Silver's deficit isn't a temporary market hiccup—it's a structural reality fundamentally reshaping the precious metals landscape. Unlike cyclical imbalances that markets eventually correct, silver's deficit structural pattern stems from irreversible technological shifts and declining primary production that create a permanent silver deficit extending far beyond current market cycles.

The numbers tell a stark story. According to the Silver Institute's latest World Silver Survey, global silver demand has exceeded mine production for three consecutive years, with the deficit widening to 237.7 million ounces in 2023. This isn't weather-related mine disruption or temporary investment buying—it's the new normal driven by forces that won't reverse.

Understanding why this silver deficit long term represents a fundamental shift requires examining the underlying structural changes in both supply and demand that make this imbalance self-reinforcing rather than self-correcting. From 5G infrastructure to solar panel manufacturing, the industrial applications driving silver consumption are expanding exponentially while primary mine production faces geological and economic constraints that traditional market mechanisms cannot resolve.

The Industrial Demand Revolution

Technology's Insatiable Silver Appetite

Modern technology has transformed silver from a monetary metal with some industrial uses into an absolutely critical industrial commodity that happens to retain investment demand. The difference is profound and permanent.

Electronics manufacturing alone consumed 250 million ounces of silver in 2023, representing 24% of total demand according to World Gold Council industrial metals data. Unlike jewelry or investment demand, which responds to price signals, electronic applications require silver's unique properties—highest electrical and thermal conductivity of all elements—with no viable substitutes at current technology levels.

The 5G rollout exemplifies this structural shift. Each 5G base station requires 3-5 times more silver than 4G infrastructure due to increased antenna complexity and heat dissipation needs. With global 5G deployments accelerating, this demand component alone adds tens of millions of ounces annually to baseline consumption. Our analysis of silver's growing demand in 5G technology details how telecommunications infrastructure creates sustained, price-inelastic demand.

Solar photovoltaic panels present an even larger structural demand driver. Each gigawatt of solar capacity requires approximately 1 million ounces of silver for the conductive paste that captures and transfers electrical current. Global solar installations reached 191 GW in 2022 and continue expanding as countries pursue renewable energy targets. Unlike cyclical demand, these installations represent permanent silver consumption—the metal becomes integral to the infrastructure and cannot be easily recovered.

Medical and Automotive Applications

Healthcare applications demonstrate how industrial silver demand becomes embedded in essential infrastructure. Silver's antimicrobial properties make it irreplaceable in medical devices, wound dressings, and hospital equipment. The COVID-19 pandemic accelerated adoption of silver-based antimicrobial technologies, creating a new baseline demand level that persists regardless of precious metals investment cycles.

Automotive electronics represent another structural demand category expanding with electric vehicle adoption. Modern vehicles contain 1-3 ounces of silver in electrical systems, with EVs requiring even higher amounts due to sophisticated battery management and charging systems. As transportation electrifies globally, this automotive silver demand grows independently of precious metals market sentiment.

Supply Side Structural Constraints

Primary Mine Production Decline

Silver's supply structure creates permanent constraints that cannot respond quickly to price signals. Unlike above-ground investment silver that can flow back to markets during price spikes, primary mine production faces geological and economic realities that prevent rapid expansion.

Only about 30% of global silver production comes from primary silver mines. The remaining 70% arrives as a byproduct of base metal mining—copper, lead, zinc, and gold operations where silver is secondary. This byproduct structure means silver supply depends heavily on demand for other metals rather than silver prices alone.

Primary silver mines face grade depletion issues that compound over time. Average silver ore grades have declined from 20+ ounces per ton in the 1900s to under 8 ounces per ton today at many operations. Lower grades require processing more material to produce the same amount of silver, increasing energy costs and environmental impacts while reducing profit margins.

Geological surveys indicate that high-grade silver deposits are becoming increasingly rare. New discoveries tend to be lower grade, more complex metallurgy, or located in challenging jurisdictions. This means new mine development requires higher silver prices to justify investment, while existing mines experience declining output as they exhaust higher-grade zones.

