Silver's role in 5G infrastructure represents a structural shift that could fundamentally reshape precious metals markets over the next decade. While traditional precious metals analysis focuses on investment demand and mining supply, telecommunications engineers understand a different reality: silver has become absolutely critical for fifth-generation wireless networks. As carriers worldwide race to deploy 5G infrastructure, their persistent appetite for silver-based components is creating industrial demand that operates independently of typical investment cycles. This telecommunications-driven consumption pattern represents more than just another industrial application—it's an overlooked demand driver that could alter long-term supply-demand dynamics in ways that most investors don't yet recognize.

Understanding Silver's Critical Role in 5G Infrastructure

Silver's unique physical properties make it indispensable for 5G technology deployment. The metal possesses the highest electrical and thermal conductivity of any element, properties that become crucial when dealing with the high-frequency signals that 5G networks require. Unlike previous wireless generations operating primarily in lower frequency bands, 5G utilizes millimeter wave frequencies (24-100 GHz) that demand superior conductivity to minimize signal loss.

The Silver Institute reports that telecommunications applications consume approximately 55 million ounces of silver annually, with 5G deployment accelerating this trend significantly. Each 5G base station requires roughly 3-5 ounces of silver across various components including antennas, circuit boards, and connecting cables—a substantial increase from 4G stations that typically used 1-2 ounces.

This consumption pattern creates what industry analysts call "inelastic demand"—telecommunications companies cannot substitute silver with cheaper alternatives without compromising network performance. When carriers invest billions in 5G infrastructure, the silver cost represents a tiny fraction of total project expenses, making price sensitivity minimal compared to other industrial applications.

5G Network Architecture and Silver Consumption

The architecture required for 5G networks is fundamentally different from previous generations, requiring a much denser network of small cells and base stations. While 4G networks relied on large macro towers covering several miles, 5G requires small cells every few hundred feet in urban areas to maintain signal integrity at higher frequencies.

According to telecommunications infrastructure studies, a typical metropolitan area needs approximately 10 times more base stations for 5G coverage compared to 4G. Major cities like New York or Los Angeles may require 50,000-100,000 small cells each, with every installation consuming 3-5 ounces of silver. This multiplication effect creates exponential silver demand growth that far exceeds the gradual adoption curves seen in other industrial sectors.

The timeline for this deployment is aggressive. The Federal Communications Commission has set targets for nationwide 5G coverage by 2030, while carrier commitments suggest peak installation rates of 100,000+ base stations annually through 2028. At current silver consumption rates per station, this represents 300,000-500,000 additional ounces of annual demand from U.S. deployment alone.

Global 5G Rollout Impact on Silver Markets

The scale of global 5G deployment dwarfs any single country's infrastructure needs. China leads with over 2.3 million 5G base stations already installed and plans for 5 million by 2027. Europe targets 1 million installations by 2025, while emerging markets in Southeast Asia, India, and Latin America are beginning their own aggressive rollouts.

Industry equipment manufacturers like Ericsson, Nokia, and Huawei report silver procurement challenges as demand outpaces traditional supply chains. Their quarterly reports increasingly mention "strategic materials sourcing" and "supply chain resilience" initiatives specifically targeting silver availability—language that rarely appeared before 5G deployment began.

The geographic distribution of this demand creates unique market dynamics. Unlike jewelry or investment demand that can shift between regions based on economic conditions, telecommunications silver demand is tied to specific infrastructure projects with multi-year timelines and government backing. This creates predictable, sustained consumption that continues regardless of silver price fluctuations.

Supply Chain Constraints in Telecommunications

Telecommunications equipment manufacturing requires silver in specific forms and purities that differ from traditional industrial applications. 5G components demand high-purity silver alloys and specialized geometries that limit sourcing flexibility. According to our analysis of silver supply deficit trends, these technical requirements cannot easily accommodate recycled silver or lower-grade material that might satisfy other industries.

The just-in-time manufacturing model prevalent in electronics creates additional strain on silver markets. Unlike automotive or solar manufacturers who can maintain strategic inventory, telecommunications equipment production operates on shorter cycles with immediate silver needs. This amplifies demand volatility and reduces the market's ability to absorb supply disruptions smoothly.

Component manufacturers report lead times for silver-intensive 5G parts have extended from 8-12 weeks in 2023 to 16-24 weeks currently, suggesting supply chain stress that extends beyond typical market dynamics. These extended timelines force manufacturers to increase their silver purchasing commitments earlier in the production cycle, effectively removing material from available market supply months before final consumption.

