Electric vehicles represent one of the most significant drivers of future silver demand, yet many investors underestimate the scale of this industrial transformation. While a conventional gasoline car contains roughly 15-28 grams of silver, modern electric vehicles require 25-50 grams per vehicle—nearly double the amount. With global EV sales projected to reach 30 million units by 2030, this sector alone could consume 750-1,500 metric tons of silver annually, equivalent to 2-4% of total global mine production.

The silver content differential stems from EVs' fundamental reliance on electrical systems where silver's unmatched conductivity becomes critical. Unlike internal combustion engines that depend primarily on mechanical energy transfer, electric vehicles convert, store, and distribute electrical energy throughout their operation—creating multiple applications where silver's 108% electrical conductivity rating (the highest of all elements) provides irreplaceable performance advantages.

Why Electric Vehicles Consume More Silver

Electric vehicles demand significantly more silver than traditional automobiles due to their fundamental architecture and operational requirements. The primary driver is the vehicle's extensive electrical system, which includes high-voltage battery packs, power electronics, charging infrastructure, and advanced driver assistance systems (ADAS).

Battery management systems represent the largest single source of silver consumption in EVs. These sophisticated electronic controllers monitor individual cell voltages, temperatures, and charge states across hundreds of battery cells. Each battery management unit contains numerous printed circuit boards with silver-plated contacts, connectors, and traces to ensure reliable data transmission and power distribution. A typical EV battery pack requires 15-25 grams of silver just for the management electronics.

Power electronics add another significant silver requirement. The inverter, which converts DC battery power to AC motor power, contains silver-plated busbars, connectors, and heat sinks. DC-DC converters that step down high-voltage battery power for auxiliary systems also rely heavily on silver contacts and conductors. The onboard charger, which converts AC grid power to DC battery charging current, incorporates silver-based components throughout its circuitry.

High-voltage wiring harnesses in EVs contain substantially more silver than conventional automotive wiring. These harnesses must safely carry 400-800 volts throughout the vehicle, requiring superior conductivity and reliability. Silver plating on copper conductors prevents corrosion and maintains low contact resistance over the vehicle's lifetime, critical for both performance and safety.

Advanced safety systems standard in most EVs add further silver demand. Radar sensors for collision avoidance, cameras for lane-keeping assistance, and LiDAR systems for autonomous driving capabilities all incorporate silver-based electronic components. These systems require precise signal processing and high-reliability connections where silver's properties prove indispensable.

Silver's Critical Role in EV Components

Silver's unique physical properties make it irreplaceable in several critical EV applications. With an electrical conductivity of 63.0 × 10^6 S/m—6% higher than copper and 60% higher than aluminum—silver enables more efficient power transmission with less energy loss. This efficiency translates directly to improved EV range and performance.

In high-current applications like battery pack connections and motor controllers, silver's superior conductivity reduces resistive heating, improving system reliability and longevity. Battery pack connections carrying 400-600 amperes benefit significantly from silver-plated terminals that maintain low contact resistance over millions of charge-discharge cycles.

Silver's thermal conductivity of 429 W/m·K also proves crucial in EV thermal management. Power electronics generate substantial heat during operation, and silver-based heat sinks and thermal interface materials help dissipate this heat effectively. Proper thermal management extends component life and maintains performance under demanding conditions.

The metal's corrosion resistance ensures reliable long-term operation in automotive environments. EV components must function reliably for 150,000+ miles over 10-15 years, exposed to temperature extremes, humidity, salt spray, and vibration. Silver's chemical stability and resistance to oxidation provide the durability required for automotive applications.

Silver's antimicrobial properties offer additional benefits in EV interiors, particularly relevant as ride-sharing and autonomous vehicles become more common. Silver-based coatings and treatments on touch surfaces help maintain hygiene without requiring harsh chemical cleaners that could damage electronic components.

