The global 5G rollout is creating an unprecedented surge in silver demand that coincides with concerning COMEX inventory dynamics. With silver trading at $77.81 per ounce and COMEX total inventory at 376.4 million ounces—down 0.7% recently—the intersection of explosive 5G infrastructure growth and tightening physical supply presents both opportunity and risk for precious metals investors. As telecommunications companies race to deploy 5G networks worldwide, silver's unique conductive properties make it irreplaceable in critical components, from antenna arrays to high-frequency circuits. This analysis examines how 5G technology is reshaping silver demand patterns while understanding COMEX inventory fluctuations reveals the supply-side vulnerabilities that could amplify this industrial demand story.

Quick Answer: 5G technology requires significantly more silver per device than 4G due to higher frequencies and complex antenna systems, creating structural demand growth of 15-20% in telecommunications applications. With COMEX silver inventory showing a concerning 52.6% coverage ratio against open interest, this industrial demand surge could exacerbate existing supply tightness and drive prices higher.

What Makes Silver Essential for 5G Infrastructure?

Silver's exceptional electrical conductivity—the highest of all elements—makes it indispensable for 5G technology's high-frequency operations. Unlike 4G networks that operate primarily in sub-6GHz frequencies, 5G utilizes millimeter wave (mmWave) frequencies up to 100GHz, where signal loss becomes critical. According to LBMA market data, silver's conductivity at 63.0 × 10^6 S/m significantly exceeds copper's 59.6 × 10^6 S/m, making it essential for minimizing signal degradation in high-frequency applications.

The technical requirements of 5G create multiple silver demand drivers. Massive MIMO (Multiple Input, Multiple Output) antenna systems, which can contain 64 to 256 antenna elements compared to 4G's typical 2-8 antennas, require silver-based conductive pastes and traces for optimal performance. Each 5G base station contains approximately 3-5 times more silver than its 4G predecessor, primarily in printed circuit boards, antenna elements, and RF (radio frequency) components.

Small cell deployments further amplify silver consumption. 5G networks require dense networks of small cells—low-power base stations covering smaller areas—to maintain signal quality at higher frequencies. The Federal Communications Commission estimates that full 5G deployment will require 800,000 to 1 million new small cell installations in the United States alone, each incorporating silver-based components for signal integrity.

Device-level demand compounds infrastructure requirements. 5G smartphones contain 15-20% more silver than 4G devices due to additional antenna systems, enhanced processing capabilities, and improved heat dissipation requirements. With global 5G smartphone shipments projected to exceed 1.2 billion units annually by 2026, according to industry analysts, this represents a substantial incremental demand stream for industrial silver applications.

How Much Additional Silver Demand Does 5G Create?

Quantifying 5G's silver demand impact requires examining both infrastructure and device consumption patterns. Infrastructure deployment creates the most immediate demand surge, with each 5G macro base station requiring 20-30 grams of silver compared to 4G's 10-15 grams. Small cell deployments, while using less silver per unit at 5-8 grams each, contribute significantly through sheer volume—density requirements mean 10-20 small cells per macro cell in urban areas.

Regional deployment schedules reveal the demand timeline. China leads 5G infrastructure rollout with over 2.3 million base stations operational, creating an estimated 150-200 metric tons of silver demand annually for network expansion and maintenance. The United States lags with approximately 100,000 5G sites but aims for 500,000+ by 2027, potentially generating 75-100 metric tons of additional annual silver consumption.

Europe's 5G deployment, while slower than Asia, targets 75% population coverage by 2025 across 27 EU member states. This geographic expansion translates to roughly 400,000 new base station installations, consuming an estimated 80-120 metric tons of silver over the deployment period. India's emerging 5G market, with plans for 500,000+ base stations by 2025, could add another 100 metric tons to annual industrial demand.

