South African production capacity is largely mature, with declining ore grades increasing extraction costs. Canadian operations in the Sudbury Basin provide some supply diversity but cannot rapidly scale to offset Russian disruptions.

Stockpile Dynamics create additional uncertainty. Both government and private stockpiles of palladium remain opaque, making it difficult to assess how long accumulated inventories could buffer supply disruptions. The US Defense Logistics Agency maintains strategic stockpiles, but specific quantities and release triggers remain classified.

Price Volatility Amplification occurs when geopolitical tensions spike. Even potential supply disruptions can trigger speculative positioning that moves prices beyond what supply-demand fundamentals would justify. This volatility makes long-term planning difficult for both mining companies and end users.

How Are Mining Companies Adapting Their Operational Strategies?

Mining companies are implementing several strategic adaptations to navigate supply chain vulnerabilities and cost pressures. These operational changes will determine which producers survive and thrive in the evolving palladium landscape.

Technology Investment Priorities focus on automation and energy efficiency. Anglo American Platinum's deployment of autonomous haul trucks and remote-controlled drilling equipment reduces labor exposure and improves productivity. Energy management systems that optimize power consumption during South Africa's load shedding periods provide operational continuity.

Portfolio Optimization Strategies involve divesting high-cost, low-margin operations while investing in mechanized, scalable projects. Impala Platinum's decision to close its Marula mine while expanding Impala Rustenburg reflects this strategic rebalancing toward lower-cost production.

Financial Risk Management becomes increasingly sophisticated as companies hedge against currency volatility, energy price swings, and interest rate fluctuations. Forward selling programs for palladium production provide revenue certainty but may limit upside participation during price rallies.

Supply Chain Localization efforts aim to reduce dependence on imported equipment and consumables. Local procurement programs in South Africa face challenges due to limited manufacturing capacity, but they provide some insulation from global supply chain disruptions.

Use our mining stock screener to analyze how individual producers are implementing these strategic adaptations and their impact on operational metrics.

What Investment Implications Emerge from Supply Chain Analysis?

The structural vulnerabilities in palladium supply chains create both risks and opportunities for mining sector investors. Understanding these dynamics is essential for portfolio positioning in an environment of elevated uncertainty.

Valuation Methodology Adjustments must account for increased operational risks and cost inflation. Traditional discounted cash flow models using historical cost assumptions may overvalue mining assets if they don't reflect current inflationary pressures. Risk premiums for mining investments should increase to reflect supply chain vulnerabilities.

Diversification Considerations suggest investors should avoid concentration in single-metal producers heavily exposed to palladium. Companies with diversified PGM production (platinum, palladium, rhodium) or those with base metal exposures may provide better risk-adjusted returns.

Timing Strategic Considerations become crucial given the industry's cyclical nature and long development timelines. Current high costs and supply chain stress may create attractive entry points for patient capital, but investors must distinguish between temporary disruptions and permanent structural challenges.

ESG Compliance Requirements add another layer of complexity to investment decisions. Mining companies with stronger environmental, social, and governance practices may command valuation premiums as institutional investors implement sustainability mandates.

The intersection of supply chain vulnerabilities and investment analysis requires sophisticated frameworks that go beyond traditional financial metrics. Our comprehensive guide to evaluating mining stocks provides detailed methodologies for assessing operational risks alongside financial performance.

Are There Emerging Solutions to Supply Chain Resilience?

Innovation in mining technology and supply chain management offers potential solutions to current vulnerabilities, though implementation timelines extend over years rather than quarters.

Recycling Technology Advancement provides the most immediate supply diversification opportunity. Improved processing techniques for spent catalytic converters could increase secondary supply, reducing dependence on primary mining. Companies like Johnson Matthey and BASF are investing heavily in recycling capacity expansion.

Alternative Mining Jurisdictions show promise but require substantial development capital. The Thunder Bay North project in Ontario and the Platreef project in South Africa represent significant undeveloped resources, but their development timelines extend 5-7 years under optimal scenarios.

Digitalization and Predictive Analytics help optimize existing operations and reduce waste. Real-time monitoring systems can predict equipment failures, optimize ore blend ratios, and improve recovery rates. These incremental improvements compound over time to meaningfully impact cost structures.

Energy Transition Opportunities may offset automotive demand declines. Palladium's properties make it valuable for hydrogen fuel cell applications and industrial chemical processes. While these markets remain small relative to automotive catalyst demand, they could provide demand diversification over time.

FAQ

What percentage of global palladium supply comes from Russia and South Africa? Russia and South Africa combined account for approximately 80% of global palladium mine production, with Russia contributing about 40% and South Africa 40%. This geographic concentration creates significant supply risk for the global market.

How do rising mining costs affect palladium prices? Rising mining costs create a theoretical price floor by making high-cost production uneconomical below certain price levels. However, since palladium is primarily a byproduct of platinum and nickel mining, this cost support can be less reliable than for primary metals like gold.

What is the typical timeline for developing new palladium mining projects? New palladium projects typically require 7-12 years from discovery to production, including exploration, feasibility studies, permitting, construction, and commissioning phases. This long lead time makes supply responses to demand changes very sluggish.

How is the shift to electric vehicles affecting palladium demand? Electric vehicles eliminate palladium demand for catalytic converters, while hybrid vehicles may actually increase palladium usage per vehicle. The transition timeline varies by region, with Europe leading and emerging markets maintaining ICE demand longer.

What role do government stockpiles play in palladium markets? Government strategic stockpiles provide potential supply buffers during disruptions, but specific quantities and release triggers remain largely classified. Private stockpiles by automakers and refiners also influence market dynamics but lack transparency.

Understanding these supply chain vulnerabilities is crucial for navigating the complex precious metals landscape. For comprehensive market data and mining stock analysis, explore our mining stocks hub and track live developments with the SilverOfTruth app.

Sources

- Johnson Matthey PGM Market Report - Comprehensive platinum group metals market analysis

- World Platinum Investment Council - Industry data on platinum and palladium markets

- CME Group Metals Data - Futures market data and trading volumes

- Anglo American Platinum Annual Report - Leading producer operational data

- U.S. Geological Survey Mineral Commodity Summaries - Government production and reserves data

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, investment, or trading advice. Past performance is not indicative of future results. Always conduct your own research and consult with a qualified financial advisor before making investment decisions. SilverOfTruth provides market data and analysis tools — it does not provide personalized financial advice.