Gold prices are experiencing one of the most dramatic rallies in precious metals history, driven by a powerful convergence of market forces that have transformed gold from a traditional safe-haven into an essential portfolio component. Seven key drivers are simultaneously propelling gold to record territory: Federal Reserve policy shifts, unprecedented central bank accumulation, escalating geopolitical tensions, persistent supply chain constraints, inflation hedging demand, currency debasement concerns, and technical momentum. Understanding these interconnected forces is crucial for investors seeking to comprehend not just why gold is surging, but whether this upward trajectory has lasting power. This analysis breaks down each driver behind gold's remarkable ascent, equipping you with the insights needed to make informed decisions about precious metals exposure in today's volatile market environment.

Driver #1: Federal Reserve Policy and Interest Rate Environment

The Federal Reserve's monetary policy stance represents the single most influential factor in gold's current rally. As a non-yielding asset, gold's attractiveness is inversely correlated with real interest rates—when adjusted for inflation, lower rates make gold more compelling relative to bonds and cash.

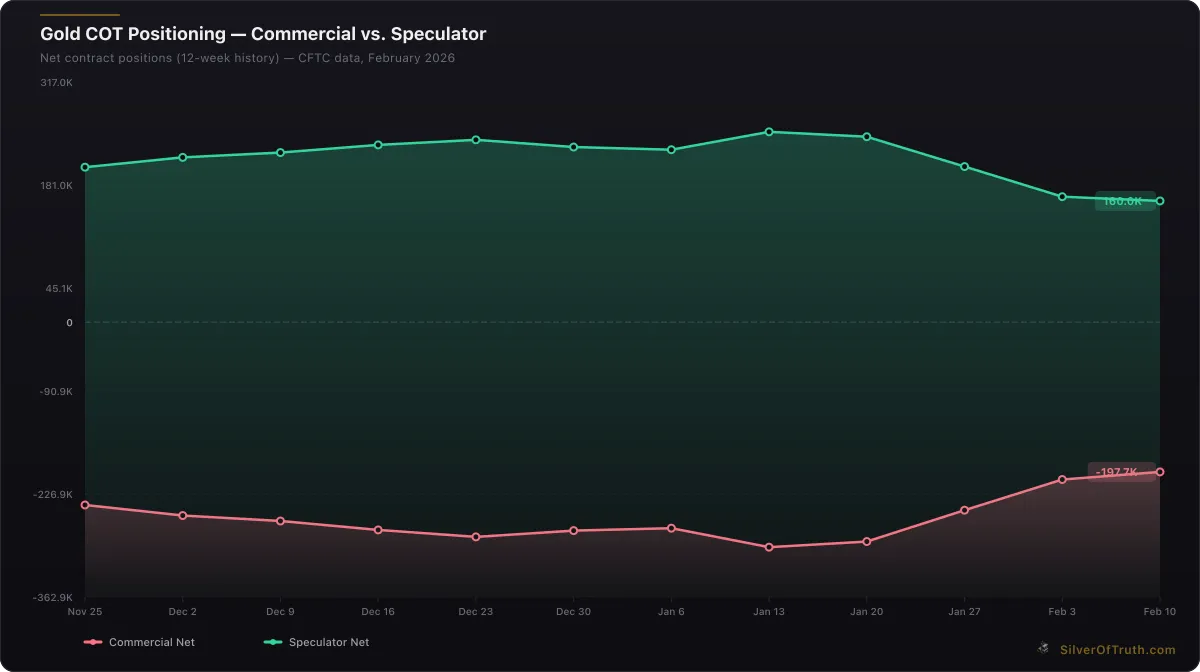

Gold COT positioning: commercial hedgers (red) vs. speculators (green). Source: CFTC via SilverOfTruth, February 2026

Recent Fed communications have signaled a potential pause in aggressive rate hikes, with several voting members expressing concerns about overtightening in the current economic environment. This shift in rhetoric has caused real interest rates to decline, reducing the opportunity cost of holding gold. When 10-year Treasury yields fell below inflation expectations in recent weeks, gold became effectively "free" to hold from a yield perspective.

The Fed's balancing act between combating persistent inflation and avoiding economic recession has created an environment where traditional monetary policy tools are less effective. This uncertainty about future rate paths has driven institutional investors toward gold as a hedge against both inflationary and deflationary scenarios—a rare dual-mandate that gold uniquely fulfills.