The Silver Institute's latest World Silver Survey indicates that telecommunications applications consumed 45 million ounces (1,400 metric tons) of silver in 2025, representing a 12% increase from pre-5G levels. Industry projections suggest this could reach 55-60 million ounces annually by 2028 as 5G deployment accelerates globally, creating structural demand growth that mining supply struggles to match.

Device-side consumption adds another layer of demand. Beyond smartphones, 5G enables Internet of Things (IoT) device proliferation—from autonomous vehicles to smart city infrastructure—each incorporating silver-based components. Automotive 5G applications alone could consume an additional 10-15 million ounces annually as connected and autonomous vehicles become mainstream, with each vehicle requiring 15-25 grams of silver for 5G communication systems.

Why Are Current COMEX Silver Inventory Levels Concerning?

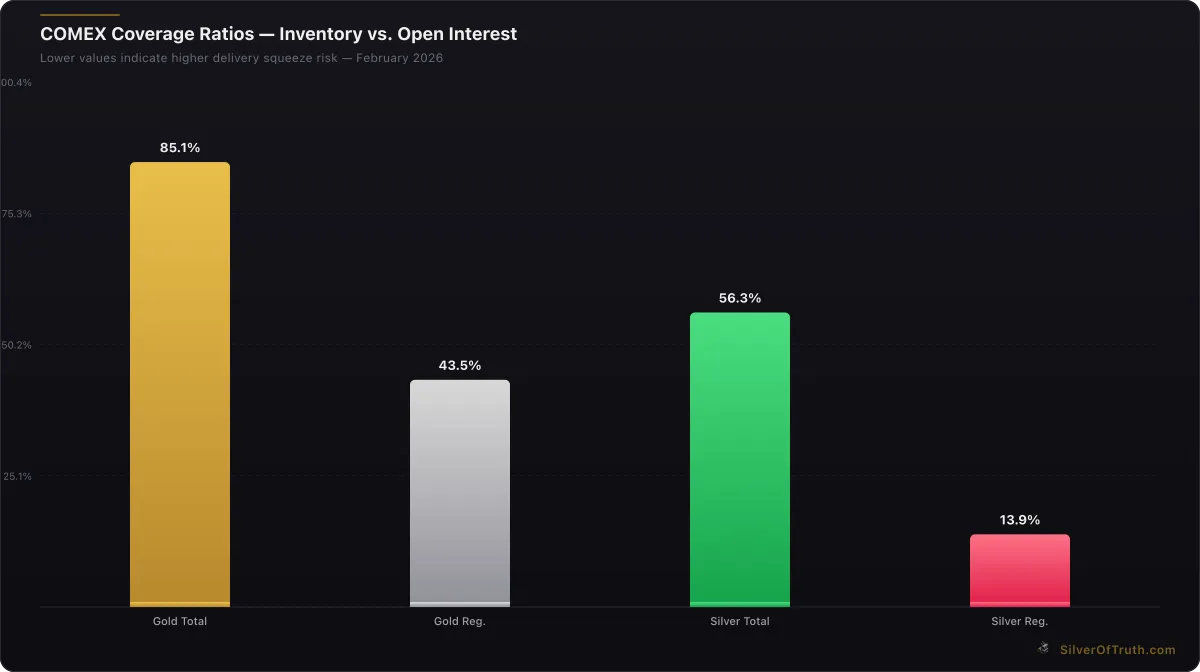

COMEX silver inventory dynamics reveal troubling supply-side vulnerabilities that 5G demand could exploit. Total inventory currently stands at 376.4 million ounces, comprising 283.5 million ounces eligible and 92.9 million ounces registered for delivery. The registered portion—immediately available for contract settlement—represents a concerning 52.6% coverage ratio against current open interest of 143,180 contracts (715.9 million ounces equivalent).

Source: SilverOfTruth COMEX data, February 2026

COMEX coverage ratios — lower values indicate higher delivery squeeze risk. Source: SilverOfTruth, February 2026

This coverage ratio indicates potential delivery stress if industrial demand increases substantially. Historical analysis shows that coverage ratios below 50% often coincide with price volatility and delivery complications, as seen during the March 2020 market stress when ratios fell below 30% and caused significant supply disruptions. Current levels at 52.6% provide minimal buffer against sustained industrial buying.