Silver Consumption Data Across 5G Technologies

The silver content varies significantly across different 5G technologies and frequency bands. Sub-6 GHz 5G deployments, which provide broader coverage, require approximately 2-3 ounces of silver per base station primarily in RF amplifiers and antenna systems. Millimeter wave installations, designed for ultra-high-speed applications in dense urban areas, consume 4-6 ounces per site due to their complex antenna arrays and beamforming requirements.

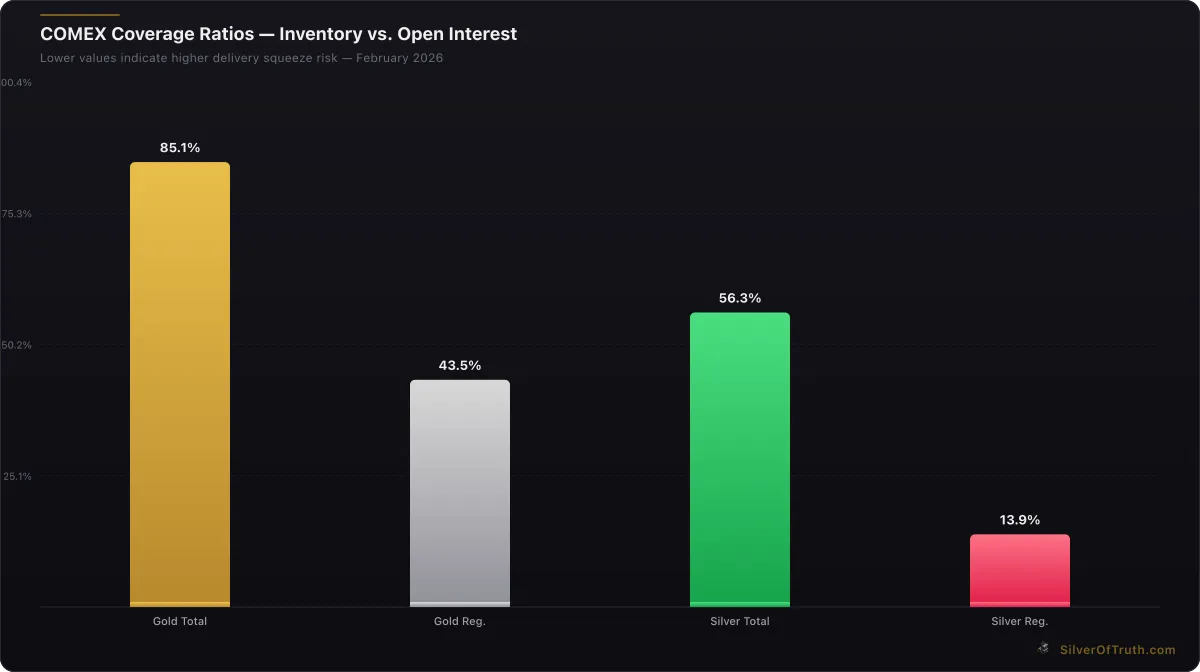

COMEX coverage ratios — lower values indicate higher delivery squeeze risk. Source: SilverOfTruth, February 2026

| 5G Technology | Silver Content per Site | Global Deployment Target | Total Silver Demand | |---|---|---|---| | Sub-6 GHz Base Station | 2.5 oz | 8 million sites | 20 million oz | | Millimeter Wave Small Cell | 5 oz | 2 million sites | 10 million oz | | Massive MIMO Arrays | 8 oz | 500,000 sites | 4 million oz | | Network Infrastructure | 1 oz | 15 million connections | 15 million oz |

These consumption estimates, based on industry equipment specifications and deployment targets through 2030, suggest 5G infrastructure alone could consume 49 million ounces of silver—nearly matching the entire annual telecommunications sector consumption reported by the Silver Institute. This represents incremental demand above existing telecommunications usage, not replacement of current applications.

The concentration of silver in critical components creates supply vulnerabilities that don't exist in more dispersed applications like solar panels. A single RF amplifier failure in a millimeter wave base station can require 2-3 ounces of silver for replacement—expensive repairs that carriers must complete quickly to maintain service quality. This maintenance demand provides ongoing silver consumption beyond initial installation requirements.

