China's Metals Demand Slowdown: Palladium & Copper Impact

China's economic deceleration is creating ripple effects across global commodity markets, with palladium and copper bearing the brunt of reduced industrial demand. While palladium has recovered to $1,729 after recent volatility and copper holds steady at $5.813, underlying structural challenges in Chinese manufacturing and automotive sectors signal continued headwinds for these critical industrial metals. Understanding these global market shifts is essential for precious metals investors navigating an increasingly complex geopolitical landscape—explore our comprehensive Global Market Analysis for broader context on how international demand patterns affect your portfolio positioning.

Quick Answer: China's economic slowdown is reducing industrial demand for palladium (automotive catalysts) and copper (construction/electronics), despite recent price recoveries. Geopolitical tensions and supply chain diversification efforts are reshaping global metals flows, creating volatility and new risk premiums across industrial commodity markets.

What Is Driving China's Metals Demand Slowdown?

China's metals consumption patterns have shifted dramatically following the country's post-COVID economic reopening and subsequent moderation. The world's largest consumer of industrial metals is experiencing structural headwinds that extend far beyond cyclical economic weakness.

Manufacturing PMI data from China has shown persistent weakness in heavy industry sectors, with automotive production declining 2.8% year-over-year through January 2026 according to China Association of Automobile Manufacturers data. This directly impacts palladium demand, as approximately 80% of global palladium consumption comes from automotive catalytic converters—a sector where China represents nearly 30% of global vehicle production.

The construction sector, representing roughly 40% of China's copper demand, faces ongoing stress from property market corrections and infrastructure investment slowdowns. Copper wire and cable demand, traditionally a bellwether for Chinese industrial activity, has declined 15% from peak 2025 levels according to Shanghai Metals Market research. This weakness cascades through global supply chains, as China consumes approximately 54% of the world's refined copper annually.

Currency pressures compound demand challenges. The Chinese yuan's weakness against the dollar increases import costs for commodities priced in USD, making metals purchases more expensive for Chinese manufacturers and reducing demand elasticity. This dynamic particularly affects copper imports, where China's refined copper imports declined 8% in Q4 2025 compared to the previous quarter.

How Are Geopolitical Factors Reshaping Metals Markets?

Beyond economic fundamentals, geopolitical tensions are restructuring global metals supply chains in ways that create both opportunities and risks for different regions and commodities.

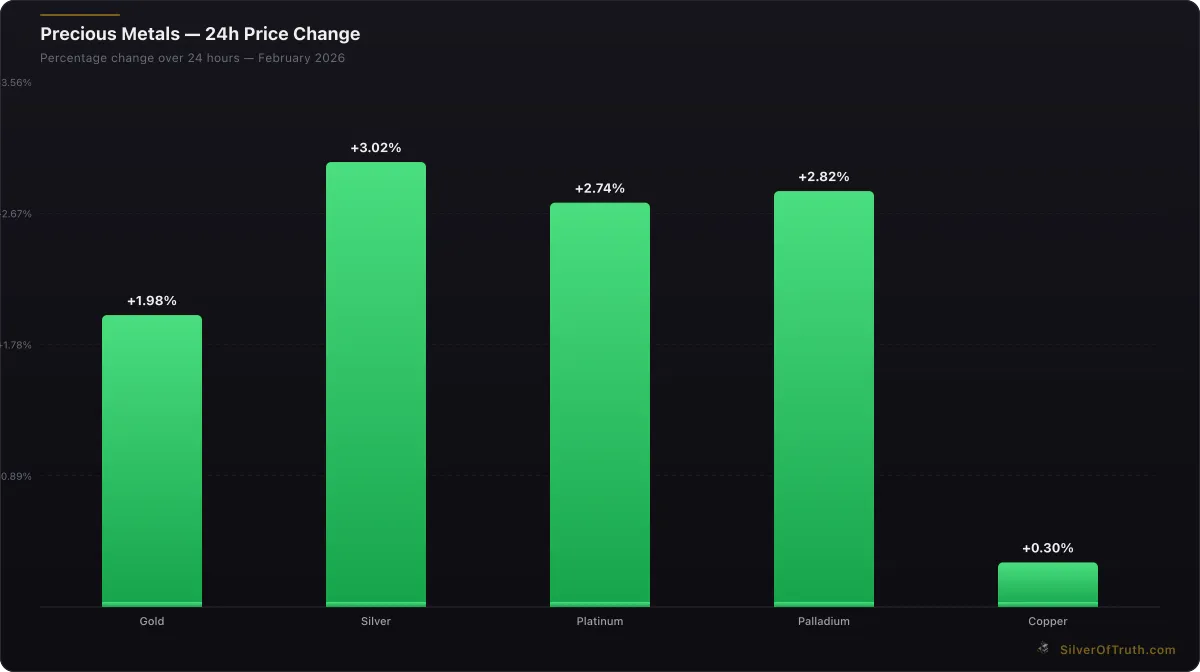

24-hour precious metals price changes. Source: SilverOfTruth, February 2026

Supply chain diversification efforts are accelerating as Western manufacturers seek alternatives to Chinese suppliers and Chinese companies look for new markets. This "friend-shoring" trend affects palladium and copper flows differently. For palladium, Russian supply restrictions continue to support prices despite demand weakness—Russia produces approximately 40% of global palladium supply, creating persistent supply chain vulnerabilities that maintain risk premiums.

