Which companies control the world's silver supply? With silver trading at $77.27 per ounce and industrial demand surging across 5G technology and electric vehicles, understanding the top silver producers becomes crucial for investors navigating today's precious metals landscape.

The global silver mining industry faces unprecedented challenges in 2026. Silver mine supply is declining while industrial applications expand rapidly, creating supply-demand imbalances that favor established producers with low-cost operations and expansion capabilities.

Global Silver Production Overview

The silver mining industry operates fundamentally differently from gold mining. While gold miners typically focus exclusively on gold extraction, most silver comes as a byproduct from base metal operations—zinc, lead, and copper mines. This structure means silver supply often depends on demand for other metals, creating unique market dynamics.

According to the Silver Institute, global mine production reached approximately 822 million ounces in 2025, with the top 10 producers accounting for roughly 60% of total output. Mexico leads global production, followed by Peru and China, but individual companies present a more complex hierarchy based on operational efficiency and reserve quality.

Primary vs. Byproduct Silver Production

Understanding the distinction between primary and byproduct silver production is essential when evaluating silver producers:

- Primary silver miners extract silver as their main product, offering pure exposure to silver price movements

- Byproduct producers extract silver alongside base metals, providing cost advantages but diluted silver exposure

- Mixed operations combine both approaches, balancing exposure with operational efficiency

This distinction significantly impacts how these companies respond to silver price changes and their strategic value for precious metals investors.

Top Silver Producers by Output

1. Fresnillo PLC (FNLPF)

Fresnillo stands as the world's largest primary silver producer, operating exclusively in Mexico with mines including Fresnillo, Herradura, and Noche Buena. The company produced approximately 53.1 million ounces of silver in 2025, maintaining its position as the industry leader.

Key Metrics:

- 2025 Production: 53.1 million oz silver

- AISC: $11.50-$13.20 per oz (estimated)

- Reserves: 1.3 billion oz silver equivalent

- Geographic Focus: Mexico (100%)

Fresnillo's advantage lies in its dedicated silver focus and extensive Mexican operations. The company benefits from Mexico's rich silver deposits and established mining infrastructure, though it faces challenges from increasing operational costs and regulatory pressures.

2. Pan American Silver Corp (PAAS)

Pan American Silver operates diversified operations across the Americas, producing approximately 25.8 million ounces in 2025. The company combines primary silver mines with byproduct operations, providing balanced exposure to silver markets.

Key Metrics:

- 2025 Production: 25.8 million oz silver

- AISC: $14.80-$16.50 per oz (estimated)

- Reserves: 350 million oz silver equivalent

- Geographic Focus: Peru, Bolivia, Mexico, Argentina

The company's strength lies in geographic diversification and operational efficiency across multiple jurisdictions. Recent acquisitions have expanded its asset base, though integration challenges and political risks in South American operations require careful monitoring.

3. Hecla Mining Company (HL)

Hecla represents the largest silver producer in the United States, with operations spanning Idaho, Alaska, and Mexico. The company produced approximately 13.2 million ounces in 2025, focusing on high-grade deposits and operational efficiency.

Key Metrics:

- 2025 Production: 13.2 million oz silver

- AISC: $15.20-$17.00 per oz (estimated)

- Reserves: 180 million oz silver equivalent

- Geographic Focus: USA (70%), Mexico (30%)

Hecla's competitive advantage stems from its U.S. operational base, providing political stability and regulatory predictability. The company's Greens Creek mine in Alaska consistently ranks among the world's lowest-cost silver operations.

4. First Majestic Silver Corp (AG)

First Majestic operates exclusively in Mexico, producing approximately 12.8 million ounces in 2025. The company focuses on primary silver production with multiple operations providing operational diversification within Mexico.

Key Metrics:

- 2025 Production: 12.8 million oz silver

- AISC: $16.50-$18.20 per oz (estimated)

- Reserves: 250 million oz silver equivalent

- Geographic Focus: Mexico (100%)

The company emphasizes vertical integration and direct sales to end-users, potentially capturing higher margins than traditional producers. However, this strategy also exposes First Majestic to operational complexity and market timing risks.

5. SSR Mining Inc (SSRM)

SSR Mining operates diversified precious metals operations, with silver production of approximately 8.9 million ounces in 2025. The company balances silver and gold production across North and South American operations.

Key Metrics:

- 2025 Production: 8.9 million oz silver

- AISC: $13.80-$15.60 per oz (estimated)

- Reserves: 95 million oz silver equivalent

- Geographic Focus: USA, Canada, Argentina

SSR Mining's strength lies in operational excellence and disciplined capital allocation. The company maintains conservative balance sheet management while pursuing strategic growth opportunities in established mining jurisdictions.