Weekly inventory changes compound concerns. Recent COMEX silver inventory data shows persistent drawdowns in registered stocks, with fluctuations reaching -0.7% in single weeks. While total inventory remains substantial, the registered-to-eligible ratio of 1:3 suggests limited immediately deliverable supply relative to potential demand from 5G infrastructure projects requiring physical silver procurement.

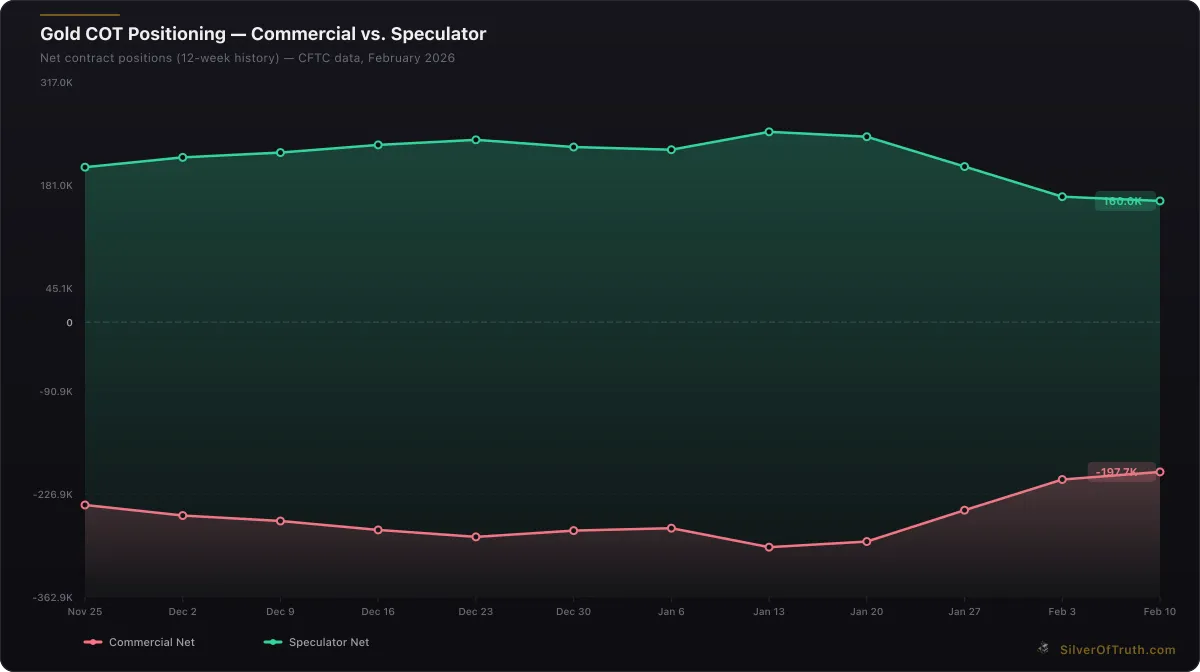

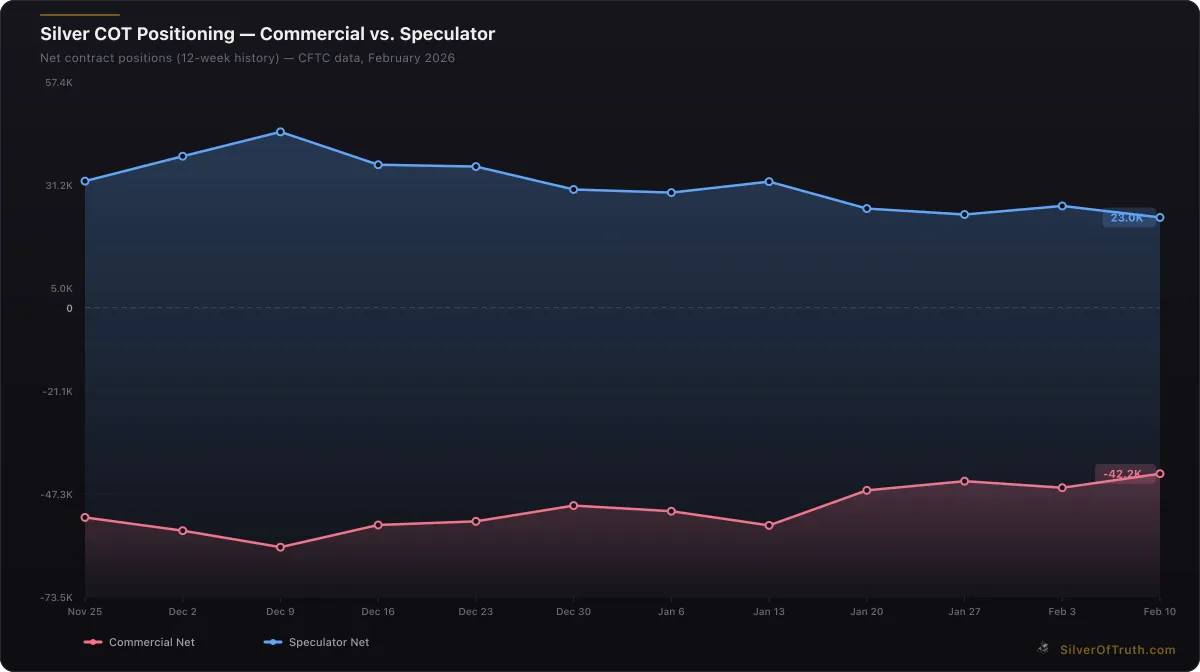

The concentration of COMEX shorts among commercial participants adds another risk dimension. According to CFTC COT reports, commercial traders hold net short positions of -45,725 contracts, representing significant hedging activity by mining companies and industrial users. If 5G demand accelerates beyond mining supply capacity, these shorts could face delivery pressure, potentially forcing cash settlement or physical procurement at higher prices.

Open interest patterns reveal market positioning ahead of potential 5G demand surge. At 143,180 contracts, current open interest remains elevated compared to historical averages, with managed money holding modest net long positions of +4,983 contracts. This relatively balanced positioning could amplify price movements if industrial buying creates sustained upward pressure on physical silver markets.

What Do Global Supply Chain Dynamics Reveal About 5G Silver Demand?