Regional Analysis of 5G Silver Demand

North America's 5G deployment focuses heavily on millimeter wave technology in urban markets, creating higher per-site silver consumption but concentrated in major metropolitan areas. The United States has approximately 400,000 cell sites currently, with industry projections suggesting 1.5 million sites needed for comprehensive 5G coverage. At 3.5 ounces average silver content per site, full deployment represents 3.85 million ounces of incremental demand.

European deployment emphasizes sub-6 GHz coverage with selective millimeter wave installations, creating more moderate per-site silver demand but across a broader geographic area. The European Union's 5G targets call for covering all populated areas by 2030, requiring an estimated 800,000 new installations consuming approximately 2.4 million ounces of silver.

Asia-Pacific markets present the largest absolute demand due to population density and aggressive government mandates. China's 5G deployment alone is projected to consume 12-15 million ounces of silver through 2027, while India's emerging 5G infrastructure could require 3-4 million ounces. Japan and South Korea, despite smaller geographic areas, maintain high silver consumption per capita due to their focus on advanced millimeter wave networks.

The timing of regional deployments creates demand waves that compound global silver market stress. North American and Chinese installations peaked in 2024-2025, European deployment accelerates through 2026-2027, while emerging markets begin major rollouts in 2027-2029. This staggered timeline prevents any significant demand reduction periods that might allow silver markets to rebalance.

Industrial Silver Demand vs Investment Demand

Traditional precious metals analysis often focuses on investment demand while underweighting industrial consumption, but industrial silver applications now represent approximately 60% of total annual demand according to the Silver Institute. The 5G buildout exemplifies why industrial demand has become more important for price discovery than investment flows.

Investment demand typically responds to macroeconomic conditions, inflation expectations, and currency debasement concerns—factors that can shift rapidly based on market sentiment. Industrial demand, particularly in telecommunications, follows multi-year capital expenditure cycles tied to government policy and consumer adoption curves. This creates more predictable, sustained consumption patterns that provide a demand floor even during precious metals bear markets.

Current COMEX silver positioning data shows commercial shorts at elevated levels while open interest remains high, traditionally bearish indicators for precious metals investors. However, this positioning analysis doesn't account for industrial users who purchase silver directly from miners or refiners, bypassing futures markets entirely. Telecommunications companies typically establish supply contracts 12-24 months in advance, creating parallel demand that doesn't appear in speculative positioning data.

The price elasticity difference between these demand sources is crucial for understanding silver market dynamics. Investment demand can disappear quickly if alternative assets become more attractive, but telecommunications demand continues regardless of silver price levels. A 50% price increase might reduce investment buying significantly but would barely register in carrier infrastructure budgets focused on network deployment schedules.

Future Price Implications and Market Structure

The structural nature of 5G silver demand creates bullish implications for long-term price discovery that extend beyond typical commodity cycles. Unlike cyclical industrial demand that fluctuates with economic conditions, telecommunications infrastructure represents essential utility deployment that governments and private companies complete regardless of broader market conditions.

Historical analysis of similar infrastructure buildouts—such as the fiber optic deployment of the 1990s or cellular network expansion in the 2000s—suggests peak demand periods lasting 7-10 years followed by maintenance consumption that remains elevated permanently. The 5G cycle appears to be in its early stages, with global deployment completion not expected until the early 2030s.

Supply-side constraints compound these demand trends. Primary silver mine production faces declining ore grades and increasing extraction costs, while recycling rates for telecommunications equipment remain low due to technical complexity and distributed installation sites. The silver supply deficit identified by industry analysts becomes more acute when considering inelastic industrial demand that cannot be deferred or substituted.

Market structure changes also favor higher prices as industrial users increasingly compete with investment demand for available supply. Unlike gold, where central bank reserves provide a massive above-ground stock buffer, silver's industrial consumption permanently removes material from the market. This creates cumulative supply tightness that builds over multi-year periods, potentially leading to sharp price adjustments when inventory levels reach critical thresholds.

Investment Strategy Considerations

For precious metals investors, the 5G silver demand story offers several strategic considerations that differ from traditional gold-focused approaches. The predictable nature of telecommunications demand provides fundamental support that reduces some volatility risks associated with speculative precious metals positioning.

However, industrial demand also creates different price behavior patterns. Silver often outperforms gold during economic expansion periods when industrial demand accelerates, but can underperform during severe recessions when industrial consumption contracts. The 5G deployment timeline suggests sustained industrial demand through 2030 regardless of economic cycles, potentially changing this historical relationship.