Byproduct Supply Vulnerability

The byproduct nature of most silver supply creates structural vulnerability during base metal downturns. When copper or lead prices decline, mining companies may reduce production or close mines entirely, cutting silver supply as an unintended consequence. This dynamic makes silver supply less responsive to silver-specific demand increases.

Environmental regulations add another structural constraint. Modern mining faces stricter environmental standards that increase costs and development timelines. Many potential silver projects require 7-10 years from discovery to production, meaning current deficits cannot be quickly resolved even if silver prices incentivize new development.

Labor and energy costs represent additional structural headwinds. Mining is energy-intensive, and electricity costs have risen substantially in many mining jurisdictions. Skilled mining labor has become scarce in some regions, increasing operational costs for existing mines while complicating new project development.

Government and Central Bank Behavior

Strategic Metal Recognition

Governments increasingly recognize silver as a strategic material critical for renewable energy and defense applications. This recognition leads to policies that prioritize domestic supply security over pure market dynamics. China, the world's largest silver producer, has implemented policies encouraging domestic consumption while limiting exports during supply tightness.

Central banks, traditionally focused on gold reserves, are beginning to acknowledge silver's strategic importance. While not yet acquiring silver reserves at scale, several central banks have commissioned studies on critical metal supply chains that include silver. This evolving perspective could eventually translate into official sector demand that competes with industrial users.

The U.S. Defense Production Act now includes silver in critical materials assessments, recognizing its importance for defense electronics and renewable energy infrastructure. Such classifications can lead to stockpiling programs or supply chain security initiatives that remove additional silver from commercial markets.

Market Structure Changes

Investment Demand Evolution

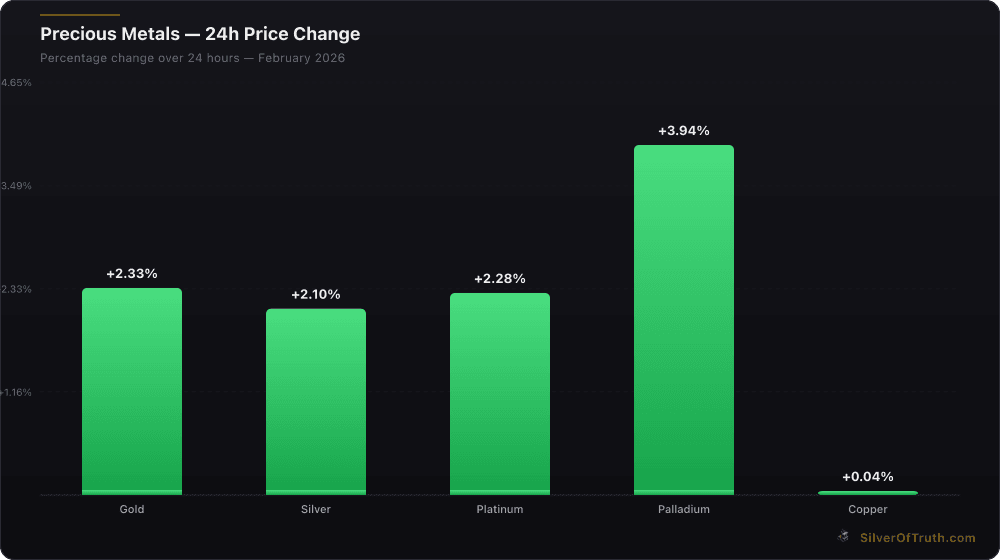

24-hour precious metals price changes. Source: SilverOfTruth, February 2026

Investment demand for silver has evolved beyond traditional safe-haven purchases during financial stress. Environmental, Social, and Governance (ESG) investing has created demand for "green metals" essential to renewable energy infrastructure. Silver's role in solar panels and wind turbines makes it attractive to ESG-focused investors seeking exposure to the energy transition.