Copper faces more complex dynamics. While Chinese demand moderates, emerging markets in Southeast Asia and India are increasing consumption as manufacturing capacity shifts away from China. Vietnam's copper imports increased 23% year-over-year in 2025, while India's refined copper consumption grew 12% according to International Copper Study Group data. However, these markets remain smaller than China, creating a net demand reduction globally.

Critical minerals initiatives from the U.S., EU, and other Western nations are also affecting market structure. The U.S. Inflation Reduction Act's domestic content requirements for EV battery materials are spurring investment in North American copper mining and processing capacity, potentially reducing long-term dependence on Chinese demand patterns.

Trade policy uncertainty adds another layer of complexity. Tariffs and export restrictions can create artificial supply constraints or demand surges, making fundamental analysis more challenging for industrial metals like copper where transportation costs and trade logistics significantly impact regional pricing.

What Does Palladium's Recent Recovery Signal?

Despite broader demand concerns, palladium has shown resilience, trading at $1,729 with a 4.36% daily gain as of February 13, 2026. This recovery reflects several factors beyond Chinese automotive demand.

Supply constraints remain the dominant narrative. While automotive demand from China has softened, Russian supply restrictions continue to limit available palladium globally. South African production, representing about 38% of global supply, faces ongoing operational challenges including power shortages and labor disputes that constrain output growth.

The automotive sector's transition to electric vehicles creates complex demand dynamics for palladium. While traditional ICE vehicles require palladium for catalytic converters, hybrid vehicles—which remain popular in China—actually use more palladium per vehicle due to their more complex emission systems. China's hybrid vehicle sales remained robust through 2025, partially offsetting pure EV adoption impacts on palladium demand.

Industrial demand beyond automotive provides some support. Palladium's use in electronics, dentistry, and chemical processing creates a demand floor, though these applications represent only about 15% of total consumption. Jewelry demand, particularly strong in China and India, also contributes to price stability during automotive sector weakness.

Speculative positioning in palladium futures markets shows significant volatility, with managed money positions swinging between extreme longs and shorts based on supply disruption fears versus demand destruction concerns. This creates price volatility that often disconnects from underlying fundamentals.

How Is Copper Navigating the China Challenge?

Copper's performance at $5.813 reflects the metal's complex relationship with global economic growth beyond China's specific challenges. As "Dr. Copper" for its economic forecasting reliability, the red metal's price action provides insights into broader global industrial trends.

Infrastructure spending outside China offers some demand support. The U.S. infrastructure bill continues driving copper demand for grid modernization and broadband expansion, while European green energy transition programs require significant copper investment for wind and solar installations. According to the International Energy Agency, renewable energy infrastructure uses 4-6 times more copper than conventional power generation.

The electric vehicle revolution creates long-term copper demand tailwinds despite Chinese automotive sector weakness. Each EV requires approximately 80 kilograms of copper compared to 20 kilograms for traditional vehicles. Global EV sales continue growing outside China, with European and North American markets showing strong adoption rates.

Supply side challenges provide price support independent of Chinese demand. Major copper mines worldwide face aging ore grades, requiring more energy and processing to extract copper from lower-quality deposits. Peru and Chile, representing about 40% of global mine production, continue experiencing operational and permitting challenges that constrain new supply development.

Market structure changes also affect copper pricing. Chinese strategic stockpile purchases, while reduced from peak levels, still provide periodic demand boosts. The Shanghai Futures Exchange's copper inventories remain well below historical averages, suggesting Chinese domestic supply tightness despite reduced industrial activity.

What Are the Investment Implications for Precious Metals Portfolios?

The divergent performance of industrial metals like palladium and copper versus monetary metals like gold and silver creates important portfolio positioning considerations for precious metals investors.

Correlation patterns are shifting as geopolitical factors become more important than traditional economic fundamentals. Historical relationships between copper prices and general economic growth are weakening as supply chain diversification and green energy transitions create new demand patterns independent of GDP growth.

For precious metals investors, industrial metals volatility affects mining company valuations differently than physical metals holdings. Mining companies with diversified operations across multiple metals benefit from these shifts, while single-metal focused miners face increased volatility from changing demand patterns.

Portfolio diversification strategies should consider that industrial metals like palladium and copper may provide different hedging characteristics than monetary metals. While gold and silver typically benefit from currency debasement and geopolitical tensions, industrial metals face demand destruction risks during economic slowdowns that precious metals may avoid.