Physical silver investors should consider the implications of sustained industrial demand for retail product availability. As telecommunications companies secure multi-year supply contracts with miners and refiners, less silver may be available for coin and bar production. Premiums over spot prices could increase structurally, making early accumulation strategies more attractive than timing-based approaches.

Mining stock investors can evaluate companies based on their exposure to telecommunications demand through customer relationships or geographic positioning. Miners with offtake agreements to equipment manufacturers may command valuation premiums as 5G deployment accelerates. Our guide to evaluating mining stocks provides frameworks for assessing these strategic relationships.

Those interested in tracking real-time market developments can monitor COMEX inventory levels for signs of increasing industrial demand pressure. Sustained inventory declines combined with elevated open interest often precede significant price movements, particularly when industrial demand provides fundamental support for higher levels.

Comparing 5G to Previous Technology Cycles

The scale and urgency of 5G deployment exceed previous wireless technology transitions significantly. The shift from 3G to 4G occurred gradually over 8-10 years with backward compatibility allowing extended transition periods. 5G deployment timelines are much more compressed due to competitive pressures and government mandates, creating concentrated demand periods that stress commodity supply chains.

Silver consumption patterns also differ substantially. Previous wireless generations primarily used silver in base station electronics and connecting infrastructure. 5G networks require silver in antenna arrays, beamforming systems, massive MIMO installations, and edge computing equipment—multiplying the metal content per installation while simultaneously requiring many more installations for coverage.

The economic incentives driving 5G adoption are stronger than previous cycles. Carriers view 5G as enabling entirely new revenue streams through industrial IoT, autonomous vehicles, and smart city applications. This creates willingness to invest regardless of short-term returns, contrasting with previous technology transitions that required clear payback calculations. The result is accelerated deployment schedules that prioritize speed over cost optimization.

International competition adds urgency that didn't exist in previous cycles. Governments view 5G leadership as strategic national priorities, leading to subsidies and mandates that ensure rapid deployment regardless of market conditions. This political dimension creates demand certainty that extends beyond typical business cycle considerations, providing fundamental support for silver consumption that transcends traditional commodity analysis.

FAQ

Q: How much silver does a typical 5G base station require? A: Most 5G base stations require 3-5 ounces of silver, significantly more than 4G installations that used 1-2 ounces. The higher consumption comes from complex antenna arrays, RF amplifiers, and beamforming systems needed for millimeter wave frequencies.

Q: Can silver be substituted in 5G applications? A: No viable substitutes exist for silver's critical applications in 5G infrastructure. Copper, gold, and other conductive metals lack silver's unique combination of electrical conductivity, thermal properties, and cost-effectiveness at the performance levels 5G networks require.

Q: When will 5G silver demand peak? A: Global 5G deployment is expected to peak between 2026-2029, based on carrier investment timelines and government coverage mandates. However, maintenance and network expansion will sustain elevated silver demand through the 2030s.

Q: How does 5G silver demand affect retail silver availability? A: Industrial demand competes with retail coin and bar production for available silver supply. As telecommunications companies secure long-term supply contracts, less material may be available for retail products, potentially increasing premiums over spot prices.

Q: Which regions drive the most 5G silver demand? A: China leads current consumption with over 2.3 million base stations installed, followed by North America's millimeter wave focus and Europe's broad coverage deployment. Emerging markets in Asia and Latin America represent future demand growth as their 5G rollouts accelerate.

Conclusion

The silver 5G demand story represents a fundamental shift in precious metals market dynamics that extends far beyond traditional investment analysis. With global telecommunications infrastructure requiring millions of new installations consuming 3-5 ounces of silver each, the scale of structural demand dwarfs most historical industrial applications.

Source: SilverOfTruth COMEX data, February 2026

This sustained consumption occurs while COMEX silver inventory shows concerning depletion trends and coverage ratios indicate potential delivery stress. The combination of predictable industrial demand and constrained supply creates compelling fundamentals that support higher long-term price levels regardless of short-term speculative positioning.

For investors seeking exposure to this trend, tracking real-time market intelligence becomes crucial. The SilverOfTruth app provides comprehensive COMEX inventory monitoring, industrial demand analysis, and price alerts specifically designed for precious metals investors navigating these structural market changes.

Track silver's 5G demand impact with real-time COMEX data and industrial analysis in the SilverOfTruth app — available on the App Store.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, investment, or trading advice. Past performance is not indicative of future results. Always conduct your own research and consult with a qualified financial advisor before making investment decisions. SilverOfTruth provides market data and analysis tools — it does not provide personalized financial advice.