Byproduct Silver Producers

Major Base Metal Miners

Several large base metal producers contribute significantly to global silver supply through byproduct extraction:

Glencore PLC extracts substantial silver from zinc and lead operations, contributing approximately 35-40 million ounces annually to global supply. The company's integrated trading operations provide additional market insights and hedging capabilities.

BHP Group produces silver as a byproduct from copper operations, particularly at its Escondida mine in Chile. Annual silver production approximates 20-25 million ounces, though silver represents a minimal portion of total revenues.

Newmont Corporation generates silver byproduct from gold operations worldwide, producing approximately 15-18 million ounces annually. The company's operational scale and technical expertise create operational efficiencies benefiting silver production costs.

These byproduct producers often achieve lower all-in sustaining costs for silver due to shared operational expenses with primary metals. However, their silver production depends on base metal demand and operational decisions prioritizing other commodities.

Production Costs and AISC Analysis

All-In Sustaining Costs (AISC) provide crucial metrics for evaluating silver producer competitiveness. Current AISC levels across the industry range from $11-$22 per ounce, with significant variations based on operational scale, ore grades, and geographic factors.

Low-Cost Producers (AISC Below $15/oz)

Companies achieving AISC below $15 per ounce typically benefit from:

- High-grade ore deposits

- Byproduct revenues from other metals

- Operational scale advantages

- Established infrastructure

These producers maintain profitability even during silver price weakness and generate substantial cash flows during favorable market conditions like the current $77.27 silver environment.

Mid-Cost Producers (AISC $15-$18/oz)

The majority of primary silver producers operate within this cost range, balancing:

- Reasonable ore grades

- Geographic diversification

- Operational efficiency initiatives

- Capital allocation discipline

These companies remain profitable at current silver prices but face margin pressure during market downturns.

High-Cost Producers (AISC Above $18/oz)

Higher-cost operations typically reflect:

- Lower ore grades requiring higher processing volumes

- Remote locations increasing transportation costs

- Regulatory challenges in certain jurisdictions

- Operational inefficiencies or integration challenges

While vulnerable during price weakness, these producers can generate significant leverage during silver bull markets.

Reserve Quality and Mine Life

Reserve quality significantly impacts long-term producer viability. Key considerations include:

Measured and Indicated Resources

Established reserves with high confidence levels provide operational predictability and expansion optionality. Companies with substantial measured and indicated resources can plan long-term operational strategies and attract financing for expansion projects.

Ore Grade Trends

Industry-wide ore grade decline creates ongoing challenges for silver producers. Companies maintaining higher grades through exploration success or operational efficiency gain competitive advantages as processing costs increase across the industry.

Mine Life Extensions

Producers with exploration capabilities and reserve expansion potential provide better long-term investment value. Companies like Fresnillo and Hecla consistently expand reserves through systematic exploration programs.

Understanding how to evaluate these factors is crucial for investors, as detailed in our guide to evaluating mining stocks, which covers reserve analysis, cost structures, and operational metrics essential for mining stock investment decisions.

Geographic Distribution and Political Risk

Silver production concentrates in specific regions, creating geographic risk factors investors must consider:

Mexico - Leading Production Hub

Mexico accounts for approximately 23% of global silver production, hosting operations from Fresnillo, First Majestic, Hecla, and numerous other producers. The country's advantages include:

- Extensive silver mineralization

- Established mining infrastructure

- Skilled workforce

- Regulatory framework supporting mining

However, recent policy changes and environmental regulations create ongoing uncertainty for Mexican operations.

Peru - Major South American Producer

Peru contributes roughly 13% of global production, primarily through operations from Pan American Silver and other international miners. Benefits include rich mineral deposits and mining-friendly policies, though political instability occasionally impacts operations.

United States - Stable but Limited

U.S. production provides political stability but represents only about 3% of global output. Hecla's domestic operations benefit from regulatory predictability and infrastructure access, though higher operational costs limit competitiveness.

China - Domestic Focus

China produces significant silver primarily for domestic consumption. Limited export availability means Chinese production has minimal impact on international markets, though domestic demand growth affects global supply-demand balances.

Growth Strategies and Expansion Plans

Top silver producers pursue various growth strategies to expand production and improve operational efficiency:

Organic Growth Through Exploration

Companies like Fresnillo and Pan American Silver invest heavily in exploration programs to extend mine lives and discover new deposits. This approach provides long-term growth potential while maintaining operational control.