Supply chain analysis reveals how 5G deployment creates cascading silver demand effects throughout the electronics manufacturing ecosystem. Printed Circuit Board (PCB) manufacturers report 25-40% increases in silver paste consumption for 5G applications compared to 4G products, driven by higher density interconnects and improved thermal management requirements. Major PCB suppliers in Taiwan and South Korea indicate they've increased silver inventory holdings by 15-20% to meet 5G production schedules.

Antenna manufacturing presents the most concentrated demand impact. Companies like Laird Connectivity and Molex report that 5G antenna production requires specialized silver-bearing alloys and conductive inks that weren't necessary for previous generation technologies. Multi-layer antenna structures for mmWave applications can contain 2-3 times more silver per unit than traditional antennas, creating supply bottlenecks when major telecommunications equipment orders surge.

Geographic concentration of 5G manufacturing creates regional silver demand hotspots. China's dominance in telecommunications equipment production through companies like Huawei, ZTE, and local manufacturers generates concentrated silver consumption in specific industrial zones. The Pearl River Delta region alone accounts for approximately 30% of global 5G equipment production, creating localized silver demand that can strain regional supply chains and affect pricing dynamics.

Just-in-time manufacturing practices amplify supply sensitivity. Unlike traditional industries with longer supply cycles, electronics manufacturers maintain minimal silver inventory to reduce working capital requirements. When 5G orders surge—often tied to government deployment mandates or carrier infrastructure commitments—manufacturers must procure silver quickly, creating spot demand spikes that can overwhelm normal supply channels.