EV Market Growth Projections and Silver Demand

Global electric vehicle sales have accelerated rapidly, growing from 3.2 million units in 2020 to over 14 million in 2023 according to the International Energy Agency. Industry forecasts project continued exponential growth, with EV sales potentially reaching 30-40 million units annually by 2030.

This growth trajectory translates to substantial silver demand increases. Using conservative estimates of 35 grams silver per EV (midpoint of 25-50g range), 30 million EVs would consume approximately 1,050 metric tons of silver annually. For context, global silver mine production totaled roughly 26,000 metric tons in 2023, meaning EVs could represent 4% of total mine supply by 2030.

Regional growth patterns suggest concentrated demand increases. China, already the world's largest EV market with 60% global market share, plans to reach 40% EV penetration by 2030. European Union mandates require 100% zero-emission vehicle sales by 2035, while several U.S. states have adopted similar timelines. These regulatory frameworks create predictable, policy-driven demand that mining companies must prepare for.

The commercial vehicle electrification adds another demand layer. Electric buses require 200-400 grams of silver each due to their larger battery packs and power systems. Electric delivery trucks, increasingly adopted by logistics companies, consume 150-300 grams per vehicle. As these segments electrify over the next decade, they could add another 500-1,000 metric tons of annual silver demand.

Tesla's latest Cybertruck, for example, incorporates approximately 45-55 grams of silver per vehicle according to materials analysts, reflecting the higher silver content typical of premium EVs with advanced features. As mainstream manufacturers adopt similar technologies, average silver content per vehicle will likely trend toward the higher end of current estimates.

Supply Chain Implications for Silver Markets

The automotive industry's shift toward electrification creates a new category of industrial silver demand with distinct characteristics from traditional electronics applications. Automotive supply chains prioritize reliability, quality, and long-term availability over cost optimization, potentially creating premium demand for silver.

Unlike consumer electronics with 2-3 year replacement cycles, automotive applications require 10-15 year component life. This durability requirement favors silver over cost alternatives like copper or aluminum, despite silver's higher material costs. Automotive manufacturers cannot compromise on reliability for components that must function flawlessly over a vehicle's lifetime.

Just-in-time automotive manufacturing also creates concentrated demand patterns. Vehicle production typically occurs in large facilities producing hundreds of thousands of units annually. A single automotive plant's silver requirements can impact regional silver markets, particularly if multiple manufacturers expand EV production simultaneously in the same geographic region.

The automotive industry's supply chain complexity adds another dynamic to silver markets. Silver demand from automotive applications flows through multiple tiers of suppliers—from raw material refiners to component manufacturers to automotive tier-1 suppliers—before reaching vehicle assembly plants. This extended supply chain can create bullwhip effects where small changes in vehicle demand translate to larger swings in silver procurement.

Automotive manufacturers' increasing focus on supply chain resilience following recent semiconductor shortages has led to longer-term procurement contracts and strategic inventory building. This trend could smooth silver demand patterns but also create periods of accelerated procurement as companies build buffer stocks.

Battery Technology Evolution and Silver Content

Lithium-ion battery technology continues evolving rapidly, with implications for silver content in future EVs. Current battery chemistries like lithium iron phosphate (LFP) and nickel-cobalt-aluminum (NCA) require extensive battery management systems that rely heavily on silver-based components.

Next-generation battery technologies may alter silver consumption patterns. Solid-state batteries, currently in development by multiple manufacturers, promise higher energy density and improved safety but may require different electronic architectures. Early prototypes suggest solid-state batteries need more sophisticated monitoring systems, potentially increasing silver content per kWh of battery capacity.

Silicon nanowire anodes, another promising technology, could increase battery capacity while requiring more complex thermal management. Silver's thermal conductivity advantages become more important as battery power density increases, potentially driving higher silver consumption per vehicle.

Battery recycling presents both opportunities and challenges for silver markets. As first-generation EVs reach end-of-life in the 2030s, recycling facilities will recover silver from battery management systems and power electronics. However, silver recovery rates from complex electronic assemblies typically achieve only 60-80% efficiency, meaning recycling cannot fully offset primary demand growth.