Strategic Acquisitions

Consolidation continues across the silver mining sector as larger producers acquire smaller operations to achieve scale advantages. Recent examples include Pan American Silver's acquisition activities and SSR Mining's strategic portfolio optimization.

Operational Efficiency Improvements

Producers focus on cost reduction through:

- Technology implementation

- Process optimization

- Energy efficiency initiatives

- Waste reduction programs

These improvements become increasingly important as ore grades decline industry-wide.

Vertical Integration

Some producers like First Majestic pursue vertical integration strategies, controlling more of the value chain from mining through refining and sales. While potentially increasing margins, this approach also increases operational complexity and capital requirements.

Impact of Industrial Demand Growth

Silver's industrial applications create unique demand dynamics affecting producer strategies and valuations. With industrial silver demand growing in 2026, producers benefit from fundamental demand growth beyond investment demand.

Technology Sector Demand

Growing applications in 5G technology, electric vehicles, and solar panels create sustained industrial demand supporting silver prices. This industrial demand provides fundamental support for silver producers beyond traditional precious metals investment demand.

Supply-Demand Imbalances

The silver supply deficit creates favorable conditions for efficient producers. Companies with low-cost operations and expansion capabilities can benefit from sustained higher silver prices driven by fundamental supply constraints.

Environmental and ESG Considerations

Environmental, Social, and Governance (ESG) factors increasingly impact silver producer operations and access to capital:

Environmental Compliance

Mining operations face stricter environmental regulations worldwide. Producers investing in cleaner technologies and sustainable practices gain operational advantages and improved access to financing.

Social License to Operate

Community relations and stakeholder engagement affect operational continuity. Companies maintaining positive relationships with local communities reduce operational risks and expansion barriers.

Governance Standards

Corporate governance standards impact investor confidence and capital access. Producers with strong governance frameworks attract institutional investment and achieve higher valuations.

Market Positioning in Current Environment

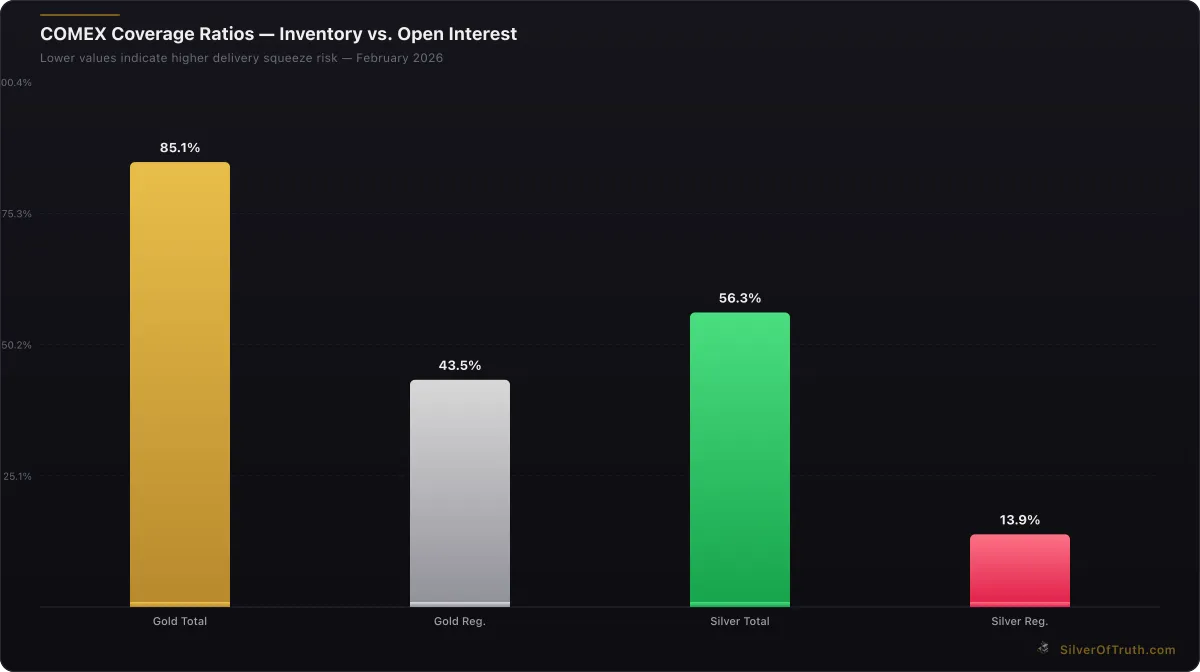

With silver at $77.27 and strong industrial demand growth, top silver producers benefit from favorable market conditions. The current COMEX silver inventory situation, showing declining registered stocks and high coverage ratios, creates additional support for silver prices benefiting all producers.

