Global silver mine supply faces its most challenging period in decades, with production declining across major mining regions while industrial demand continues its relentless climb. This fundamental shift in supply dynamics has created what many analysts consider a structural deficit that could reshape precious metals markets for years to come.

The numbers paint a stark picture: primary silver mine production has fallen approximately 12% from peak levels reached in 2015-2016, while recycling rates struggle to offset the shortfall. Meanwhile, industrial applications now consume over 50% of annual silver supply, creating unprecedented competition between investors and manufacturers for available metal. Understanding these supply constraints is crucial for anyone evaluating silver's long-term prospects.

Global Silver Mine Production Trends

Silver mine production reached historic highs of approximately 886 million ounces in 2016, according to data from the Silver Institute. However, this peak marked the beginning of a concerning downward trend that continues today. By 2023, global mine production had declined to roughly 780 million ounces—a reduction of over 100 million ounces annually.

Source: SilverOfTruth COMEX data, February 2026

This decline stems from multiple interconnected factors affecting mines worldwide. Ore grades have deteriorated significantly as miners exhaust high-grade deposits discovered decades ago. The average silver ore grade has fallen from approximately 12-15 ounces per ton in the 1980s to just 6-8 ounces per ton today at many operations. This means miners must process twice as much rock to extract the same amount of silver, dramatically increasing costs and environmental impact.

Mexico, the world's largest silver producer, exemplifies these challenges. Mexican silver production peaked at 196 million ounces in 2016 but has since declined to approximately 175 million ounces annually. Major Mexican mines like Fresnillo's Saucito and Ciénega operations have reported declining ore grades and increased production costs, forcing some mines to reduce output or enter care-and-maintenance status.

Peru, the second-largest producer, faces similar headwinds. The country's silver output has fallen from peak levels of 140 million ounces to approximately 115 million ounces currently. Environmental regulations, community opposition to mining, and aging infrastructure have compounded the natural decline in ore quality. Political instability in Peru has further deterred investment in new mining projects, limiting the potential for production growth.

Cost Inflation and Economic Pressures

Silver mining costs have skyrocketed over the past decade, creating economic pressure that forces mine closures even when silver prices remain elevated. All-in sustaining costs (AISC) for primary silver miners now average $15-20 per ounce, compared to $8-12 per ounce a decade ago. This cost inflation results from multiple factors including higher energy prices, increased labor costs, stricter environmental regulations, and the need to process lower-grade ore.

