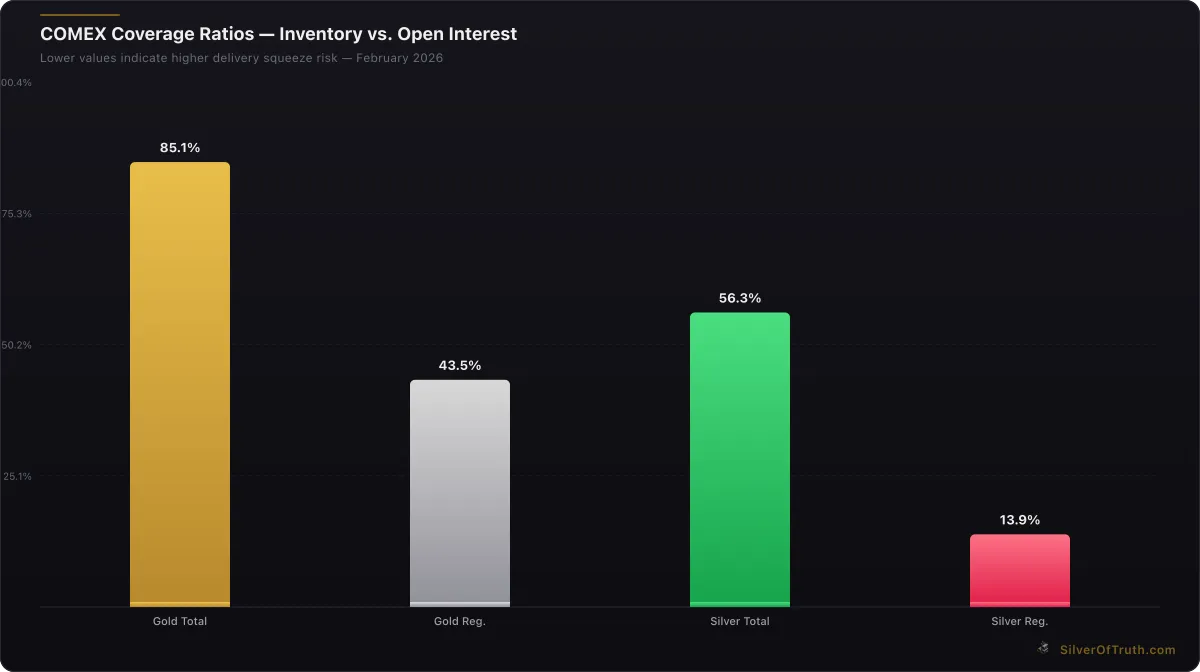

Industrial silver demand is experiencing its most dramatic transformation in decades, with 2026 marking a pivotal year where technology-driven consumption could fundamentally reshape the precious metals market. Current market data shows silver trading at $77.27 per ounce, up 2.1% in 24 hours, while COMEX silver inventory has declined to 376.4 million ounces with a concerning coverage ratio of just 56.3% against open interest.

The confluence of solar energy expansion, electric vehicle adoption, 5G infrastructure deployment, and emerging technologies is creating unprecedented industrial silver demand that threatens to overwhelm traditional mining supply. Understanding these demand drivers is crucial for investors navigating what could become the most significant supply-demand imbalance in silver's modern history.

Solar Energy's Silver Appetite Explosion

Solar panel manufacturing represents the single largest growth driver in silver industrial demand 2026, with photovoltaic installations consuming approximately 130 million ounces annually according to the Silver Institute. Each solar panel requires 15-20 grams of silver for optimal conductivity, making silver irreplaceable in converting sunlight to electricity efficiently.

Global solar capacity additions reached record highs in 2025, with China alone installing over 200 gigawatts of new capacity. The International Energy Agency projects solar installations will double by 2028, requiring an additional 100-150 million ounces of silver annually beyond current consumption levels. This exponential growth trajectory coincides with government renewable energy mandates across major economies.

Silver's unique properties make it indispensable in solar applications. Its electrical conductivity exceeds all other metals, ensuring minimal power loss in photovoltaic cells. While copper alternatives exist, they reduce panel efficiency by 8-12%, making silver the preferred choice despite premium costs. As panel efficiency becomes critical for space-constrained installations, silver demand intensifies.

The solar industry's silver intensity has actually increased over recent years. Early panels used approximately 12 grams per panel, but modern high-efficiency designs require 18-22 grams to achieve optimal performance. This trend toward higher silver content per panel amplifies total demand even if installation growth remained constant.

Regional demand patterns show Asia-Pacific consuming 65% of solar-related silver, with Europe and North America accounting for 20% and 12% respectively. China's dominance in panel manufacturing means its policy decisions directly impact global silver demand. Recent Chinese subsidies for domestic solar installations could add 20-30 million ounces of unexpected demand in 2026 alone.