Regional exposure within mining portfolios matters more in this environment. Companies with significant Chinese revenue exposure face different risks than those focused on Western markets or emerging economies outside China. Track these dynamics with our Mining Stock Screener for detailed company-specific analysis.

What Should Investors Watch Going Forward?

Several key indicators will determine whether current weakness in China metals demand represents a temporary correction or a structural shift requiring longer-term portfolio adjustments.

Chinese economic data releases remain critical, particularly manufacturing PMI, automotive production, and construction starts. However, investors should focus on leading indicators rather than lagging measures. Copper and steel futures prices on Chinese exchanges often signal demand changes before official statistics publication.

Central bank policy coordination affects metals markets through currency and liquidity channels. The People's Bank of China's monetary policy stance, relative to Federal Reserve policy, impacts yuan strength and Chinese import capacity for dollar-denominated commodities.

Geopolitical developments require ongoing monitoring, particularly regarding Russian sanctions, U.S.-China trade relations, and Western critical minerals initiatives. Supply chain disruptions from sanctions or trade restrictions can create short-term price spikes independent of fundamental demand changes.

Technological adoption rates for EVs and renewable energy will determine long-term copper demand growth trajectories. While Chinese EV adoption may moderate, global electrification trends continue supporting copper fundamentals beyond China-specific factors.

How Do These Trends Affect Broader Precious Metals Positioning?

The industrial metals weakness from Chinese demand slowdowns creates interesting contrasts with monetary precious metals performance. Gold's recent strength to $5,056 and silver's advance to $77.81 suggest investors are rotating from industrial commodities toward monetary hedges during economic uncertainty.

This rotation pattern historically signals broader economic concerns beyond China-specific issues. When industrial metals weaken while monetary metals strengthen, it often indicates fears about global growth rather than localized demand adjustments. Monitor our Live Silver Price and Gold Price tracker for real-time updates on these divergences.

COMEX inventory dynamics in precious metals remain disconnected from industrial metals trends, with silver registered inventory at 92.9M oz and gold at 17.6M oz showing different supply-demand characteristics than physically-delivered industrial metals markets.

For precious metals stackers, industrial metals weakness may create mining stock opportunities at attractive valuations while supporting the monetary demand case for physical gold and silver. This environment favors selective positioning rather than broad commodities exposure.

FAQ

Q: How long might China's metals demand slowdown persist? A: Structural factors including property market corrections and manufacturing capacity shifts suggest 12-18 months of continued weakness, though stimulus measures could provide temporary demand boosts.

Q: Does palladium's recent recovery indicate the worst is over? A: The recovery primarily reflects supply constraints rather than demand improvement. Automotive sector fundamentals remain weak, limiting upside potential despite short-term price strength.

Q: Should precious metals investors avoid mining stocks during this period? A: Not necessarily. Selective exposure to companies with limited Chinese revenue dependence and strong balance sheets may offer opportunities, while avoiding broad commodities or China-focused miners.

Q: How do these trends affect silver's industrial demand? A: Silver's industrial applications differ from copper and palladium, with electronics, solar, and medical uses showing different geographic demand patterns less dependent on Chinese automotive and construction sectors.

Q: Will supply chain diversification permanently reduce China's metals influence? A: Partial reduction likely, but China's scale means it will remain the dominant demand driver for most metals. Diversification creates more regional pricing variations rather than eliminating Chinese influence entirely.

Conclusion

China's metals demand slowdown presents complex challenges for palladium and copper markets that extend beyond simple supply-demand mathematics. Geopolitical factors, supply chain diversification, and technological transitions are reshaping how these critical industrial metals trade and creating new risk-return profiles for investors.

While palladium's recent recovery to $1,729 reflects supply constraints more than demand improvement, and copper's stability at $5.813 masks underlying weakness in key consuming sectors, these developments signal broader shifts in global commodity flows. Precious metals investors should view these trends as validation of monetary metals' hedging properties during periods of industrial uncertainty.

The divergence between industrial metals challenges and precious metals strength reinforces the portfolio protection argument for gold and silver allocation. As global supply chains adapt to new geopolitical realities, monetary metals may continue outperforming their industrial counterparts. For comprehensive analysis of how these global market shifts affect your precious metals strategy, explore our Silver Investing hub for educational resources and practical guidance.

Track these evolving dynamics in real-time with the SilverOfTruth app—available on the App Store for iOS users seeking professional-grade metals market intelligence.

Sources

- China Association of Automobile Manufacturers: https://www.caam.org.cn

- Shanghai Metals Market: https://www.smm.cn

- International Copper Study Group: https://www.icsg.org

- International Energy Agency: https://www.iea.org

- U.S. Geological Survey Minerals Information: https://www.usgs.gov/centers/national-minerals-information-center

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, investment, or trading advice. Past performance is not indicative of future results. Always conduct your own research and consult with a qualified financial advisor before making investment decisions. SilverOfTruth provides market data and analysis tools — it does not provide personalized financial advice.