Standing for physical delivery on COMEX futures transforms paper contracts into real bars of gold and silver, yet most traders never navigate this process. Understanding how COMEX delivery works reveals the critical bridge between paper trading and physical precious metals ownership. This comprehensive guide walks you through every step of the delivery process—from initial notice to final vault receipt—explaining the procedures, costs, and requirements that turn futures contracts into tangible metal. Whether you're considering delivery or simply want to understand how the world's largest precious metals exchange operates, knowing these mechanics provides crucial insight into how paper and physical markets connect.

COMEX Contract Specifications for Delivery

COMEX precious metals futures contracts specify exact delivery requirements that both buyers and sellers must meet. A gold futures contract (GC) represents 100 troy ounces of gold with a minimum fineness of 995 parts per thousand. Silver contracts (SI) cover 5,000 troy ounces at 999 fineness minimum.

COMEX coverage ratios — lower values indicate higher delivery squeeze risk. Source: SilverOfTruth, February 2026

Gold Contract Delivery Specifications:

- Contract size: 100 troy ounces

- Minimum fineness: 995 parts per thousand

- Deliverable brands: LBMA Good Delivery bars or equivalent

- Weight tolerance: +/- 5% allowed

- Assay requirements: Must meet exchange standards

Silver Contract Delivery Specifications:

- Contract size: 5,000 troy ounces

- Minimum fineness: 999 parts per thousand

- Deliverable forms: 1,000 oz bars (5 bars per contract)

- Weight tolerance: +/- 6% allowed

- Brand requirements: Exchange-approved refiners only

The exchange maintains strict quality standards through approved assayers and refiners. Only bars meeting COMEX delivery specifications qualify for settlement. This ensures consistent quality across all delivered metal, supporting market confidence in the physical settlement process.

The Five-Day Delivery Process

COMEX delivery operates on a precise five-day schedule within the contract's delivery month. This standardized timeline coordinates activities between long holders seeking metal, short holders providing it, and approved warehouses storing inventory.

First Notice Day

The delivery process begins on First Notice Day, typically the first business day of the delivery month. Short position holders must decide by 8:00 PM CT whether to deliver against their contracts. Those choosing delivery file an "Intention to Deliver" notice with the clearing firm.

During this phase, longs maintain full flexibility. They can offset positions until the Position Day deadline, avoiding delivery if market conditions or personal circumstances change. However, longs planning to take delivery should ensure adequate margin and prepare for the multi-day process ahead.

Last Trading Day

Last Trading Day marks the final opportunity for position holders to trade out of delivery obligations. This day typically falls on the third-to-last business day of the delivery month. After the close, remaining positions automatically enter the delivery process.

Market dynamics often shift dramatically around Last Trading Day. Participants unwilling or unable to make or take delivery exit positions, sometimes creating price volatility as the remaining players sort out physical settlement logistics.

Position Day

Position Day occurs one business day after Last Trading Day. By 2:00 PM CT, the exchange matches long and short positions for delivery. Clearing firms receive notifications identifying which customers will participate in delivery.

The matching process follows exchange algorithms considering factors like warehouse location, metal availability, and clearing firm preferences. This systematic approach prevents manipulation while ensuring efficient physical settlement across COMEX's warehouse network.

Notice Day

On Notice Day, short position holders issue formal delivery notices through their clearing firms. These notices specify the warehouse location, metal quantities, and other delivery details. Longs receive notice assignments, learning where and how much metal they will receive.

Delivery notices become binding obligations. Shorts must deliver the specified metal, while longs must accept and pay for it. The exchange's clearinghouse guarantees performance, protecting both parties from counterparty risk throughout the settlement process.

Delivery Day

The final step occurs on Delivery Day when physical transfer happens. Warehouse receipts change hands, representing legal ownership of specific metal bars stored in approved facilities. Payment flows from buyer to seller through the clearinghouse, completing the transaction.

Warehouse receipts function as bearer instruments—whoever holds the receipt owns the metal. These documents specify exact bar numbers, weights, and assays, enabling precise tracking of individual pieces through the delivery system.

COMEX Approved Warehouses and Storage

The delivery process relies on COMEX's network of approved warehouses strategically located near major transportation hubs. These facilities must meet stringent security, insurance, and operational standards to maintain exchange approval.