Recycling from end-of-life solar panels remains minimal, as most installations from the early 2000s solar boom are still operational. The Silver Institute estimates less than 5% of solar silver is currently recovered, creating a one-way consumption pattern that depletes above-ground stocks. Our complete analysis of silver in solar panels explores these dynamics in detail.

Electric Vehicle Revolution Drives Silver Consumption

The electric vehicle sector represents the fastest-growing component of silver industrial demand 2026, with each EV requiring 25-50 grams of silver compared to just 15-28 grams in traditional internal combustion engine vehicles. This 50-80% increase per vehicle occurs as global EV sales approach 15 million units annually, according to World Gold Council automotive sector analysis.

Battery electric vehicles consume the most silver, utilizing the metal in battery management systems, charging infrastructure, and advanced driver assistance systems. Tesla Model S vehicles contain approximately 1.5 ounces of silver each, while luxury EVs can require up to 2 ounces per vehicle. Multiply this by millions of units annually, and the consumption becomes substantial.

Charging infrastructure deployment amplifies silver demand beyond the vehicles themselves. Each DC fast charging station requires 5-8 ounces of silver for power electronics and contactors. The Biden Administration's infrastructure bill allocated $7.5 billion for 500,000 charging stations, representing 2.5-4 million additional ounces of silver demand through 2030.

Autonomous driving features increase silver content per vehicle significantly. LiDAR sensors, radar systems, and advanced computing require high-conductivity connections where silver excels. Level 4 and Level 5 autonomous vehicles could require 75-100 grams of silver each, triple current consumption levels.

Major automakers' electrification timelines create predictable silver demand surges. General Motors pledges 30 new EV models by 2030, while Volvo commits to 100% electric sales by 2030. Ford's Lightning F-150 production ramp alone could consume 500,000-750,000 ounces annually at full capacity.

China dominates EV production and consumption, manufacturing 60% of global electric vehicles while purchasing 50% of new EV sales. Chinese government mandates require 40% of new vehicle sales to be electric by 2030, representing massive silver demand growth. Our detailed analysis of silver in electric vehicles examines these trends comprehensively.

Supply chain constraints already impact silver availability for EV manufacturers. Several automakers report sourcing challenges for silver-intensive components, with lead times extending from 12 weeks to 20-24 weeks in 2025. This suggests industrial demand is beginning to stress traditional supply channels.

5G Infrastructure Creates New Demand Vectors

The global 5G network rollout represents an emerging but rapidly growing source of silver industrial demand 2026, with each 5G base station requiring 3-5 times more silver than previous generation equipment. Network infrastructure upgrades across major economies are creating millions of ounces in additional annual demand.

5G's higher frequencies require superior conductivity to minimize signal loss and heat generation. Silver's electrical properties make it essential in radio frequency components, antennas, and circuit boards. Alternative metals like copper introduce signal degradation that compromises 5G's speed and reliability advantages.

Base station deployment numbers are staggering. China installed over 1.5 million 5G base stations through 2025, with plans for 3 million more by 2030. The United States targets 800,000 new base stations, while Europe plans 1.2 million installations. Each station's 15-25 grams of silver content creates 50-75 million ounces of cumulative demand.

Small cell networks multiply silver demand exponentially. 5G requires dense networks of small cells for urban coverage, with some cities needing one small cell per city block. These installations, while smaller than macro base stations, collectively consume massive silver quantities due to their sheer numbers.

Data center upgrades accompanying 5G deployment further increase silver consumption. Cloud computing infrastructure supporting 5G applications requires high-performance servers with silver-intensive components. Major tech companies' capital expenditure on data centers reached $200 billion in 2025, much incorporating silver-heavy 5G-enabled equipment.

Smartphone and device upgrades create additional demand as consumers replace equipment to access 5G networks. Each 5G-enabled smartphone contains 200-300 milligrams of silver, compared to 150-200 milligrams in 4G devices. With 1.4 billion smartphone sales annually, this represents 280-420 million grams (9-13.5 million ounces) of additional demand.

Our comprehensive guide to silver's 5G demand details how this technology revolution impacts precious metals markets, while our analysis of silver supply deficits examines whether mining can meet these new consumption levels.

Medical and Healthcare Technology Silver Applications

Healthcare technology represents a rapidly expanding sector for silver industrial demand 2026, driven by antimicrobial properties that make silver invaluable in medical devices, wound care, and infection control applications. The COVID-19 pandemic accelerated adoption of silver-based solutions across healthcare systems globally.