Exchange-traded products (ETPs) have fundamentally changed how investment silver demand impacts the physical market. Major silver ETFs hold over 900 million ounces collectively, representing physical metal removed from industrial supply chains. Unlike futures contracts that can be cash-settled, ETPs require actual silver backing, creating persistent demand that doesn't fluctuate with short-term sentiment.

Digital asset developments have created new silver investment vehicles that appeal to younger investors. Fractional ownership platforms and blockchain-based silver tokens expand the investor base beyond traditional precious metals buyers, potentially creating sustained investment demand from demographics that historically showed little interest in physical precious metals.

Economic Factors Supporting Structural Deficit

Currency Debasement Trends

Global monetary policy trends support long-term precious metals demand that compounds the structural deficit. With central banks maintaining accommodative policies and government debt levels reaching historical highs, currency debasement concerns drive ongoing investment demand for silver as monetary insurance.

Inflation persistence in developed economies, despite central bank efforts, maintains silver's appeal as a real asset hedge. Unlike previous decades when inflation was considered transitory, current inflationary pressures stem from structural factors—supply chain deglobalization, energy transition costs, demographic changes—that support sustained precious metals investment demand.

Geopolitical tensions encourage diversification away from financial assets tied to specific currencies or jurisdictions. Silver's physical nature and global acceptance make it attractive for investors seeking assets independent of particular financial systems, creating demand that persists regardless of traditional economic cycles.

Wealth Preservation in Developing Markets

Emerging market wealth creation generates additional silver investment demand as new affluent classes seek portfolio diversification beyond local financial systems. Countries experiencing currency instability or financial system concerns often see increased precious metals demand as citizens preserve wealth in tangible assets.

Demographic trends in developing countries support this dynamic. Younger populations in countries like India and China show increasing interest in precious metals investing, often through digital platforms that make small-amount purchases accessible. This demographic shift creates ongoing investment demand that adds to industrial consumption.

