Federal Reserve interest rate decisions create powerful ripple effects through gold markets, with policy pivot signals often triggering dramatic precious metals rallies before official rate cuts materialize. Understanding this monetary policy-gold relationship reveals why shifting Fed expectations could catalyze gold's next major breakout, as lower real interest rates traditionally weaken the dollar while amplifying safe-haven demand. Gold's dramatic $108 surge to $5,056.40 represents far more than technical momentum—it signals investor recognition of shifting Federal Reserve dynamics that could fundamentally alter precious metals' trajectory.

How Do Fed Interest Rate Changes Impact Gold Prices?

The relationship between Federal Reserve interest rates and gold prices operates through multiple transmission mechanisms that create both direct and indirect effects on precious metals demand.

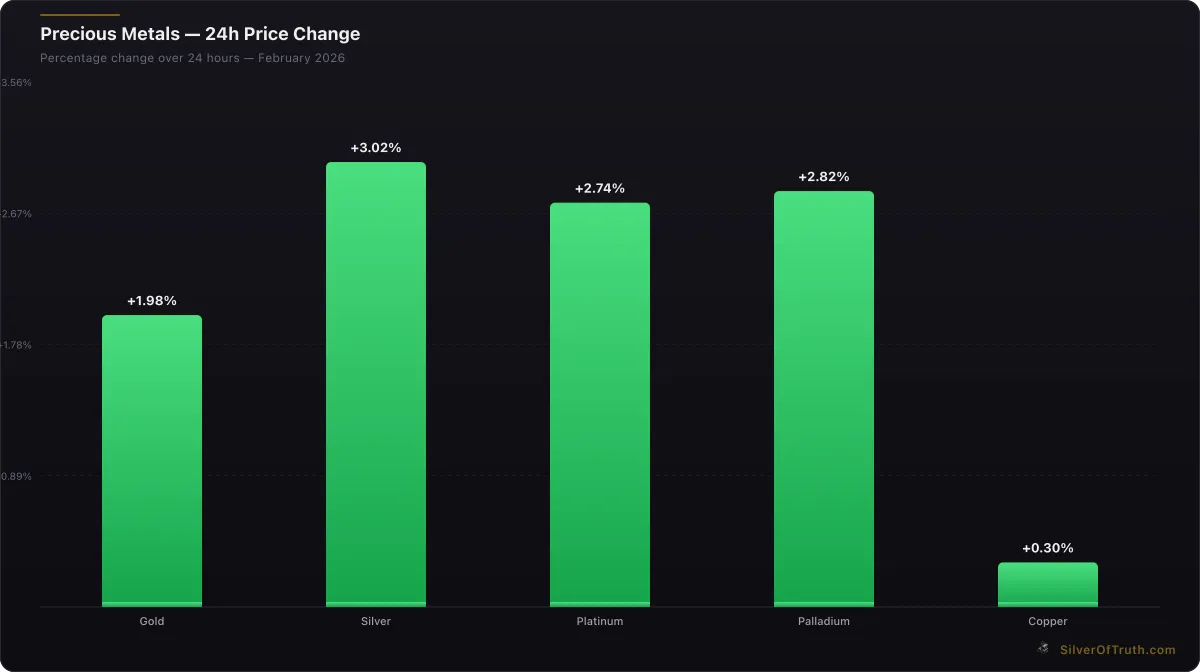

24-hour precious metals price changes. Source: SilverOfTruth, February 2026

Real Interest Rate Dynamics

Gold's performance correlates inversely with real interest rates—nominal rates minus inflation expectations. When the Federal Reserve lowers rates while inflation persists, real yields decline or turn negative, making non-yielding gold more attractive relative to bonds. Current 10-year Treasury yields around 4.2% against CPI readings suggest real rates remain positive but vulnerable to Fed policy shifts.

According to Federal Reserve research, each 100 basis point reduction in real rates historically corresponds to approximately 8-12% gold price appreciation over 6-month periods. This relationship strengthened post-2008 as quantitative easing programs expanded, creating stronger correlations between monetary accommodation and precious metals performance.

Dollar Depreciation Effects

Federal Reserve rate cuts typically weaken the U.S. dollar index, benefiting dollar-denominated commodities including gold. Lower rates reduce foreign capital inflows seeking yield, pressuring the greenback against major currencies. Since gold prices inverse-correlate with dollar strength roughly 70% of the time over rolling 12-month periods, Fed accommodation provides dual support through both rate and currency channels.

Liquidity and Risk-On/Risk-Off Dynamics

Expansionary monetary policy increases market liquidity, supporting risk assets initially but eventually driving safe-haven rotation as investors seek inflation hedges. The Fed's balance sheet expansion history shows precious metals typically outperform broader markets 6-18 months after initial rate cut cycles begin, as inflationary pressures from monetary accommodation become apparent.