The push toward faster charging capabilities also increases silver demand. High-power DC fast charging requires robust power electronics capable of handling 150-350kW power levels safely. These systems incorporate larger amounts of silver for heat dissipation and electrical connections, adding 5-10 grams per vehicle compared to standard charging systems.

Competitive Materials and Silver Substitution

Despite silver's superior properties, cost pressures drive ongoing research into alternative materials for automotive applications. Copper remains the primary substitute due to its lower cost and adequate conductivity for many applications. However, copper's 6% lower conductivity and higher susceptibility to corrosion limit its effectiveness in critical EV systems.

Graphene-enhanced conductors represent an emerging alternative, potentially offering silver-like conductivity at lower costs. However, graphene production remains expensive and technically challenging, limiting near-term commercial viability. Most graphene applications focus on specialty electronic components rather than bulk automotive wiring.

Aluminum substitution works for some applications but requires larger conductor cross-sections due to its lower conductivity. This size increase often negates cost savings and creates packaging challenges in space-constrained EV designs. Aluminum also suffers from galvanic corrosion when connected to other metals, reducing system reliability.

Silver-plated copper provides a compromise solution, offering most of silver's benefits at reduced material costs. This approach uses silver only where its properties prove critical—typically contact surfaces and high-current connections—while using copper for bulk conductors. However, silver plating still represents substantial silver consumption, typically 2-5 grams per vehicle depending on plating thickness and coverage area.

The automotive industry's conservative approach to material substitution limits rapid changes. Vehicle manufacturers require extensive testing and validation before adopting new materials, often taking 3-5 years from initial evaluation to production implementation. This validation timeline provides stability for silver demand even as alternative materials develop.

Regional EV Adoption Patterns Affecting Silver Demand

Electric vehicle adoption varies significantly by region, creating geographic concentrations of silver demand. China leads global EV production and sales, with cities like Shenzhen achieving nearly 100% electric bus fleets. Chinese EV manufacturers like BYD and CATL have become major silver consumers as their production scales reach millions of vehicles annually.

European EV adoption accelerates rapidly due to aggressive government policies and consumer incentives. Norway achieved 80% EV market share in new vehicle sales, while Netherlands and Germany show strong growth trends. European EV manufacturers tend to use higher silver content per vehicle due to premium positioning and advanced feature sets.

United States EV adoption remains concentrated in certain states, with California representing 40% of national EV sales. Tesla's dominance in the U.S. market creates concentrated silver demand, as Tesla vehicles typically contain above-average silver content due to their advanced electrical systems and over-the-air update capabilities requiring robust electronic architectures.

Emerging markets present the next wave of EV adoption, with India, Brazil, and Southeast Asian countries developing EV incentive programs. However, these markets typically favor lower-cost EVs with reduced silver content compared to premium markets. As these regions develop, silver content per vehicle may increase due to safety regulations and consumer preferences for advanced features.

Manufacturing Process Silver Requirements

EV production itself requires silver beyond what ends up in finished vehicles. Manufacturing equipment for battery production, electric motor assembly, and power electronics fabrication incorporates silver-based components for precision and reliability.

Battery cell manufacturing requires specialized equipment with silver-plated contacts and conductors for handling high currents during formation and testing. Cell formation equipment alone can consume 10-20 kilograms of silver per production line capable of producing batteries for 100,000 vehicles annually.

Electric motor manufacturing uses silver-brazing alloys for joining rotor and stator components. High-performance EV motors require precise metallurgical joints that maintain electrical and mechanical integrity under extreme operating conditions. Silver brazing provides superior joint strength and conductivity compared to alternative materials.

Quality control and testing equipment throughout EV production incorporates silver-based components. High-voltage testing equipment, electromagnetic compatibility (EMC) chambers, and precision measurement devices all rely on silver's electrical properties for accurate results.