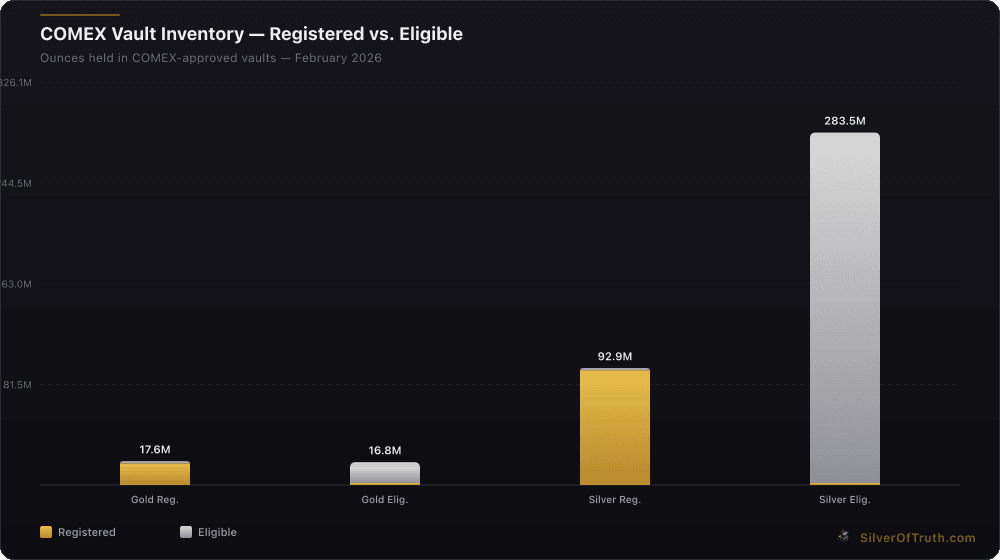

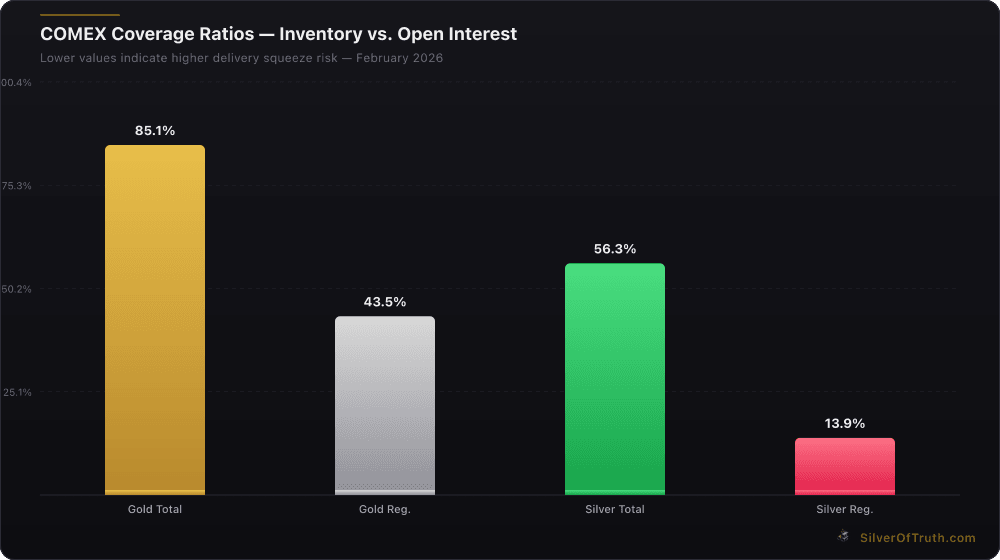

COMEX Inventory and Physical Market Stress

Current COMEX silver registered inventory stands at 92.9 million ounces against open interest of 133,641 contracts, creating a coverage ratio of just 13.9%—well below levels that historically indicate adequate physical supply backing paper positions. This tight inventory situation reflects the broader structural deficit as industrial users and investors compete for available supplies.

Source: SilverOfTruth COMEX data, February 2026

COMEX coverage ratios — lower values indicate higher delivery squeeze risk. Source: SilverOfTruth, February 2026

The distinction between eligible and registered inventory becomes crucial during structural deficits. Eligible silver represents metal held in COMEX warehouses but not available for delivery against futures contracts. Total COMEX silver inventory of 376.4 million ounces includes 283.5 million eligible ounces that might not flow to the market during delivery periods, concentrating pressure on the smaller registered component.

Our analysis of COMEX registered vs eligible dynamics explains how structural deficits can create delivery complications when physical demand exceeds registered supplies. Unlike temporary shortages that can be resolved by converting eligible to registered inventory, structural deficits reflect genuine supply tightness that cannot be easily alleviated.

Industrial users increasingly bypass paper markets entirely, securing silver through direct mining company contracts or tolling arrangements that guarantee supply outside exchange-traded markets. This "financialization reversal" removes silver from speculative trading while ensuring industrial supply chains remain intact, further tightening availability for investment and trading purposes.

The Recycling Reality Check

Recycling Cannot Fill the Gap

Silver recycling, while environmentally beneficial, cannot structurally resolve the deficit due to technological constraints and economic realities. Electronic applications, representing the largest industrial demand category, typically involve such small amounts per device that collection and processing costs exceed recovery value except at very high silver prices.

According to LBMA recycling statistics, global silver recycling recovered approximately 180 million ounces in 2023, primarily from jewelry, silverware, and some industrial applications. However, much of the silver consumed in modern electronics, solar panels, and medical applications becomes permanently embedded or consumed, making recovery economically unfeasible.

Photovoltaic panel recycling presents particular challenges. Solar panels have 25-30 year lifespans, meaning silver consumed today won't return to markets until the 2050s. Even then, panel recycling remains expensive and complex, with no guarantee that recovered silver will be economically competitive with mined supply.

The recycling rate for silver from electronic waste remains below 20% globally, according to United Nations e-waste monitoring data. Collection challenges, processing costs, and the dispersed nature of electronic silver consumption mean that recycling cannot scale to offset growing industrial demand, making the structural deficit self-reinforcing.