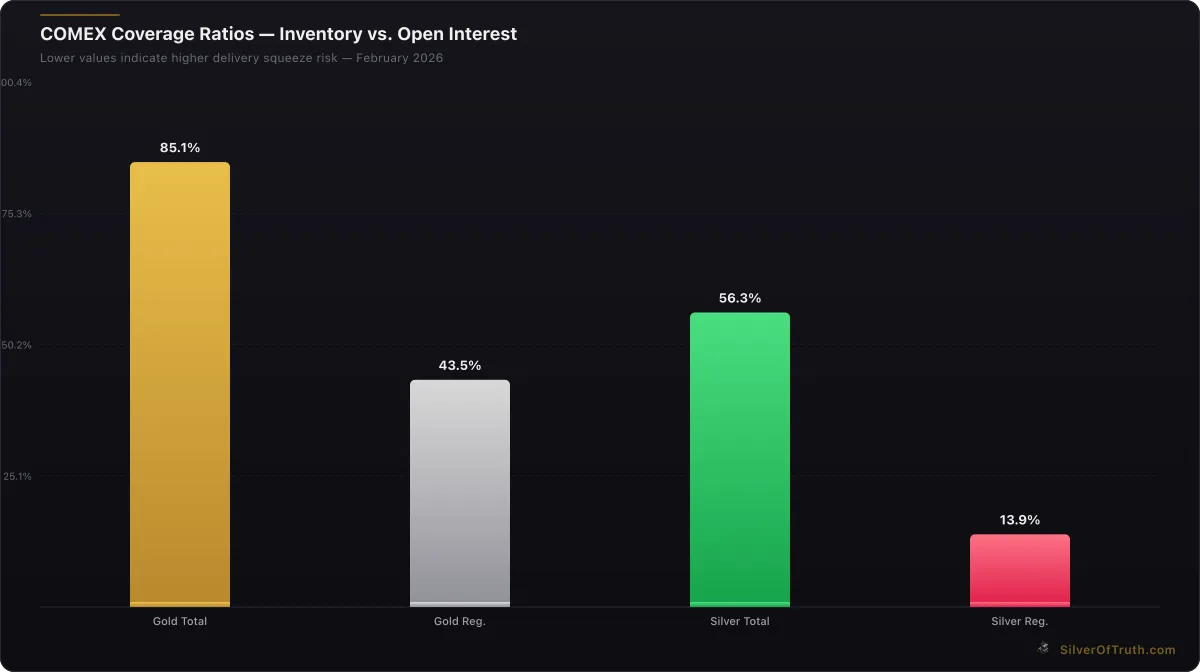

COMEX coverage ratios — lower values indicate higher delivery squeeze risk. Source: SilverOfTruth, February 2026

Energy represents the largest component of mining costs, often accounting for 20-30% of total expenses. As mines dig deeper and process more ore to maintain output, electricity consumption rises exponentially. The shift toward renewable energy, while environmentally beneficial, has added complexity and upfront capital requirements that strain mining budgets.

Labor costs have also surged as skilled miners become increasingly scarce. Remote mining locations struggle to attract workers, forcing companies to offer premium wages and benefits. Additionally, enhanced safety requirements and training programs, while necessary, add operational complexity and expense. These factors combine to create a challenging environment where marginal mines become uneconomical at current silver prices.

Our guide to evaluating mining stocks provides detailed analysis of how investors can assess whether mining companies can maintain profitability amid rising costs. The metrics show that only the most efficient operations with highest-grade deposits remain economically viable in today's environment.

Depletion of High-Grade Deposits

The silver mining industry faces a fundamental challenge: the world's richest, most accessible silver deposits have largely been exhausted. Historical mining focused on high-grade veins and surface deposits that could be extracted relatively cheaply. Today's miners increasingly rely on lower-grade deposits that require advanced extraction technologies and massive capital investment.

Major silver districts worldwide show clear signs of depletion. The legendary Comstock Lode in Nevada, which produced over 8 million ounces annually at its peak, now yields minimal amounts. Similarly, the famous Potosí region in Bolivia, once the world's largest silver producer, operates at a fraction of historical output levels. Even modern mining districts face depletion pressures as companies exhaust the highest-grade zones within their concessions.

The geological reality is that silver deposits follow natural distribution patterns, with a small percentage of deposits containing the majority of economically recoverable metal. The Pareto Principle applies to mineral deposits: roughly 20% of deposits contain 80% of high-grade ore. As miners exhaust these prime deposits, they face the choice of processing lower-grade material at higher costs or abandoning operations entirely.

This depletion cycle explains why new silver discoveries rarely replace production from exhausted mines. Even when exploration teams locate new deposits, the ore grades typically fall well below historical averages. Modern silver mines average 6-10 ounces per ton compared to 15-20 ounces per ton at historic operations. This fundamental shift requires entirely different mining approaches and economic models.

For investors seeking exposure to silver supply fundamentals, understanding these depletion patterns is crucial. Our analysis of COMEX inventory trends shows how mine supply constraints translate into warehouse drawdowns and potential delivery pressures in futures markets.

Regional Mining Analysis

Mexico: The Dominant Producer Under Pressure

Mexico produces approximately 23% of global silver mine supply, making it the world's undisputed leader. However, Mexican production faces multiple headwinds that threaten its dominance. The country's major silver-producing states—Zacatecas, Chihuahua, and Durango—all report declining output from aging mines.

Fresnillo plc, Mexico's largest silver producer, exemplifies industry-wide challenges. The company's flagship Fresnillo mine has operated since 1554 but now faces declining ore grades and complex geology that increases extraction costs. Fresnillo's annual reports show silver ore grades falling from 380 grams per tonne in 2005 to approximately 280 grams per tonne currently—a 26% decline that requires processing significantly more rock for the same silver output.