Medical device manufacturing consumes increasing silver quantities as devices become more sophisticated and regulations demand higher reliability. Cardiac pacemakers, defibrillators, and surgical instruments utilize silver for its biocompatibility and antimicrobial effects. Each pacemaker contains approximately 1-2 grams of silver, with 1.4 million devices implanted annually worldwide.

Antimicrobial coatings using silver nanoparticles are becoming standard in hospitals and healthcare facilities. Door handles, bed rails, surgical instruments, and air filtration systems increasingly incorporate silver to reduce healthcare-associated infections. This represents a new consumption category that barely existed a decade ago.

Diagnostic equipment upgrades during the pandemic created unexpected silver demand. Digital X-ray systems, CT scanners, and MRI machines require silver for electrical conductivity and electromagnetic shielding. Hospital infrastructure investments totaling $180 billion globally in 2025 incorporated significant silver content.

Wound care products utilizing silver's healing properties consume millions of ounces annually. Silver sulfadiazine creams, antimicrobial dressings, and surgical mesh products prevent infection while promoting healing. An aging global population increases demand for these silver-intensive medical supplies.

Water purification systems for healthcare facilities represent emerging silver demand. Hospitals require ultra-pure water for dialysis, surgical applications, and laboratory use. Silver-based purification systems are replacing traditional chemical treatments, creating steady industrial consumption streams.

Electronics and Technology Hardware Consumption

Traditional electronics manufacturing remains the largest single category of silver industrial demand 2026, consuming approximately 250 million ounces annually according to LBMA industrial usage reports. While mature markets show slower growth, emerging technologies within electronics are accelerating silver consumption rates.

Printed circuit boards in consumer electronics require silver for reliable connections and heat dissipation. Smartphones, tablets, computers, and televisions each contain 150-500 milligrams of silver depending on complexity. With 2.8 billion consumer electronic devices sold annually, this represents substantial ongoing demand.

Automotive electronics beyond EVs are increasing silver content per vehicle. Advanced infotainment systems, navigation equipment, and safety features require high-reliability electrical connections where silver excels. Traditional vehicles now contain 15-28 grams of silver, up from 12-18 grams a decade ago.

Industrial electronics for manufacturing automation and robotics consume growing silver quantities. Each industrial robot contains 1-3 ounces of silver in motor controls, sensors, and communication systems. With industrial robot sales exceeding 500,000 units annually, this represents 500,000-1.5 million ounces of demand.

Internet of Things (IoT) device proliferation creates new silver consumption vectors. Smart home devices, industrial sensors, and connected infrastructure require reliable electrical connections in challenging environments. Silver's durability and conductivity make it essential for IoT applications where replacement is difficult or costly.

Semiconductor manufacturing uses silver in specialized applications where its unique properties are irreplaceable. Advanced chip designs require silver for specific conductivity and thermal management applications. As semiconductor complexity increases, silver content per chip grows proportionally.

Our comprehensive guide to physical silver investing explains how industrial demand impacts investment markets, while our analysis of silver storage options helps investors navigate increasing premiums driven by supply constraints.

Supply-Demand Imbalance Creating Market Stress

The convergence of multiple industrial silver demand growth drivers is creating what analysts describe as the most severe supply-demand imbalance in silver's modern history. Current COMEX silver inventory data shows registered stocks at just 92.9 million ounces, with a concerning coverage ratio of 13.9% against open interest, indicating potential delivery stress.

Source: SilverOfTruth COMEX data, February 2026

COMEX coverage ratios — lower values indicate higher delivery squeeze risk. Source: SilverOfTruth, February 2026

Mine production cannot keep pace with accelerating industrial demand. Global silver mining yields approximately 830 million ounces annually, but this has grown just 1-2% yearly while industrial consumption increases 4-6% annually. The Silver Institute projects a 200 million ounce supply deficit by 2030 if current trends continue.

Recycling rates remain insufficient to bridge the supply gap. Unlike gold, where recycling provides 25-30% of supply, silver recycling contributes only 15-18% due to industrial applications that consume the metal permanently. Solar panels, electronics, and medical devices rarely return silver to the market, creating one-way demand flows.

Above-ground silver inventories are declining rapidly. Our analysis of above-ground silver stocks reveals that readily available silver has decreased 35% since 2015, while industrial demand has increased 40%. This scissors effect threatens market stability as inventories approach critically low levels.

Exchange-traded product demand compounds industrial consumption, removing additional silver from available supply. Silver ETFs hold approximately 1 billion ounces globally, representing metal that cannot serve industrial applications. When combined with private investment demand, total silver sequestered from industrial use exceeds 1.5 billion ounces.

Regional supply constraints are emerging as industrial users compete for limited silver availability. Electronics manufacturers in Asia report sourcing difficulties, while solar panel producers face allocation systems from silver refiners. These supply chain stresses suggest the market is approaching physical limits.