The shift toward domestic supply chains following geopolitical tensions adds complexity. U.S. and European efforts to reduce dependence on Chinese 5G equipment manufacturers create new regional demand centers that lack established silver supply relationships. This geographic diversification of 5G production could reduce supply chain efficiency and increase silver procurement costs in developing manufacturing hubs.

How Does 5G Silver Demand Compare to Other Industrial Applications?

Contextualizing 5G within broader industrial silver consumption reveals its relative importance and growth trajectory. Solar photovoltaic panels remain the largest industrial silver application at approximately 130 million ounces annually, but growth rates are slowing as manufacturers optimize silver content through thinner paste applications and alternative materials research. In contrast, 5G represents one of the fastest-growing segments with 15-20% annual demand growth expected through 2028.

Automotive applications provide an interesting comparison point. Traditional automotive silver consumption—primarily in electrical contacts and components—totals roughly 55 million ounces annually with steady 3-5% growth. However, electric vehicles and autonomous driving technologies incorporating 5G connectivity could add another 20-30 million ounces of demand by 2030, creating synergistic demand patterns between automotive electrification and telecommunications advancement.

Electronics manufacturing more broadly consumes approximately 240 million ounces annually across all applications, making it silver's largest demand sector. 5G applications currently represent 15-18% of electronics demand but could reach 25-30% by 2028 as deployment accelerates. This rapid growth within the largest demand sector creates compounding effects on overall industrial silver consumption.

Medical applications, while smaller at 25 million ounces annually, demonstrate how technological advancement drives silver demand evolution. Advanced medical devices increasingly incorporate wireless connectivity for remote monitoring and data transmission, with 5G enabling real-time patient data streaming that requires silver-based circuits and antennas. This convergence of healthcare technology and telecommunications creates additional incremental demand streams.

The key differentiator for 5G demand lies in its structural nature and limited substitution potential. Unlike some industrial applications where manufacturers actively research silver alternatives to reduce costs, 5G's performance requirements make silver substitution extremely difficult without significant performance degradation. This creates more durable demand that's less sensitive to silver price increases than cost-conscious applications like solar panels.

What Investment Implications Does 5G Silver Demand Create?