Long-Term Implications for Silver Markets

Price Discovery Mechanism Changes

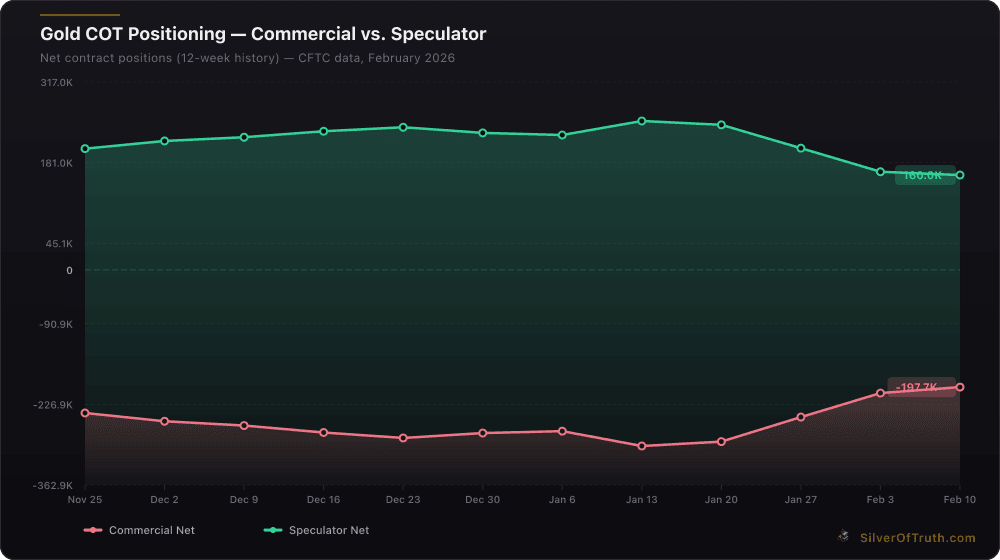

Gold COT positioning: commercial hedgers (red) vs. speculators (green). Source: CFTC via SilverOfTruth, February 2026

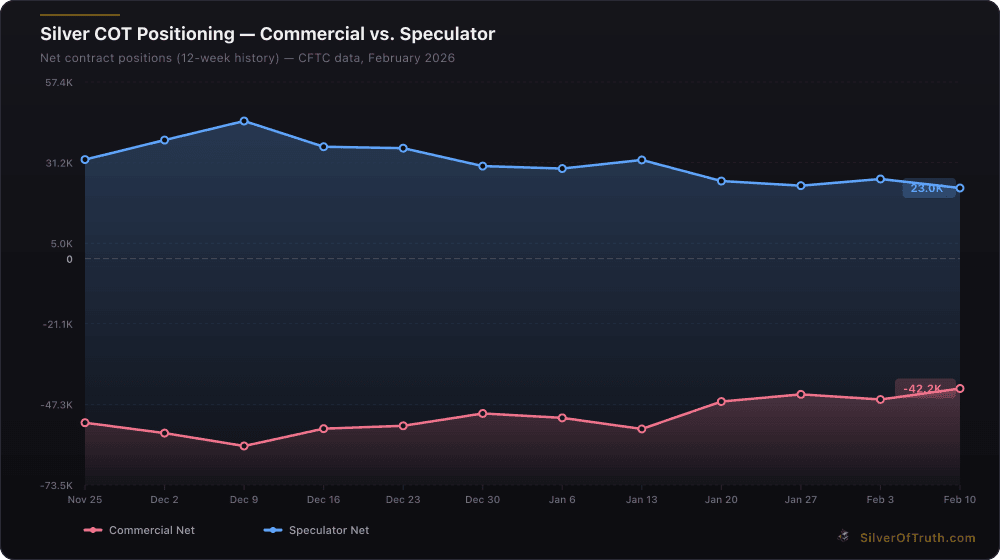

Silver COT positioning: commercial hedgers (red) vs. speculators (blue). Source: CFTC via SilverOfTruth, February 2026

Structural deficits fundamentally alter how silver prices are discovered and established. Traditional precious metals pricing relied heavily on investment sentiment, central bank policies, and speculative positioning. Structural industrial demand creates a price floor based on actual consumption needs rather than financial market sentiment alone.