Environmental and social challenges compound Mexico's production difficulties. New mining projects face lengthy permitting processes and community opposition, while existing operations must invest heavily in environmental remediation and social programs. These factors increase costs and delay expansion projects, limiting Mexico's ability to offset declining production from mature mines.

Peru: Political Risk and Infrastructure Challenges

Peru's silver mining industry, while still significant, faces unique challenges that limit growth potential. Political instability has deterred foreign investment in new mining projects, while aging infrastructure constrains existing operations. The country's remote mining locations require significant infrastructure investment for power, transportation, and communications—costs that become prohibitive as ore grades decline.

Recent political tensions have created uncertainty around mining taxation and environmental regulations. Some international mining companies have reduced their Peruvian operations or delayed expansion projects due to regulatory uncertainty. This political risk premium makes it difficult to justify the large capital investments required for modern silver mining operations.

Other Producing Regions

China, while not traditionally considered a major silver producer, has become increasingly important through its massive lead-zinc mining operations that produce silver as a byproduct. However, Chinese silver production data remains opaque, making it difficult to assess long-term trends. What is clear is that Chinese domestic silver demand has grown dramatically, reducing the amount available for export.

Australia and Canada, traditional mining powerhouses, have seen silver production stagnate as miners focus on more profitable commodities like gold and copper. Many silver deposits in these countries remain uneconomical at current price levels and cost structures, leaving significant resources undeveloped.

Exploration and New Discovery Challenges

The pipeline of new silver discoveries has virtually dried up, creating long-term supply concerns that extend well beyond current production declines. Major mining companies have reduced exploration budgets for silver-focused projects, preferring to invest in larger-scale gold and copper operations that offer better returns on capital.

Exploration success rates have declined significantly over the past two decades. The likelihood of a major new silver discovery has fallen from roughly 1 in 1,000 targets in the 1990s to approximately 1 in 3,000 today. This decline reflects the reality that the most obvious and accessible deposits have already been found, leaving exploration teams to investigate increasingly remote and challenging locations.

Modern silver exploration requires sophisticated geological techniques and substantial capital investment. Deep drilling programs can cost millions of dollars with no guarantee of success. Many junior mining companies lack the financial resources for comprehensive exploration programs, while major miners prefer to acquire proven deposits rather than invest in grassroots exploration.

The time horizon from discovery to production has also lengthened dramatically. Environmental assessments, community consultation, and permitting processes now typically require 7-10 years even for straightforward projects. Complex deposits or those in sensitive locations may require 15-20 years from discovery to first production. This extended timeline means that even significant new discoveries made today won't impact supply for at least a decade.

For investors tracking silver supply dynamics, our silver supply deficit analysis provides detailed examination of how exploration challenges contribute to long-term structural deficits in silver markets.

Byproduct vs. Primary Production Dynamics

Understanding silver's production profile reveals a critical vulnerability in global supply chains. Approximately 70% of silver mine production comes as a byproduct of lead-zinc, copper, and gold mining operations. Only 30% comes from primary silver mines where silver is the main economic driver. This byproduct dependency creates unique supply risks that don't exist for most other commodities.

When primary metals like lead, zinc, or copper face price declines, mining companies may reduce production or close operations entirely, cutting silver output as an unintended consequence. The silver market has limited ability to respond to these supply disruptions through price signals, since silver revenue represents only 10-20% of total revenue at byproduct operations.

Recent copper price volatility illustrates this dynamic. When copper prices declined in 2023, several major copper mines reduced output or entered maintenance mode, cutting silver production by an estimated 15-20 million ounces annually. Silver prices would need to rise dramatically to incentivize these operations to maintain output solely for silver revenue.

Primary silver miners face their own challenges. These operations typically require silver prices above $25-30 per ounce to justify expansion or new development. With silver currently trading around $77.27, economic conditions appear favorable. However, the lead time for new mine development means supply responses lag price signals by many years.

The byproduct dependency also means silver supply correlates with industrial metals demand rather than precious metals fundamentals. During economic downturns when silver investment demand typically rises, byproduct silver supply often falls as industrial metals operations reduce output. This creates a natural supply-demand imbalance that can amplify price volatility.