Major COMEX Warehouse Locations:

| Facility | Location | Metals Stored | Security Features | |----------|-----------|---------------|-------------------| | Brink's | New York, Delaware | Gold, Silver, Platinum, Palladium | 24/7 armed guards, vault construction | | Delaware Depository | Delaware | Gold, Silver | Underground vaults, multiple access controls | | HSBC USA | New York | Gold, Silver | Bank-grade security, segregated storage | | JP Morgan Chase | New York | Gold, Silver | Integrated clearing, institutional access | | Manfra, Tordella & Brookes | New York | Gold, Silver, Platinum | Specialized precious metals handling | | Scotia Mocatta | New York | Gold, Silver | Canadian bank subsidiary, global network |

Each warehouse maintains separate "registered" and "eligible" inventory categories. Registered metal is specifically warranted for delivery against futures contracts and immediately available for settlement. Eligible inventory represents exchange-quality metal owned by warehouse customers but not designated for delivery.

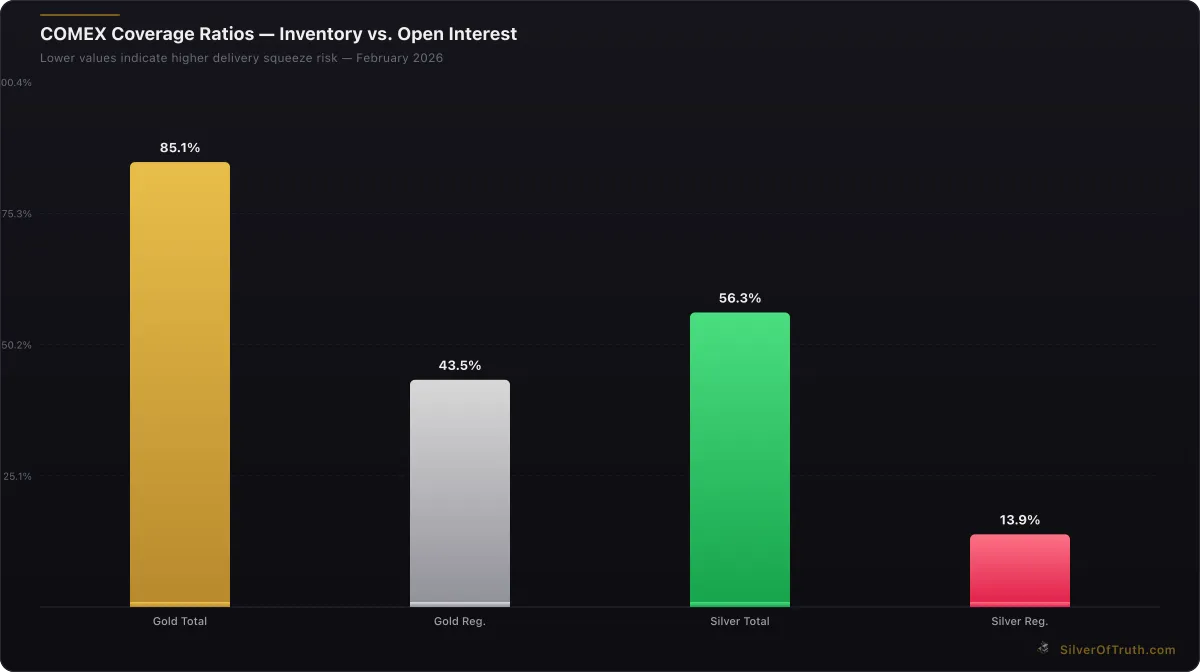

Understanding current COMEX inventory levels helps assess delivery availability. With registered gold at 17.58 million ounces covering 43.5% of open interest, delivery capacity remains adequate but not excessive. Silver's 92.9 million registered ounces provide 13.9% coverage against open interest, indicating tighter physical conditions.

Delivery Costs and Practical Considerations

Taking delivery involves multiple costs beyond the contract's futures price. These expenses include warehouse storage fees, transportation costs, insurance, and administrative charges that can significantly impact the total cost of acquiring physical metal.

Typical COMEX Delivery Costs:

- Warehouse charges: $0.60-$1.20 per ounce annually for storage

- Delivery fees: $50-$150 per contract for transfer services

- Transportation: $200-$500 for armored car service to personal vaults

- Insurance: 0.1-0.3% of metal value during transport

- Documentation: $25-$75 for warehouse receipt processing

- Assay verification: $100-$300 if bars require re-assaying

These costs often exceed retail premiums for comparable physical metal, making COMEX delivery economically viable primarily for large-scale transactions. Individual investors typically find better value purchasing from bullion dealers offering competitive premiums and smaller minimum quantities.

Storage represents an ongoing expense. Warehouse fees accumulate daily, making extended storage expensive. Many delivery takers arrange prompt removal to private vaults or secure storage facilities offering lower long-term rates.

Who Typically Takes COMEX Delivery

Despite common perceptions, retail investors rarely take COMEX delivery. The process suits institutional participants with specific operational requirements and sufficient scale to justify the associated costs and complexity.