Industrial users demonstrate willingness to pay premiums above spot prices to secure reliable supply, as evidenced by direct mining company contracts and tolling arrangements that guarantee delivery outside exchange markets. This price discovery occurs largely outside visible futures markets, potentially causing official prices to lag underlying physical market dynamics.

The development of industrial silver stockpiles by major technology companies represents another structural change. Companies like Tesla, Samsung, and major solar manufacturers maintain strategic inventory levels to ensure production continuity, creating demand that persists even during precious metals bear markets.

Investment Strategy Implications

Understanding silver's structural deficit requires rethinking traditional precious metals investment approaches. Unlike gold, where investment demand drives price discovery, silver's industrial foundation creates different risk-return profiles and timing considerations.

Our comprehensive guide on silver stacking strategies addresses how structural deficits impact accumulation approaches, while our analysis of physical vs paper silver explains why structural deficits favor physical ownership over financial derivatives.

The permanent nature of silver's structural deficit suggests that traditional cyclical analysis may prove inadequate. Instead, investors must consider technological adoption curves, renewable energy deployment schedules, and industrial capacity expansion as primary drivers rather than monetary policy or currency movements alone.

Frequently Asked Questions

Q: How long will silver's structural deficit persist? A: The structural deficit appears permanent based on current technology trends. Industrial demand growth from 5G, solar energy, electric vehicles, and electronics shows no signs of slowing, while primary mine production faces ongoing constraints. Unless breakthrough recycling technologies emerge or silver substitutes are developed, the deficit should persist indefinitely.

Q: Can higher prices eventually balance silver supply and demand? A: Higher prices may encourage some additional mining and recycling, but silver's byproduct nature means supply doesn't respond quickly to price signals. Most silver comes from base metal mines where silver is secondary, so production depends more on copper, lead, and zinc demand than silver prices. Additionally, many industrial applications are relatively price-inelastic since silver represents a small component of final product costs.

Q: What price level would be needed to balance the silver market? A: Economic analysis suggests silver prices would need to reach $150-200 per ounce to incentivize enough additional mining and recycling to balance supply and demand. However, at those prices, some industrial applications might find substitutes, potentially reducing demand. The interaction between higher prices, supply response, and demand destruction makes exact price targets difficult to predict.

Q: How does silver's structural deficit compare to other metals? A: Silver's deficit is unique among precious metals due to its combination of monetary properties and critical industrial applications. While lithium, cobalt, and rare earth elements also face structural deficits, they lack silver's investment demand component. Gold faces occasional deficits, but its primarily monetary role makes supply-demand balancing different from silver's industrial reality.

Q: Could technological substitution eliminate silver's industrial demand? A: Current technology offers no viable substitutes for silver's electrical and thermal conductivity properties in most applications. While researchers explore alternatives like copper nanowires or graphene, these remain experimental and haven't achieved silver's performance characteristics at commercial scale. The physics of electrical conductivity make finding silver substitutes particularly challenging.

The evidence overwhelmingly supports that silver's deficit represents a structural, permanent shift rather than a temporary imbalance. Industrial demand continues expanding through technological adoption while supply faces geological and economic constraints that cannot be quickly resolved. This creates an investment environment where physical silver ownership becomes increasingly attractive as the structural deficit persists and potentially widens.

For investors seeking exposure to this structural trend, the SilverOfTruth app provides real-time COMEX inventory tracking, industrial demand analysis, and supply chain monitoring tools essential for navigating silver's evolving market dynamics. Track inventory levels, coverage ratios, and delivery trends that reflect the ongoing structural deficit directly from the App Store.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, investment, or trading advice. Past performance is not indicative of future results. Always conduct your own research and consult with a qualified financial advisor before making investment decisions. SilverOfTruth provides market data and analysis tools — it does not provide personalized financial advice.