Environmental and Regulatory Impact

Environmental regulations have become a major constraint on silver mine development and operation worldwide. Modern mining operations must meet increasingly stringent environmental standards that add significant costs and complexity to silver extraction. These regulations, while necessary for environmental protection, create barriers to new mine development and increase operating costs at existing operations.

Water usage regulations particularly impact silver mining operations. Many silver deposits are located in arid regions where water resources are scarce and heavily regulated. Modern extraction techniques require substantial water for ore processing, dust suppression, and waste management. Obtaining water permits can take years and may limit production capacity even at approved operations.

Tailings management has become another critical environmental challenge. Silver mines generate substantial waste rock and tailings that must be stored and monitored indefinitely. Recent tailings dam failures at other mining operations have triggered stricter oversight and higher financial requirements for waste storage. These requirements increase capital costs and may make marginal silver deposits uneconomical.

Carbon emissions regulations add another layer of complexity. Mining operations consume substantial energy for ore processing, transportation, and equipment operation. As governments implement carbon taxes and emissions limits, mining costs increase significantly. Some operations have invested in renewable energy systems, but these require substantial upfront capital investment that strains project economics.

Social license to operate has become equally important as formal environmental permits. Mining companies must now engage extensively with local communities and address social concerns that extend far beyond environmental impact. These consultation processes can delay projects for years and require ongoing social investment that increases operating costs.

Technology and Mining Innovation

Technological innovation offers some hope for addressing silver mine supply challenges, though current solutions remain limited in scope and effectiveness. Advanced extraction techniques can marginally improve recovery rates from existing operations, while new exploration technologies may identify previously overlooked deposits.

Artificial intelligence and machine learning show promise for optimizing existing mining operations. These technologies can improve ore sorting, reduce waste, and optimize processing parameters to extract maximum silver from available ore. However, these improvements typically increase recovery rates by only 5-10%, insufficient to offset the broader supply decline trends.

Automated mining equipment reduces labor costs and improves safety but requires substantial capital investment that many silver operations cannot justify. The technology works best in large-scale operations with consistent geology, limiting its application to many smaller silver mines that operate in complex geological environments.

New extraction techniques like in-situ leaching show promise for certain deposit types but remain unproven at commercial scale for most silver deposits. These techniques work best in specific geological conditions and may not be applicable to the majority of remaining silver resources worldwide.

The fundamental challenge is that technology cannot create new high-grade silver deposits or eliminate the geological reality of resource depletion. While innovation can marginally improve efficiency and reduce costs, it cannot solve the underlying problem of declining ore grades and exhausted deposits.

Our physical vs. paper silver analysis explores how mine supply constraints affect different investment approaches and why physical metal becomes increasingly valuable as supply tightens.

Investment and Capital Allocation Challenges

The silver mining industry faces a chronic shortage of development capital that perpetuates supply constraints. Major mining companies increasingly focus on larger-scale gold and copper projects that offer better returns on invested capital. Silver projects, even those with good economics, struggle to compete for capital within diversified mining portfolios.

Junior mining companies, traditionally the source of new silver discoveries, face particular financing challenges. Equity markets for small-cap mining companies remain depressed, making it difficult to raise exploration and development capital. Debt financing is often unavailable for unproven projects, forcing companies to rely on dilutive equity raises that may not provide sufficient capital for full project development.

The capital requirements for modern silver mine development have increased dramatically. Environmental compliance, community engagement, and infrastructure development now represent major cost components that were minimal in previous decades. A greenfield silver mine may require $500 million to $1 billion in development capital—amounts that exceed the capabilities of most junior miners and may not generate adequate returns for major mining companies.

Private equity and institutional investors show limited interest in silver-focused projects compared to gold or diversified commodity investments. Silver's price volatility and smaller market size make it less attractive to institutional capital seeking predictable returns. This capital shortage means many economically viable silver deposits remain undeveloped.

The financing challenge creates a vicious cycle: without adequate capital, new silver mines cannot be developed, perpetuating supply constraints that ultimately justify higher silver prices and better project economics. However, by the time silver prices rise sufficiently to attract development capital, the lead time for new mine development means supply shortages persist for years.