Market participants are also positioning for potential quantitative easing (QE) resumption if economic conditions deteriorate. Historical data shows gold prices typically surge during QE periods due to currency debasement concerns and increased money supply. The mere possibility of renewed asset purchases has contributed to gold's recent momentum.

Understanding how Federal Reserve rate signals could spark gold price rebounds provides crucial insight into this primary driver of precious metals performance.

Driver #2: Unprecedented Central Bank Accumulation

Central banks worldwide have become gold's most significant source of demand, with official sector purchases reaching levels not seen since the 1970s. According to the World Gold Council, central bank net purchases exceeded 1,000 tonnes annually for the past three years, representing approximately 20-25% of total annual gold demand.

This buying surge reflects a fundamental shift in monetary policy thinking. Central banks in emerging markets, particularly those in Asia, Eastern Europe, and Latin America, are diversifying their reserves away from dollar-heavy portfolios. Countries like China, Russia, Turkey, and India have led this charge, viewing gold as both a hedge against currency volatility and a strategic asset independent of Western financial systems.

The pace of accumulation has accelerated recently, with monthly purchase data showing consistent net buying even as gold prices reached multi-year highs. This behavior—buying into strength rather than weakness—signals conviction rather than opportunistic accumulation. Central banks typically have longer investment horizons and deeper research capabilities than private investors, suggesting their continued buying reflects fundamental value rather than speculative positioning.

China's People's Bank has been particularly active, adding over 300 tonnes to official reserves since 2022 while likely accumulating additional gold through state-owned entities not reflected in official statistics. This pattern of systematic accumulation by the world's second-largest economy provides substantial price support and reduces available supply for private markets.

The role of BRICS nations and gold in reshaping global monetary systems illustrates how central bank demand has evolved beyond traditional reserve management into strategic positioning for a multipolar financial world.

Driver #3: Geopolitical Tensions and Safe-Haven Demand

Global geopolitical instability has intensified significantly, driving institutional and individual investors toward gold's traditional safe-haven properties. Unlike previous periods where specific regional conflicts drove short-term spikes, current tensions span multiple theaters simultaneously, creating sustained rather than episodic demand.

The ongoing tensions between major powers have fundamentally altered investment risk assessments. Traditional safe assets like government bonds now carry sovereign risk premiums, particularly as sanctions and financial system weaponization have become standard diplomatic tools. Gold, being physically held and politically neutral, offers protection that paper assets cannot provide.

Military conflicts in Eastern Europe and the Middle East have demonstrated how quickly geopolitical events can disrupt global supply chains and energy markets. This has prompted both sovereign wealth funds and private investors to increase portfolio allocations to physical assets that maintain value regardless of political outcomes.

Currency wars and trade disputes have added another layer of uncertainty. As major economies implement competitive devaluations and trade restrictions, gold serves as a neutral store of value unaffected by bilateral political relationships. This has been particularly relevant for investors in emerging markets facing currency instability.

The fracturing of the post-1945 international order has created systemic risks that traditional diversification strategies cannot address. Gold's 5,000-year history as a store of value during periods of social and political upheaval makes it uniquely positioned to benefit from current global uncertainties.

Driver #4: Inflation Pressures and Currency Debasement

Despite central bank efforts to control inflation, underlying price pressures remain elevated across major economies. Core inflation readings continue above target levels in most developed nations, while supply chain disruptions and energy price volatility create recurring inflationary shocks.

Gold's effectiveness as an inflation hedge has been demonstrated across multiple economic cycles. When real returns on bonds and cash turn negative—as they have periodically over the past several years—gold maintains purchasing power even without yielding interest or dividends.

The broader trend of currency debasement extends beyond traditional monetary policy. Government debt-to-GDP ratios have reached historically high levels across developed nations, creating long-term pressure for currency devaluation as the only politically feasible method of debt reduction. This has prompted both institutional and individual investors to seek assets that maintain value independent of any single currency.

Central bank digital currencies (CBDCs) and the gradual reduction of cash usage have raised concerns about monetary control and financial privacy. Gold offers an alternative that cannot be digitally monitored, seized, or devalued through programming changes—characteristics that become more valuable as financial systems become increasingly digital and centralized.

Energy price volatility has created persistent inflationary pressures that are difficult to address through traditional monetary policy. As energy represents a significant input cost across all sectors, sustained high prices create embedded inflation that gold historically outpaces over extended periods.

Driver #5: Supply Constraints and Mining Challenges

Gold mining faces increasingly difficult operational challenges that limit new supply growth even as demand surges. The industry's all-in sustaining costs (AISC) have risen steadily due to declining ore grades, deeper mining requirements, and increased environmental regulations.