Primary Delivery Participants:

- Refiners and processors: Acquiring raw material for production operations

- Large dealers: Building inventory for retail distribution networks

- Industrial users: Electronics, jewelry, and manufacturing companies needing bulk metal

- ETF sponsors: Physical-backed funds requiring vault metal for creation units

- Arbitrageurs: Exploiting price spreads between physical and futures markets

- Sovereign entities: Central banks and government agencies accumulating reserves

Commercial operations dominate delivery activity because they possess infrastructure for handling, storing, and processing large metal quantities. These entities also maintain established relationships with approved warehouses and transportation providers, reducing logistical complexity.

Retail investors interested in physical precious metals generally achieve better outcomes through specialized bullion dealers. These vendors offer smaller quantities, competitive premiums, and convenient delivery options better suited for individual ownership. Our guide to physical vs paper silver explores alternatives for retail investors.

Registered vs Eligible Inventory Impact

The distinction between registered and eligible inventory critically affects delivery availability and market dynamics. Understanding these categories reveals supply constraints that influence futures pricing and delivery timing.

Source: SilverOfTruth COMEX data, February 2026

Registered inventory represents metal specifically warranted for delivery against futures contracts. Warehouse operators have completed all paperwork, assays, and legal requirements necessary for immediate settlement. This metal stands ready for delivery notices and forms the backbone of COMEX's physical settlement system.

Eligible inventory consists of exchange-quality metal stored in approved warehouses but not designated for delivery. Owners may convert eligible to registered status by completing warrant procedures, but this process takes time and isn't guaranteed. Some owners prefer keeping metal eligible to avoid potential delivery obligations.

Current data shows unusual patterns in the gold market, where registered inventory (17.58M oz) slightly exceeds eligible holdings (16.84M oz). This inversion from typical patterns suggests either recent conversions from eligible to registered or significant eligible metal withdrawals. Either scenario indicates tightening physical supply conditions.

Silver inventory displays more traditional patterns with eligible (283.5M oz) substantially exceeding registered (92.9M oz). However, the registered coverage ratio of only 13.9% against open interest creates potential delivery squeeze conditions if demand increases or inventory declines further.

For detailed analysis of these inventory dynamics, review our comprehensive guide to registered vs eligible inventory. These metrics provide crucial insight into physical market stress and delivery capacity constraints.

Alternative Physical Acquisition Methods

While COMEX delivery remains the institutional standard for large-scale physical acquisition, individual investors typically benefit from alternative approaches offering better economics and convenience.

Bullion Dealers: Specialized precious metals dealers offer competitive premiums, smaller minimum orders, and flexible delivery options. Established dealers like APMEX, JM Bullion, and SD Bullion provide extensive product selections with transparent pricing and reliable service.

Physical ETFs: Exchange-traded funds like SPDR Gold Shares (GLD) and iShares Silver Trust (SLV) offer exposure to physical metal without storage requirements. While not providing direct ownership, these funds maintain allocated metal backing their shares.

Allocated Storage Programs: Companies like BullionVault and GoldMoney enable fractional ownership of professionally stored metal. These services provide allocated storage at lower costs than COMEX warehouses while maintaining individual ownership rights.

Local Coin Shops: Regional dealers often offer competitive pricing and personal service for smaller transactions. Establishing relationships with reputable local dealers provides ongoing access to physical metal with minimal transaction costs.

Precious Metals IRAs: Self-directed retirement accounts enable tax-advantaged precious metals ownership through approved custodians. This approach combines physical ownership with retirement planning benefits.

Each alternative serves different needs and investment scales. Our silver stacking guide provides detailed comparison of these options for beginning investors.

Delivery Notice Trends and Market Signals

Monthly delivery statistics provide valuable insights into physical demand and market structure. Tracking delivery notices, issues, and stops reveals underlying supply-demand dynamics affecting futures pricing.

February 2026 data shows 35,850 gold contracts delivered month-to-date, representing balanced activity between issues and stops. This equilibrium suggests steady commercial demand without acute physical stress or unusual arbitrage opportunities.

Historical patterns reveal delivery activity peaks during specific months. December traditionally sees elevated gold deliveries as jewelry manufacturers build inventory for holiday seasons. March and September often show increased silver deliveries coinciding with industrial demand cycles.

Key Delivery Metrics to Monitor:

- Total notices issued: Indicates short seller delivery intentions

- Notices stopped: Shows long holder acceptance of physical metal

- Redeliveries: Metal changing hands within warehouse system

- Net withdrawals: Metal leaving COMEX warehouses entirely

- Stopage rates: Percentage of notices actually delivered

Unusual delivery patterns often signal market stress or opportunity. Delivery notices exceeding normal seasonal patterns suggest strong physical demand or supply constraints. Conversely, below-normal delivery activity may indicate weak physical fundamentals or abundant supply.