Future Supply Projections and Market Impact

Current trends suggest silver mine supply will continue declining for the foreseeable future, with potential for accelerating declines if economic pressures intensify. Conservative estimates project mine supply falling an additional 5-10% over the next five years as aging mines deplete and few new operations come online to replace lost production.

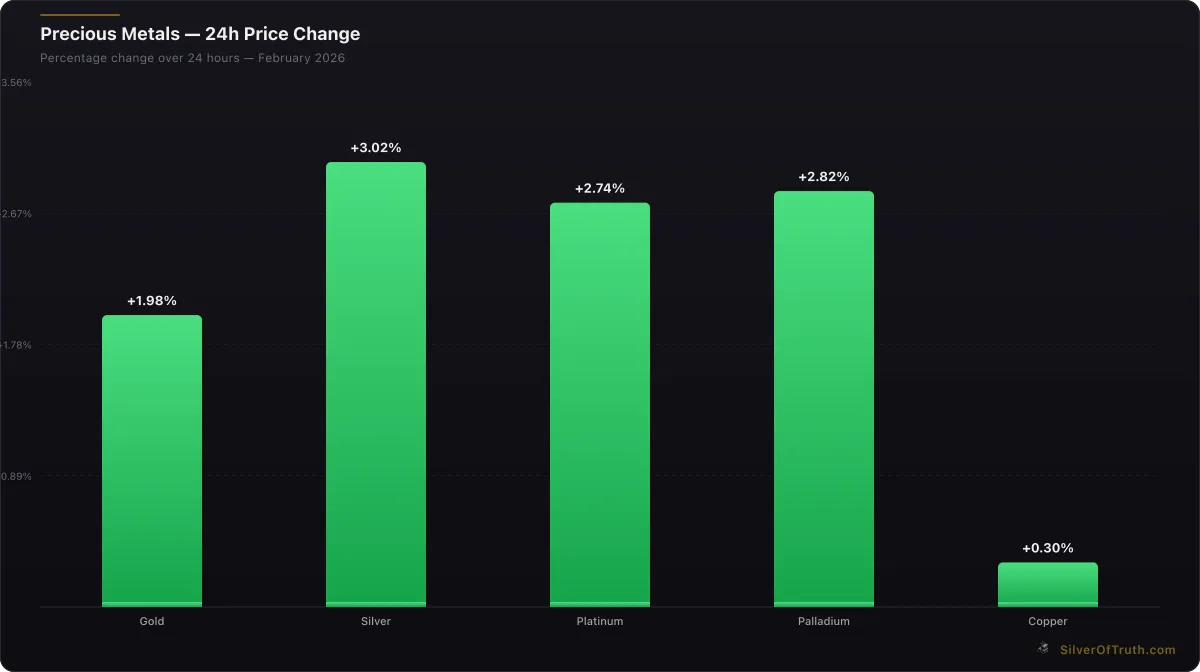

24-hour precious metals price changes. Source: SilverOfTruth, February 2026

The Silver Institute's latest projections indicate total silver supply (including recycling) may fall below 900 million ounces annually within the next decade, down from current levels around 1 billion ounces. This decline occurs while industrial demand continues growing, driven by renewable energy applications, electronics manufacturing, and emerging technologies like 5G networks.

The supply-demand imbalance creates potential for significant price volatility and sustained higher silver prices. However, the timing and magnitude of price responses remain uncertain given the complexity of silver markets and the influence of investment demand, which can fluctuate dramatically based on economic conditions and investor sentiment.

Some analysts project silver prices could reach $100-150 per ounce if supply constraints coincide with strong investment demand driven by monetary policy concerns or economic uncertainty. However, such price levels might eventually incentivize new mine development or increased recycling that could moderate long-term supply shortages.

The implications extend beyond silver prices to affect industrial users who rely on silver for critical applications. Electronics manufacturers, solar panel producers, and automotive companies may face supply constraints that force them to redesign products, substitute alternative materials, or accept higher input costs that ultimately affect consumer prices.

For investors seeking exposure to these supply dynamics, our silver stacking guide provides practical information on building physical silver positions that could benefit from long-term supply constraints.