Major gold discoveries have become increasingly rare, with most new projects representing smaller deposits in more remote locations. The average time from discovery to production now exceeds 15 years due to permitting delays, environmental reviews, and community opposition. This long lead time means current high prices cannot quickly stimulate significant new supply.

Geopolitical risks have affected mining operations in several key producing regions. Political instability, changes in mining regulations, and resource nationalism have made some previously accessible deposits unavailable to international mining companies. This has reduced the effective global resource base and increased supply concentration risks.

Labor shortages and rising energy costs have further pressured mining economics. Many operations require significant diesel fuel for equipment and electricity for processing, making them vulnerable to energy price spikes. Skilled mining labor has become increasingly expensive and difficult to retain, particularly in remote locations.

Environmental, social, and governance (ESG) considerations have added compliance costs and limited access to certain deposits. While necessary for sustainable mining practices, these requirements increase capital expenditure and operational complexity, ultimately constraining supply growth relative to demand increases.

The difficulty of evaluating mining stocks in this environment has led many investors to prefer physical gold exposure over equity positions in mining companies, further increasing demand for the underlying metal.

Driver #6: Portfolio Diversification and Institutional Adoption

Modern portfolio theory increasingly recognizes gold's role as a portfolio diversifier that reduces overall volatility while maintaining return potential. Academic research demonstrates that gold's negative correlation with stocks during market stress periods makes it an effective hedge against equity market crashes.

Institutional adoption has accelerated significantly since 2020, with pension funds, insurance companies, and endowments adding gold allocations. Many institutions that previously avoided commodities now view gold as essential infrastructure for risk management, particularly given increasing correlation among traditional asset classes during crisis periods.

The introduction of physically-backed gold ETFs and improved storage solutions has made institutional gold ownership more practical and cost-effective. Professional money managers can now add gold exposure without the operational complexity of physical storage and insurance, removing significant barriers to adoption.

Quantitative analysis by major investment banks consistently shows that portfolios with 5-10% gold allocations achieve better risk-adjusted returns than those without precious metals exposure. This mathematical advantage has driven systematic allocation programs by large institutional investors.

The rise of alternative investment strategies, including hedge funds and family offices, has created a sophisticated investor base that understands gold's portfolio construction benefits beyond simple inflation hedging. These investors often maintain permanent gold positions as part of their strategic asset allocation.

Understanding how to integrate precious metals into broader investment strategies, including the differences between physical vs paper silver, helps investors maximize diversification benefits across the precious metals complex.