Source: SilverOfTruth COMEX data, February 2026

COMEX coverage ratios — lower values indicate higher delivery squeeze risk. Source: SilverOfTruth, February 2026

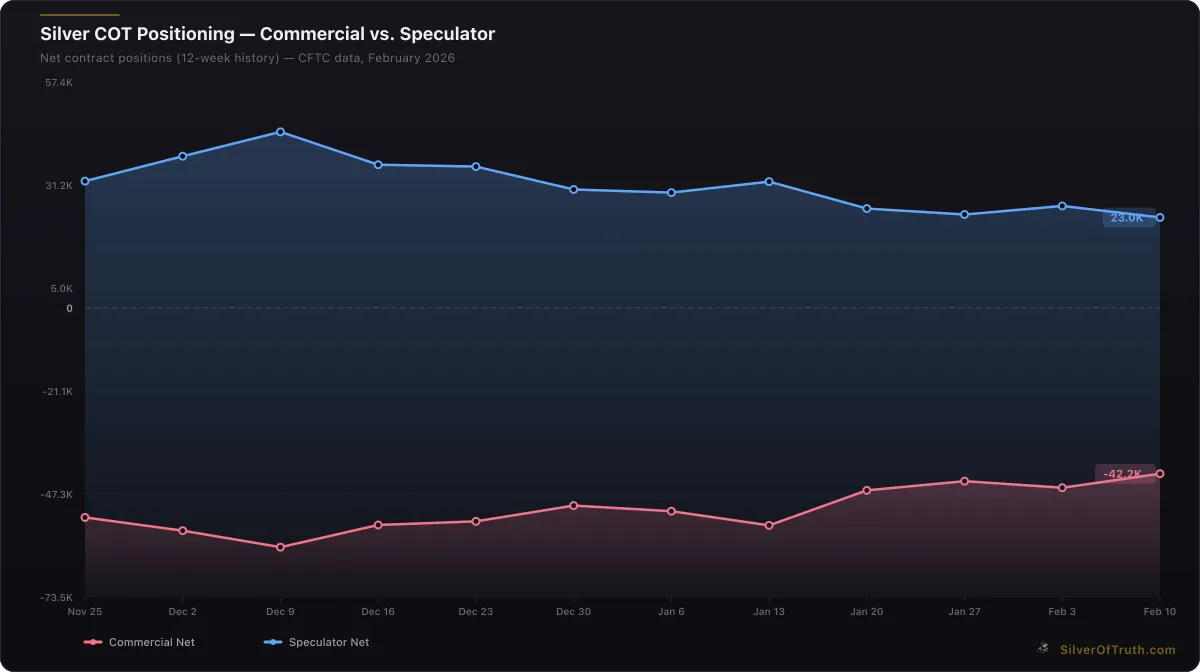

Silver COT positioning: commercial hedgers (red) vs. speculators (blue). Source: CFTC via SilverOfTruth, February 2026