The semiconductor fabrication equipment used to produce EV power electronics also represents significant silver consumption. Advanced power semiconductors like silicon carbide (SiC) and gallium nitride (GaN) require specialized processing equipment with silver-based components for high-temperature and high-power handling capabilities.

Infrastructure Development and Silver Demand

EV charging infrastructure development creates additional silver demand beyond the vehicles themselves. Level 2 and DC fast charging stations incorporate substantial amounts of silver in their power electronics and electrical connections.

A typical DC fast charging station contains 500-1,500 grams of silver depending on power rating and number of charging ports. With plans for millions of charging stations globally, infrastructure development could add 500-1,000 metric tons of annual silver demand by 2030.

Smart grid integration required for widespread EV adoption also drives silver consumption. Advanced metering infrastructure, grid-scale energy storage, and demand response systems all incorporate silver-based electronic components. The expanding electrical grid infrastructure needed to support EV charging represents a secondary but significant source of silver demand.

Vehicle-to-grid (V2G) technology, which allows EVs to supply power back to the electrical grid, requires additional power electronics and communication systems. V2G-capable vehicles typically contain 10-15 grams more silver than standard EVs due to bidirectional charging capabilities and grid communication requirements.

Wireless charging systems under development by several manufacturers could substantially increase silver consumption per vehicle. Wireless charging requires high-frequency power electronics and precisely tuned resonant circuits where silver's low resistance proves critical for efficiency. Early prototype systems suggest wireless charging capability could add 20-30 grams of silver per vehicle.

Market Impact Analysis

Current silver prices at $77.27/oz (as of February 13, 2026) reflect broader precious metals market dynamics but may not fully account for emerging industrial demand from EV adoption. Silver's industrial applications already consume approximately 60% of annual mine production, with automotive applications representing a small but rapidly growing segment.

The automotive industry's price-insensitive demand characteristics could provide support for silver prices during economic downturns when investment demand typically weakens. Unlike speculative investment flows, automotive silver demand derives from production schedules and regulatory requirements that persist regardless of economic conditions.

Supply constraints present the most significant market risk. Global silver mine production has declined in recent years due to ore grade deterioration and limited new mine development. Adding 1,000+ metric tons of annual automotive demand to an already tight supply market could create significant price pressures.