Driver #7: COMEX Market Dynamics and Physical Demand

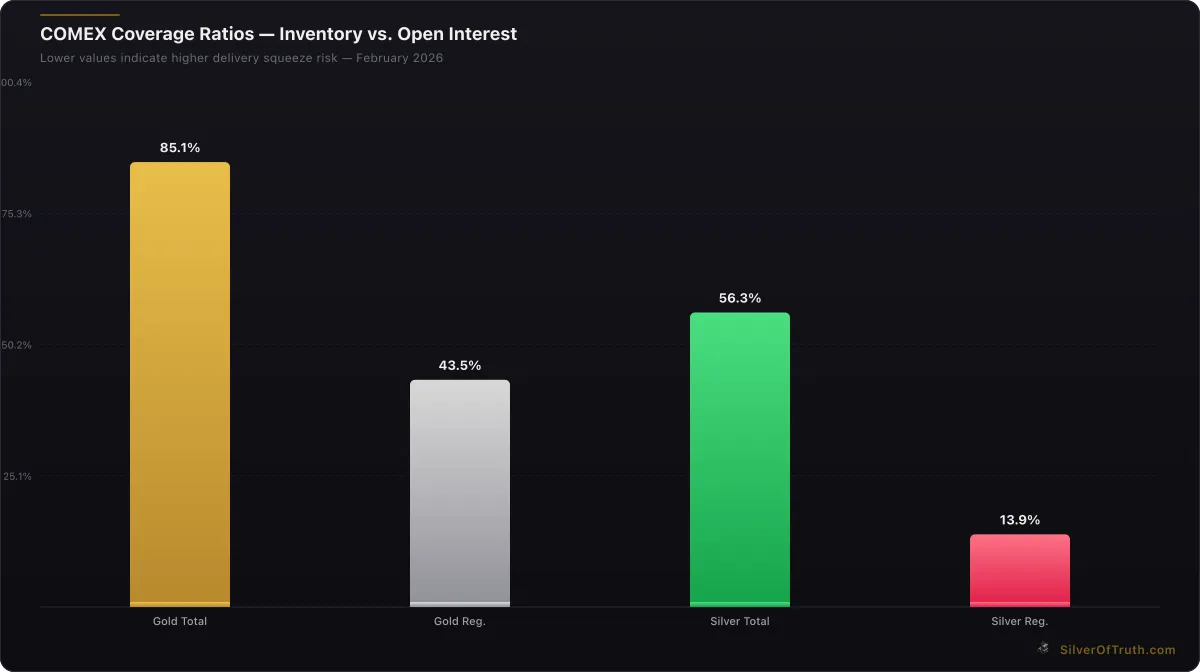

Current COMEX inventory data reveals significant strain on available gold supplies, with registered (deliverable) inventory at 17.58 million ounces against open interest of 404,391 contracts representing 40.44 million ounces of potential delivery obligations. This 43.5% coverage ratio, while classified as "medium" risk, has shown consistent monthly depletion of 4.76%.

Source: SilverOfTruth COMEX data, February 2026

COMEX coverage ratios — lower values indicate higher delivery squeeze risk. Source: SilverOfTruth, February 2026

The unusual dynamic where registered inventory (17.58M oz) exceeds eligible inventory (16.84M oz) suggests metal is being positioned for potential delivery rather than storage. This inversion from typical patterns indicates either preparation for significant outflows or recent shifts as holders prepare for withdrawal from the system.

COMEX delivery mechanisms show balanced activity with 35,850 contracts issued and stopped month-to-date, indicating steady physical demand without acute delivery stress. However, the consistent inventory decline suggests underlying tightness that could create squeeze conditions if demand accelerates.

Commitment of Traders (COT) data shows commercials maintaining heavily net short positions at -197,738 contracts (70.8% of open interest), while speculators hold net long positions of +160,012 contracts. Recent speculator selling of 5,592 contracts amid falling open interest suggests profit-taking rather than fundamental bearishness, potentially creating a more stable foundation for price advances.

The concentration of positions among large traders—with the top 4 controlling 33.8% of short positions—creates potential for rapid price movements if any major shorts cover positions. This market structure, combined with declining available inventory, suggests physical demand could overwhelm paper market mechanics.

Learning to interpret COMEX inventory trends and COT report signals provides essential insight into the paper gold market's influence on spot prices and delivery dynamics.

Market Outlook and Investment Implications

The convergence of these seven drivers creates a uniquely supportive environment for gold prices that extends beyond typical cyclical factors. Unlike previous gold rallies driven primarily by single issues like inflation or currency crises, current conditions represent multiple, reinforcing trends that are likely to persist for extended periods.