Global Economic Impact on Silver Mining

Macroeconomic conditions significantly influence silver mine viability and production decisions. Rising interest rates increase mining companies' financing costs while stronger currencies in mining jurisdictions make their silver output less competitive globally. Current monetary policy uncertainty creates additional challenges for long-term mining investment decisions.

Inflation affects mining costs disproportionately since mining is energy and labor intensive. When general inflation rises, mining input costs typically increase faster than silver prices, squeezing profit margins and making marginal operations uneconomical. This relationship partly explains why silver production has declined despite relatively strong silver prices over the past several years.

Currency fluctuations add another layer of complexity. Many major silver mines operate in countries with volatile currencies, creating additional risks for international mining companies. Currency hedging costs reduce project returns, while currency volatility makes long-term planning difficult for operations with multi-decade lifespans.

Global trade policies also affect silver mining competitiveness. Import tariffs on mining equipment or export restrictions on strategic minerals can disadvantage certain mining jurisdictions. Recent trade tensions have created uncertainty that discourages long-term mining investment in some regions.

The interconnected nature of global commodity markets means that silver mining responds to economic conditions affecting other metals and industrial commodities. When broader economic conditions weaken demand for base metals, byproduct silver supply typically falls as well, creating complex feedback loops that are difficult to predict.

FAQ: Silver Mine Supply Decline

Why is silver mine supply declining globally?

Silver mine supply is declining due to multiple interconnected factors: depletion of high-grade deposits discovered decades ago, rising production costs, falling ore grades, and reduced exploration investment. Many mines now process twice as much rock to extract the same amount of silver compared to operations from the 1980s, making production increasingly expensive and environmentally challenging.

How much has global silver production declined?

Global silver mine production peaked at approximately 886 million ounces in 2016 and has since fallen to around 780 million ounces annually—a decline of over 100 million ounces per year. This represents approximately a 12% reduction from peak levels, with several major producing countries showing continued declining trends.

What percentage of silver comes from byproduct mining?

Approximately 70% of silver mine production comes as a byproduct of lead-zinc, copper, and gold mining operations, with only 30% from primary silver mines. This byproduct dependency creates supply vulnerabilities since silver output depends on economic conditions affecting other metals rather than silver market fundamentals alone.

Are there any new major silver discoveries being developed?

Very few major silver discoveries are currently under development. Exploration success rates have declined dramatically, and most major mining companies have reduced silver-focused exploration budgets. The pipeline of new silver projects is extremely limited, with most new discoveries featuring lower ore grades than historical operations.

How do rising mining costs affect silver supply?

Rising mining costs have made many marginal silver operations uneconomical, forcing mine closures and production cuts. All-in sustaining costs for primary silver miners now average $15-20 per ounce compared to $8-12 per ounce a decade ago. Energy costs, labor expenses, and environmental compliance requirements continue increasing faster than silver prices, squeezing profit margins across the industry.

Conclusion

The decline in global silver mine supply represents a fundamental shift in precious metals markets that could have far-reaching implications for both investors and industrial users. With mine production falling over 12% from peak levels while industrial demand continues growing, the structural supply deficit appears likely to persist and potentially worsen in coming years.

The confluence of geological realities—depleted high-grade deposits, declining ore grades, and limited new discoveries—combines with economic pressures from rising costs and reduced capital investment to create supply constraints unprecedented in modern silver markets. Unlike temporary supply disruptions that can be resolved through price adjustments, these challenges reflect long-term trends that may require years or decades to reverse.

For precious metals investors, understanding these supply dynamics provides crucial context for evaluating silver's long-term prospects. The fundamental case for silver strengthens considerably when supply constraints coincide with growing industrial demand and potential investment inflows during periods of economic uncertainty.

Track silver supply developments and inventory trends in real-time with the SilverOfTruth app, available on the App Store. Our comprehensive market intelligence helps investors navigate the complexities of precious metals markets with institutional-grade data and analysis.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, investment, or trading advice. Past performance is not indicative of future results. Always conduct your own research and consult with a qualified financial advisor before making investment decisions. SilverOfTruth provides market data and analysis tools — it does not provide personalized financial advice.