Market participants closely monitor delivery trends through CME Group's daily reports. These documents provide transparency into physical settlement activity supporting informed trading decisions.

Risk Management and Delivery Obligations

Futures positions approaching delivery month require careful risk management to avoid unintended delivery obligations. Both long and short holders face specific risks requiring proactive management strategies.

Long Position Risks:

- Unexpected delivery assignment requiring immediate payment

- Storage and insurance obligations for received metal

- Market timing risk if unable to liquidate physical holdings quickly

- Credit requirements for margin and delivery payments

Short Position Risks:

- Inability to source deliverable metal meeting exchange specifications

- Warehouse scheduling delays preventing timely delivery

- Quality failures requiring expensive reprocessing or replacement

- Opportunity costs from tying up capital in physical inventory

Professional traders employ several strategies to manage delivery risk:

Position Rolling: Moving positions to later delivery months before First Notice Day avoids immediate delivery obligations while maintaining market exposure.

Spread Trading: Simultaneously buying and selling different delivery months creates neutral delivery exposure while capturing price relationships.

Physical Hedging: Maintaining warehouse inventory to cover short positions ensures delivery capability without last-minute sourcing.

Credit Management: Ensuring adequate margin and cash availability prevents forced liquidation during delivery periods.

Understanding COT report positioning helps assess market-wide delivery risk. High speculative positioning combined with declining inventory creates potential squeeze conditions requiring defensive positioning.

Technology and Modern Delivery Infrastructure

COMEX delivery operations leverage modern technology to ensure accurate, secure, and efficient physical settlement. Electronic systems track every step from delivery notice through final warehouse receipt transfer.

Digital Warehouse Receipts: Electronic documentation replaces paper certificates, enabling faster transfers and reducing fraud risk. Digital receipts contain encrypted authentication preventing counterfeiting while speeding settlement.

Automated Matching: Computer algorithms optimize delivery assignments considering warehouse locations, metal availability, and participant preferences. This systematic approach prevents manipulation while maximizing efficiency.

Real-time Inventory Tracking: Continuous monitoring of warehouse stocks provides current availability data supporting delivery planning. Market participants access this information through CME Group's data services.

Integrated Settlement: Electronic funds transfer coordinates with physical delivery ensuring simultaneous exchange of payment and ownership. This integration reduces counterparty risk and settlement failures.

Audit Trails: Comprehensive transaction logging creates permanent records of all delivery activity. These records support regulatory compliance and dispute resolution when necessary.

Modern infrastructure makes COMEX delivery more reliable and efficient than historical systems. However, the fundamental process remains unchanged—converting paper contracts into physical ownership of precious metals stored in secure warehouse facilities.

Frequently Asked Questions

How long does COMEX delivery take from start to finish?

The standard COMEX delivery process takes five business days from First Notice Day to final settlement. However, planning for delivery should begin earlier since positions can't be easily exited once the delivery period starts. Preparation including credit arrangements and storage planning should occur weeks before the delivery month.

What are the minimum quantities for taking COMEX delivery?

Gold delivery requires taking delivery of complete 100-ounce contracts, while silver contracts represent 5,000 ounces each. Partial contract delivery isn't possible, making COMEX settlement suitable primarily for large-scale transactions. Retail investors typically find bullion dealers offer more flexible quantities.

Can individual investors realistically take COMEX delivery?

While technically possible, individual investors rarely benefit from COMEX delivery due to high minimum quantities, substantial costs, and complex logistics. The process suits institutional participants with appropriate scale and infrastructure. Retail investors generally achieve better economics through specialized precious metals dealers.

What happens if registered inventory becomes insufficient for delivery demands?

COMEX maintains procedures for handling delivery squeezes including encouraging eligible-to-registered conversions, facilitating cash settlements, and temporarily raising margin requirements. However, severe inventory shortages could force delivery delays or alternative settlement arrangements. Current registered coverage ratios provide early warning of potential stress.

Are COMEX-delivered bars easily resellable to dealers?

COMEX bars meet international standards and are generally accepted by major dealers, though retail premiums may be lower than popular retail products. The large bar sizes (100 oz gold, 1,000 oz silver) suit institutional rather than retail transactions. Individual investors often prefer smaller denominations offering better resale flexibility.

Track live COMEX delivery data and inventory levels with SilverOfTruth's comprehensive precious metals dashboard — available on the App Store for real-time market intelligence.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, investment, or trading advice. Past performance is not indicative of future results. Always conduct your own research and consult with a qualified financial advisor before making investment decisions. SilverOfTruth provides market data and analysis tools — it does not provide personalized financial advice.