Price premiums for physical silver have expanded significantly, with retail premiums reaching 15-25% above spot prices compared to historical 5-8% levels. This premium expansion reflects growing scarcity of readily available silver for immediate delivery.

The COMEX silver inventory situation shows registered stocks declining weekly, while open interest remains elevated. This dynamic creates potential for delivery squeezes if industrial users or investors demand physical metal from exchange warehouses.

Investment Implications and Portfolio Considerations

Silver industrial demand 2026 creates compelling investment considerations as supply-demand fundamentals suggest potential price appreciation beyond current $77.27 levels. The combination of inelastic industrial demand growth and constrained supply represents a rare commodity investment opportunity.

Industrial users' price sensitivity is limited when silver represents a small percentage of final product costs. Solar panels and EVs remain profitable with silver at $100+ per ounce, suggesting industrial demand will persist through significant price increases. This price inelasticity provides upward price pressure without demand destruction.

Strategic silver shortages could develop as industrial users secure long-term supply agreements. Major electronics and solar manufacturers are reportedly negotiating multi-year silver supply contracts, potentially removing millions of ounces from spot market availability. These supply agreements create artificial scarcity for remaining market participants.

Physical silver investment becomes increasingly attractive as industrial demand reduces available supplies. Coins, bars, and allocated storage products provide direct exposure to the supply-demand imbalance without counterparty risks inherent in paper silver products.

Mining stock investments offer leveraged exposure to higher silver prices driven by industrial demand. Silver miners' production costs remain relatively stable while selling prices could increase substantially if supply deficits materialize. However, investors should research individual companies' production profiles and cost structures carefully.

Geographic diversification matters as regional supply constraints emerge. Asian silver supplies may face greatest stress due to concentrated industrial demand, while North American and European suppliers might command premiums. Our guide to silver bars vs coins helps investors choose appropriate physical formats.

Portfolio allocation considerations suggest silver's industrial demand story differs fundamentally from gold's monetary role. While gold serves as wealth preservation, silver offers potential appreciation driven by irreplaceable industrial consumption growth. This creates different risk-return profiles for precious metals investors.

Frequently Asked Questions

What drives silver industrial demand growth in 2026? Solar energy expansion, electric vehicle adoption, 5G infrastructure deployment, and medical technology advancement create unprecedented silver consumption. Solar panels require 15-20 grams each, EVs need 25-50 grams, and 5G base stations consume 15-25 grams of silver for optimal performance.

How does industrial demand affect silver prices? Industrial users show limited price sensitivity since silver represents small percentages of final product costs. Solar panels and EVs remain profitable with silver above $100/oz, creating inelastic demand that supports higher prices without consumption reduction.

Can silver mining increase to meet industrial demand? Global silver production grows 1-2% annually while industrial consumption increases 4-6% yearly. The Silver Institute projects 200 million ounce supply deficits by 2030, suggesting mining cannot match demand growth without significant price increases.

What happens if silver becomes too expensive for industrial use? Silver's unique conductivity and antimicrobial properties make substitution difficult in critical applications. Solar efficiency drops 8-12% with copper alternatives, while 5G performance degrades with inferior conductors. Most industrial users will pay higher prices rather than compromise product performance.

How do supply constraints affect silver investors? Physical premiums are expanding as industrial demand competes with investment demand for limited supplies. COMEX registered inventory shows concerning coverage ratios, while above-ground stocks decline. These dynamics suggest potential price appreciation and supply chain stress for physical silver purchases.

Conclusion

Silver industrial demand 2026 represents a fundamental shift in precious metals markets, where technology-driven consumption creates unprecedented supply-demand dynamics. Solar energy expansion requiring 130 million ounces annually, EV adoption consuming growing silver quantities, and 5G infrastructure deployment demanding millions of additional ounces annually are reshaping the silver market permanently.

The convergence of multiple demand drivers with constrained mining supply and declining above-ground inventories suggests significant market stress ahead. Current COMEX data showing 56.3% coverage ratios and registered inventory declines provide early warning signals of potential delivery constraints.

For investors seeking exposure to these powerful industrial demand trends, the SilverOfTruth app provides real-time COMEX inventory tracking, coverage ratio monitoring, and comprehensive precious metals market analysis. Track these developing supply-demand imbalances and delivery risks with institutional-grade data available on the App Store.

The silver market's transformation from primarily monetary metal to critical industrial commodity creates unique investment opportunities for those positioned ahead of the supply-demand squeeze. Understanding these industrial demand drivers becomes essential for navigating what could become the most significant precious metals market development in decades.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, investment, or trading advice. Past performance is not indicative of future results. Always conduct your own research and consult with a qualified financial advisor before making investment decisions. SilverOfTruth provides market data and analysis tools — it does not provide personalized financial advice.