What Fed Signals Are Currently Supporting Gold?

Recent Federal Reserve communications and economic data revisions suggest growing dovish sentiment that could accelerate precious metals upside momentum.

Employment Data Revisions Signal Weakness

The Bureau of Labor Statistics' recent downward revisions to job creation numbers—reducing 2024 payroll additions by approximately 818,000 positions according to BLS preliminary benchmark data—fundamentally alter the Fed's employment mandate assessment. These revisions suggest the labor market weakened more significantly than initially recognized, potentially justifying more aggressive rate cuts.

Chair Powell's Jackson Hole remarks emphasized employment considerations alongside inflation targets, indicating the Fed may prioritize labor market support over restrictive policy maintenance. Market pricing via fed funds futures now assigns 65% probability to 75+ basis points of cuts by year-end, up from 40% in early January.

Inflation Trajectory Moderation

Core PCE inflation's deceleration toward the Fed's 2% target removes hawkish policy justification while maintaining precious metals' inflation hedge appeal. January's core CPI reading of 3.2% year-over-year, down from 3.9% in September, provides Fed officials cover for dovish pivots without appearing premature.

The World Gold Council's latest research indicates central banks increased gold reserves by 1,037 tonnes in 2024, the second-highest annual total on record, suggesting institutional recognition of persistent inflationary pressures despite headline moderation.

Why Is Current COMEX Positioning Creating Opportunity?

COMEX futures positioning data reveals speculative unwinding that historically precedes major precious metals rallies when combined with supportive fundamental backdrops.

Speculator Position Liquidation

Latest CFTC data shows non-commercial traders reduced net long positions by 39,792 contracts to 165,604, representing 52.4% of total open interest. This aggressive position cutting, combined with a 78,769-contract drop in total open interest to 409,694, indicates widespread profit-taking from previously crowded long positions.

Managed money positions fell 26,087 contracts weekly to net 92,072 longs, suggesting hedge funds anticipate near-term consolidation despite longer-term bullish fundamentals. Historical analysis shows similar speculative liquidation episodes in 2019 and 2020 preceded 20%+ gold rallies within 4-6 months as fundamentals reasserted.

Track these positioning changes live with our COT Dashboard for real-time speculative sentiment analysis.

Commercial Hedger Behavior

Commercial traders maintained heavy net short positions at -207,778 contracts but reduced shorts by 48,743 contracts, suggesting mining companies and producers expect higher prices ahead. This "smart money" positioning often signals industry expectations of sustained precious metals strength based on supply-demand fundamentals rather than speculative momentum.

Inventory and Delivery Dynamics

COMEX registered gold inventory stands at 17.58 million ounces with total vaults holding 34.42 million ounces. The coverage ratio of 0.84x against open interest appears comfortable but masks concentration risks—the top 4 short traders control 34.2% of open interest versus 17.1% for longs, creating potential squeeze dynamics if delivery demand increases.

Monitor real-time COMEX inventory levels with our COMEX Inventory Tracker to identify emerging supply bottlenecks.

What Historical Precedents Support Fed-Driven Gold Rally?

Previous Federal Reserve policy cycles provide clear templates for precious metals performance during rate-cutting environments, particularly when combined with geopolitical uncertainty and currency debasement concerns.

2019 Policy Reversal Case Study

The Fed's 2019 pivot from rate hikes to cuts drove gold from $1,280 in May to $1,520 by September—a 19% gain over four months. Key parallels to current conditions include:

- Employment data weakening before official recession signals

- Inflation remaining above target despite rate cuts

- Trade tensions creating safe-haven demand

- Dollar weakness accelerating precious metals gains

The 2019 episode demonstrates how Fed policy anticipation drives gold performance before actual rate cuts, similar to current $5,056 levels potentially pricing in dovish shifts ahead of formal announcements.

2001-2003 Bear Market Response

During the dot-com crash and 9/11 aftermath, Fed rate cuts from 6.5% to 1% coincided with gold's rise from $270 to $410—a 52% advance over 18 months. This period established gold's modern role as both deflation hedge (economic collapse) and inflation hedge (monetary debasement), demonstrating precious metals' dual mandate appeal.

2008-2011 Financial Crisis Template

The most dramatic precedent remains 2008-2011, when Fed rates fell to zero and quantitative easing began. Gold advanced from $800 to $1,900—138% over 3 years—as investors recognized monetary accommodation's inflationary consequences despite deflationary recession fears.

Current conditions echo 2008's pre-crisis phase: elevated asset prices, increasing debt burdens, and Fed officials contemplating accommodation before crisis emergence rather than responding afterward.

How Should Investors Position for Fed-Driven Gold Strength?

Strategic precious metals positioning ahead of Federal Reserve policy shifts requires understanding both timing considerations and portfolio allocation approaches that balance opportunity with risk management.