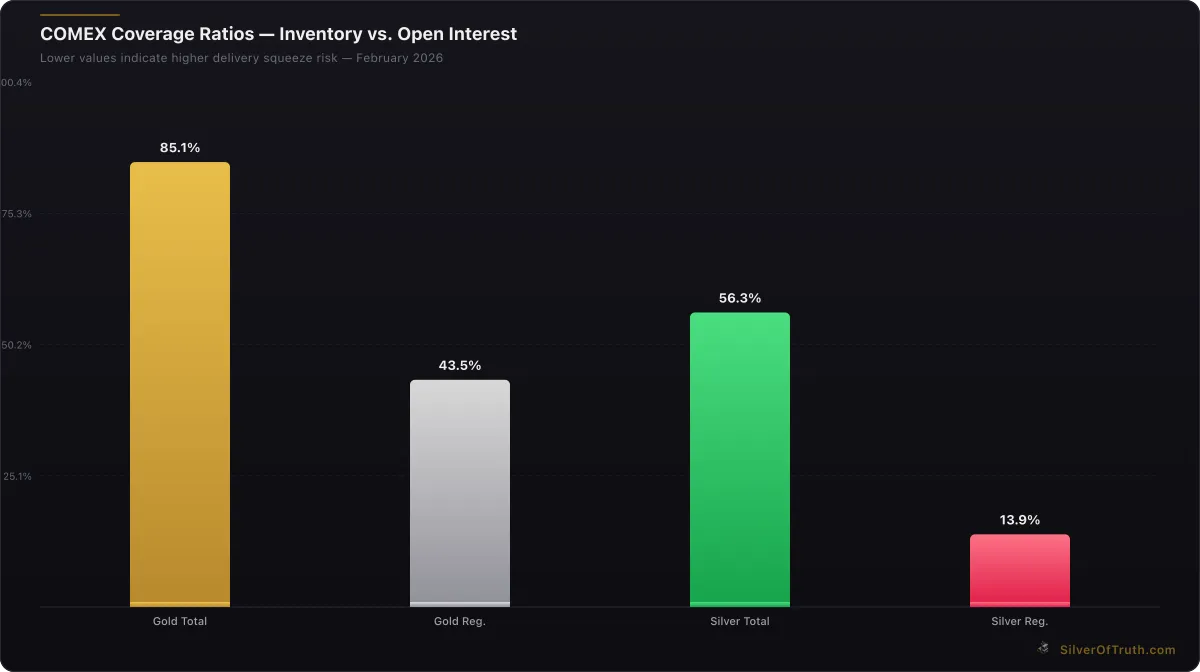

COMEX silver inventory currently shows concerning trends, with registered silver at 92.9 million ounces and coverage ratios at high-risk levels according to SilverOfTruth data. Industrial demand growth from EVs and other applications could exacerbate existing supply tightness in physical silver markets.

Investment implications extend beyond silver prices to mining company valuations and automotive supply chain costs. Silver miners with low-cost production profiles may benefit disproportionately from sustained industrial demand growth. Conversely, automotive manufacturers may face increased materials costs that could impact EV pricing strategies.

Frequently Asked Questions

How much silver does a typical electric vehicle contain? Modern electric vehicles contain 25-50 grams of silver on average, compared to 15-28 grams in conventional gasoline vehicles. Premium EVs with advanced features and larger battery packs often contain 45-60 grams of silver.

Can silver be substituted with other materials in EVs? While copper and aluminum can substitute silver in some applications, silver's superior electrical conductivity, corrosion resistance, and thermal properties make it irreplaceable in critical EV systems like battery management, power electronics, and high-current connections.

Will silver recycling from end-of-life EVs offset demand growth? Silver recycling from EVs will provide some supply relief starting in the 2030s, but recovery rates of 60-80% from complex electronic assemblies mean recycling cannot fully offset growing primary demand from expanding EV production.

How does EV charging infrastructure affect silver demand? EV charging stations require 500-1,500 grams of silver each for power electronics and electrical connections. Global charging infrastructure development could add 500-1,000 metric tons of annual silver demand by 2030.

Which EV manufacturers use the most silver per vehicle? Premium manufacturers like Tesla, Mercedes EQS, and BMW iX typically incorporate above-average silver content due to advanced electrical systems, autonomous driving capabilities, and high-performance power electronics.

Investment Implications and Market Outlook

The convergence of accelerating EV adoption with constrained silver supply creates a compelling long-term investment thesis for silver markets. Unlike cyclical consumer electronics demand, automotive applications provide sustained, growing demand with limited substitution possibilities.

Source: SilverOfTruth COMEX data, February 2026

COMEX coverage ratios — lower values indicate higher delivery squeeze risk. Source: SilverOfTruth, February 2026

Investors can monitor EV silver demand through multiple data sources available in the SilverOfTruth app, including industrial demand trends, COMEX inventory levels, and global EV production statistics. Understanding these interconnected factors provides insight into one of silver's most significant emerging demand drivers.

The transformation of global transportation toward electrification represents a generational shift that will unfold over the next two decades. As EV technology advances and production scales, silver's role becomes increasingly critical—positioning the metal as an essential component of the clean energy transition. Track real-time silver market developments and EV demand indicators with comprehensive data analysis in the SilverOfTruth app, available on the App Store.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, investment, or trading advice. Past performance is not indicative of future results. Always conduct your own research and consult with a qualified financial advisor before making investment decisions. SilverOfTruth provides market data and analysis tools — it does not provide personalized financial advice.