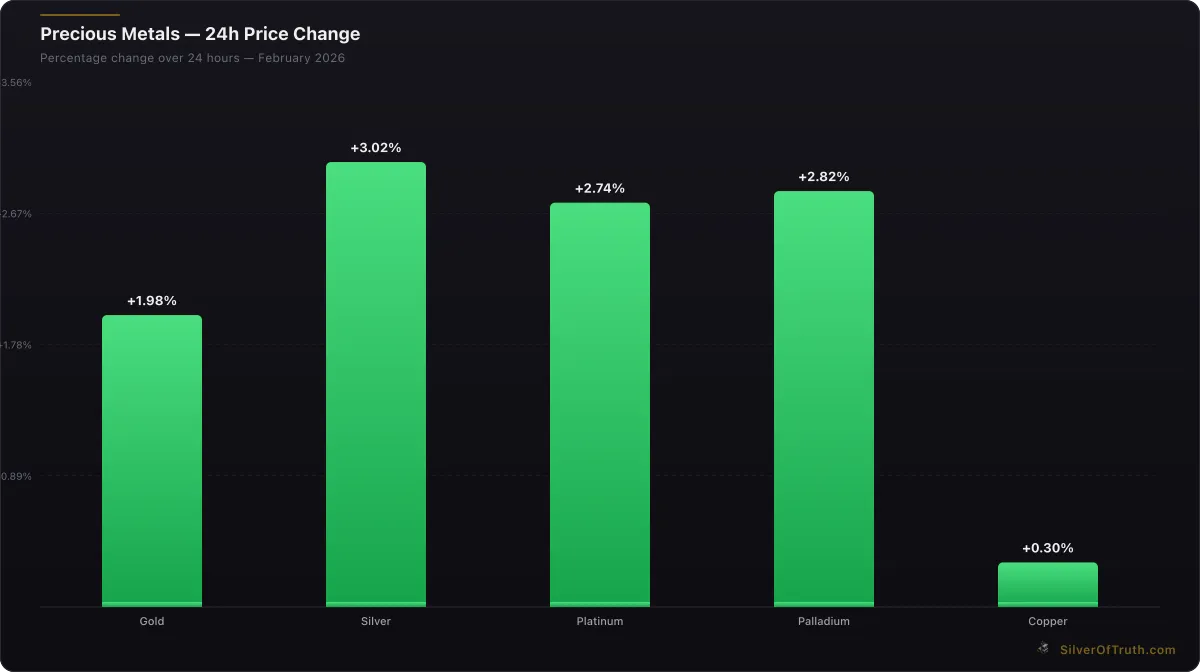

24-hour precious metals price changes. Source: SilverOfTruth, February 2026

The structural nature of many drivers—particularly central bank buying, geopolitical realignments, and supply constraints—suggests this gold cycle may have greater longevity than previous rallies. Historical analysis shows that gold bull markets driven by monetary system changes (like the 1970s dollar devaluation) tend to last longer and reach higher prices than those driven by temporary economic stress.

However, investors should recognize that gold's recent surge to $5,063 may include some speculative premium that could correct in the short term. The 2.33% single-day gain represents momentum that may not be sustainable without continued fundamental support from the underlying drivers.

For portfolio construction, the multiple supporting factors suggest gold allocations remain appropriate even at current elevated prices. Unlike single-factor rallies that require precise timing, the diverse driver set reduces timing risk for long-term holders while maintaining potential for further appreciation.

The key risk factors to monitor include Federal Reserve policy reversals, resolution of major geopolitical tensions, and significant new gold discoveries that could alter supply dynamics. However, the structural nature of most current drivers suggests these risks are lower probability than during previous gold cycles.

Track live COMEX inventory trends and precious metals positioning data with the SilverOfTruth app to stay informed of developing market dynamics that could affect gold's trajectory.

Frequently Asked Questions

What is driving gold prices to record highs in 2026?

Seven key factors are driving gold's rally to over $5,000 per ounce: Federal Reserve policy shifts lowering real interest rates, unprecedented central bank buying exceeding 1,000 tonnes annually, escalating geopolitical tensions creating safe-haven demand, persistent inflation pressures despite rate hikes, mining supply constraints with rising production costs, increased institutional portfolio adoption for diversification, and COMEX market tightness with inventory declining 4.76% monthly while coverage ratios compress.

How does Federal Reserve policy affect gold prices?

Gold prices are inversely correlated with real interest rates—when Fed policy creates lower inflation-adjusted returns on bonds and cash, gold becomes more attractive despite yielding no interest. Recent Fed communications suggesting potential rate hike pauses have reduced the opportunity cost of holding gold, while possibilities of renewed quantitative easing create currency debasement concerns that historically drive gold demand.

Why are central banks buying so much gold?

Central banks, particularly in emerging markets, are diversifying reserves away from dollar-heavy portfolios as a hedge against currency volatility and geopolitical risks. Countries like China, Russia, and India view gold as a strategic asset independent of Western financial systems. The pace of accumulation has accelerated even as prices reach multi-year highs, indicating conviction-based buying rather than opportunistic positioning.

Is gold still an effective inflation hedge at current prices?

Yes, gold maintains its inflation-hedging properties even at elevated prices because its effectiveness stems from maintaining purchasing power when real returns on bonds and cash turn negative. With core inflation remaining above central bank targets and currency debasement pressures from high government debt levels, gold continues serving its traditional role as a store of value independent of any single currency's purchasing power.

How do COMEX inventory levels affect gold prices?

COMEX registered inventory at 17.58 million ounces provides only 43.5% coverage against potential delivery obligations from open interest contracts. Monthly inventory depletion of 4.76% indicates consistent physical offtake, creating supply tightness that could lead to delivery squeezes if demand accelerates. The unusual situation where registered inventory exceeds eligible suggests metal is being positioned for withdrawal rather than storage, indicating underlying market stress.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, investment, or trading advice. Past performance is not indicative of future results. Always conduct your own research and consult with a qualified financial advisor before making investment decisions. SilverOfTruth provides market data and analysis tools — it does not provide personalized financial advice.