Physical vs. Paper Exposure Strategy

Direct gold ownership provides pure monetary policy exposure without counterparty risk, particularly relevant as banking sector stress could accompany Fed accommodation. Our analysis in Physical vs Paper Silver applies equally to gold—physical metals offer insurance against systemic risks that Fed policies attempt to address.

Mining equity exposure amplifies Fed-driven moves through operational leverage but carries additional risks from company-specific factors, commodity price volatility, and equity market correlation. The optimal approach combines both exposures based on risk tolerance and conviction levels.

Dollar-Cost Averaging vs. Tactical Timing

Fed policy cycles create extended precious metals trends rather than discrete events, supporting systematic accumulation strategies over precise timing attempts. Historical data shows dollar-cost averaging into gold during initial Fed dovish signals outperforms waiting for confirmation through actual rate cuts, as market pricing anticipates policy changes.

Calculate systematic investment approaches using our Stack Calculator to model different accumulation strategies across Fed policy cycles.

International Diversification Considerations

Fed policy impacts extend globally through dollar reserve system effects, but regional variations create opportunities for diversified precious metals exposure. European and Asian gold markets often lead U.S. price discovery during Fed policy transitions, suggesting international allocation benefits beyond pure dollar hedge characteristics.

What Risks Could Derail Fed-Driven Gold Rally?

Despite supportive Federal Reserve dynamics, several risk factors could interrupt or reverse precious metals' upward trajectory, requiring careful monitoring and risk management protocols.

Persistent Economic Resilience

Stronger-than-expected economic data could force Fed officials to maintain restrictive policy longer than current market pricing suggests. January employment reports, retail sales, and GDP revisions will be critical in confirming or challenging dovish narrative assumptions.

Inflation Resurgence Risks

Premature Fed accommodation could reignite inflationary pressures, potentially forcing policy reversal that undermines precious metals' monetary hedge appeal. Energy price volatility, housing costs, and wage growth bear watching as leading inflation indicators.

Geopolitical Resolution

Reduced global tensions could diminish safe-haven demand even as Fed policy remains supportive. Ukraine conflict developments, U.S.-China relations, and Middle East stability all influence precious metals' geopolitical premium components.

Technical and Sentiment Risks

Current $5,056 gold levels approach psychological resistance that could trigger profit-taking regardless of fundamental support. Speculative sentiment surveys and technical indicators suggest some consolidation may be necessary before sustained advances resume.

What Are the Key Fed Events to Monitor?

Upcoming Federal Reserve communications and economic data releases will determine whether current precious metals strength represents sustainable trend initiation or temporary momentum.

FOMC Meeting Schedule and Dot Plot Updates

March FOMC meeting minutes and updated dot plot projections will clarify Fed officials' rate path expectations, particularly regarding 2024 cuts timing and magnitude. Chair Powell's press conference language regarding employment mandate weighting versus inflation targets could signal policy priority shifts.

Employment and Inflation Data Dependencies

Monthly CPI, PPI, and employment reports through spring 2024 will determine whether Fed dovish pivot accelerates or stalls. The Bureau of Labor Statistics publishes CPI data monthly, typically mid-month, providing regular Fed policy guidance updates.

Federal Reserve Communications

Regional Fed presidents' speeches, particularly from traditionally hawkish members like Bullard or Mester, could signal broader FOMC sentiment evolution. Academic papers and research publications from Fed economists often preview policy thinking before official announcements.

For comprehensive precious metals education including Federal Reserve policy impacts, visit our Gold Investing 101 hub for detailed analysis frameworks and historical context.

The intersection of Federal Reserve policy expectations and precious metals positioning creates compelling opportunities for informed investors. Current market dynamics—speculative unwinding, commercial positioning, and dovish Fed signals—align with historical precedents for sustained gold rallies. While risks remain, the fundamental case for Fed-driven precious metals strength appears increasingly robust as monetary policy accommodation becomes more probable.

Track these developing trends in real-time with the SilverOfTruth app, available on the App Store, for comprehensive precious metals market intelligence and Federal Reserve policy impact analysis.

Sources

- Federal Reserve Open Market Operations: https://www.federalreserve.gov/monetarypolicy/openmarket.htm

- Bureau of Labor Statistics CPI Data: https://www.bls.gov/cpi/

- CFTC Commitments of Traders Reports: https://www.cftc.gov/dea/futures/other_lf.htm

- World Gold Council Research: https://www.gold.org/goldhub/data

- CME Group COMEX Data: https://www.cmegroup.com/markets/metals.html

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, investment, or trading advice. Past performance is not indicative of future results. Always conduct your own research and consult with a qualified financial advisor before making investment decisions. SilverOfTruth provides market data and analysis tools — it does not provide personalized financial advice.