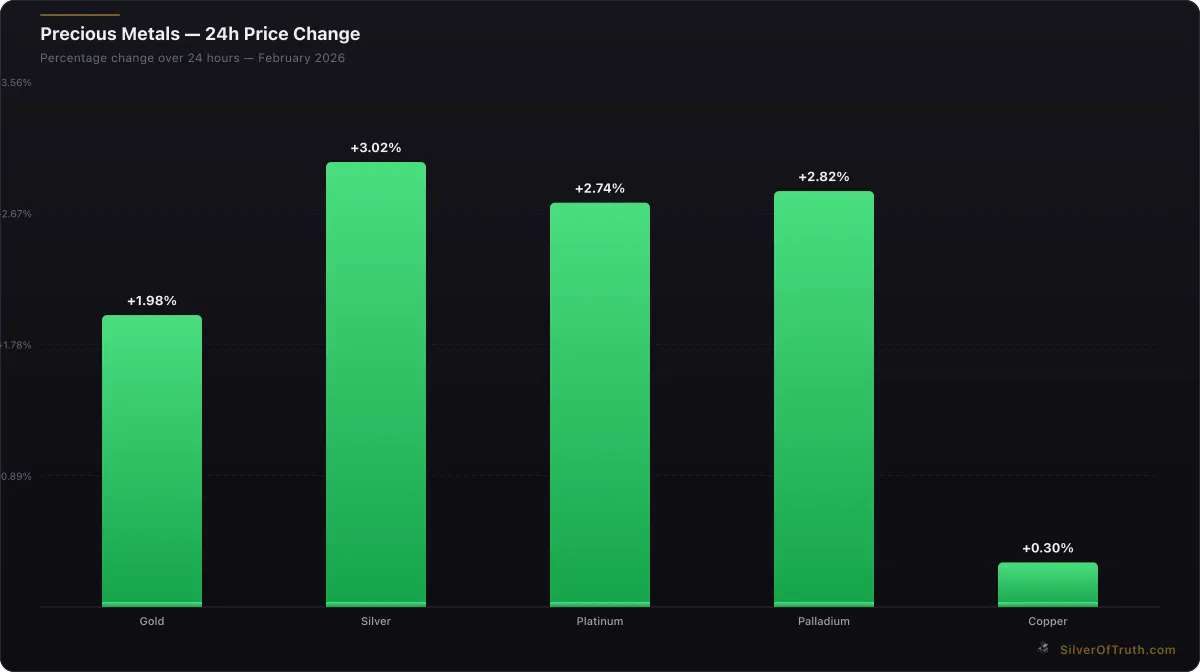

24-hour precious metals price changes. Source: SilverOfTruth, February 2026

However, producers must balance current favorable conditions with long-term operational sustainability. Companies focusing on operational excellence, cost control, and strategic growth position themselves for success across various market cycles.

Understanding the differences between physical vs paper silver helps investors appreciate how mining stocks provide exposure to silver markets while maintaining operational and strategic risks distinct from physical metal ownership.

Investment Considerations

When evaluating silver producers for investment consideration, key factors include:

Production Growth Trajectory

Companies demonstrating consistent production growth through operational efficiency improvements and strategic expansion provide superior investment potential compared to declining producers.

Cost Structure Sustainability

Producers maintaining competitive AISC levels while investing in operational improvements and exploration programs offer better long-term value than companies focusing solely on short-term cost cutting.

Balance Sheet Strength

Financial stability becomes crucial during commodity cycles. Companies maintaining conservative leverage levels and strong cash flow generation can pursue growth opportunities while managing operational risks.

Management Quality

Experienced management teams with successful track records of operational excellence and strategic execution provide competitive advantages in challenging operating environments.

FAQ Section

What makes a silver producer "top-tier" in the industry?

Top-tier silver producers typically combine several characteristics: annual production exceeding 10 million ounces, AISC below $16 per ounce, substantial reserves supporting 10+ year mine lives, operational excellence with consistent production guidance achievement, and strong balance sheets enabling strategic flexibility. Companies like Fresnillo and Pan American Silver exemplify these characteristics through consistent operational performance and strategic positioning.

How do byproduct silver producers compare to primary silver miners for investors?

Byproduct producers often achieve lower AISC due to shared operational costs with base metals, providing better margins during challenging silver markets. However, primary silver miners offer purer exposure to silver price movements and typically prioritize silver production optimization. Byproduct producers may reduce silver output if base metal economics improve, while primary miners focus consistently on silver production maximization. Investment choice depends on desired silver exposure level and risk tolerance.

Which geographic regions offer the best combination of silver resources and operational stability?

Mexico provides the richest silver deposits and established mining infrastructure but faces increasing regulatory uncertainty. The United States offers maximum political stability but limited high-grade deposits and higher operational costs. Peru combines good silver resources with mining-friendly policies but carries political risks. Canada provides excellent stability and regulatory frameworks but fewer world-class silver deposits. Diversified producers operating across multiple jurisdictions often provide optimal risk-adjusted exposure.

How do rising operational costs affect silver producer competitiveness?

Rising costs from inflation, energy price increases, and labor shortages pressure all producers, but impact varies significantly. Low-grade operations face disproportionate cost pressures as processing expenses increase, while high-grade producers maintain competitive advantages. Companies with operational scale, established infrastructure, and efficiency improvement programs better manage cost inflation. Producers unable to maintain competitive AISC levels risk operational curtailment or asset divestiture during challenging market conditions.

What role does exploration success play in silver producer valuations?

Exploration success provides long-term value through reserve replacement and mine life extensions, crucial for maintaining production levels as existing deposits deplete. Companies consistently replacing reserves through exploration maintain operational sustainability and growth optionality. Successful exploration programs also provide acquisition targets and joint venture opportunities, enhancing strategic flexibility. However, exploration requires sustained capital investment with uncertain returns, making execution quality critical for value creation versus capital destruction.

Track the performance of top silver producers with real-time mining stock analysis in the SilverOfTruth app — available on the App Store.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, investment, or trading advice. Past performance is not indicative of future results. Always conduct your own research and consult with a qualified financial advisor before making investment decisions. SilverOfTruth provides market data and analysis tools — it does not provide personalized financial advice.