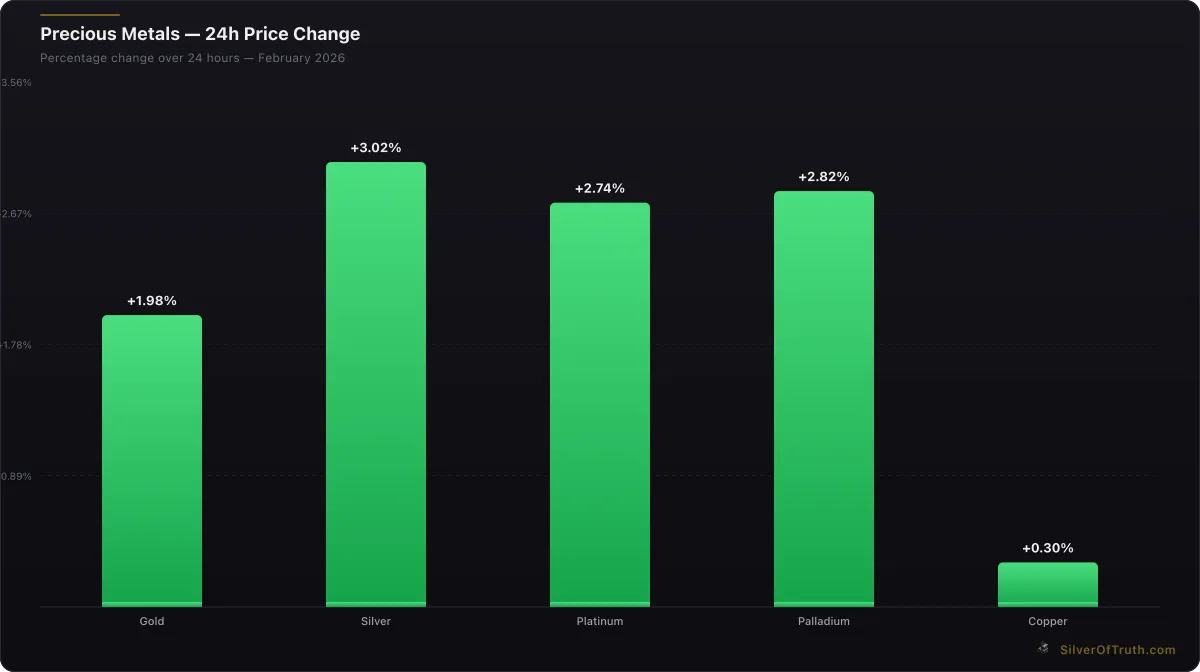

The investment thesis for 5G-driven silver demand centers on structural supply-demand imbalances that price discovery mechanisms haven't fully recognized. With silver trading at $77.81 per ounce and a gold-silver ratio of 65.0, traditional precious metals relationships may not capture the industrial demand dynamics that 5G creates. Track current pricing developments with our live silver price tracker to monitor how 5G news affects market valuations.

24-hour precious metals price changes. Source: SilverOfTruth, February 2026

Physical silver investment strategies could benefit from 5G demand acceleration. Unlike speculative demand that can reverse quickly, industrial consumption represents committed purchasing that occurs regardless of investment sentiment. 5G infrastructure projects typically involve multi-year procurement contracts that provide sustained silver buying support, creating a demand floor that investment demand builds upon. This fundamental support could reduce downside volatility during precious metals bear markets.

Mining stock investment implications vary by company exposure to industrial demand. Primary silver miners like First Majestic Silver and Hecla Mining benefit directly from sustained industrial buying that reduces price volatility and supports margin expansion. Silver streaming companies such as Wheaton Precious Metals provide leveraged exposure to price appreciation without operational risks, potentially outperforming during 5G-driven demand acceleration.

Exchange-traded fund (ETF) flows could amplify 5G demand effects. Physical silver ETFs like SLV and PSLV must purchase silver to back new share creation, creating additional demand when 5G news drives investment inflows. With current ETF holdings exceeding 600 million ounces globally, even modest percentage inflows could generate significant physical demand that compounds industrial procurement.

The timing of investment positioning matters given 5G deployment schedules. Peak 5G infrastructure deployment typically occurs 2-3 years after spectrum auctions and regulatory approvals, suggesting 2026-2028 could represent peak demand impact years. Early positioning ahead of this demand surge could capture both fundamental price appreciation and speculative momentum as markets recognize 5G's silver consumption implications.

Options and derivatives markets present additional opportunities for sophisticated investors. Silver call options could benefit from volatility spikes when 5G deployment news accelerates industrial procurement. However, the industrial nature of 5G demand may actually reduce volatility over time as consistent buying provides price support, potentially favoring outright long positions over volatility-dependent strategies.

Our comprehensive silver investing guide explores various investment approaches for capitalizing on structural demand trends like 5G deployment. Understanding these fundamental drivers helps investors position for long-term silver appreciation while managing short-term volatility.

Frequently Asked Questions

How much silver does a typical 5G base station require? A 5G macro base station contains approximately 20-30 grams of silver, primarily in antenna systems, power amplifiers, and high-frequency circuits. This represents 2-3 times more silver than 4G base stations due to higher frequencies and more complex antenna arrays required for 5G performance.

Can other metals substitute for silver in 5G applications? Silver's unique combination of electrical conductivity and thermal properties makes substitution extremely difficult in 5G applications. While copper costs less, its inferior conductivity at high frequencies degrades 5G signal quality. Gold offers comparable performance but costs significantly more, making silver the optimal choice for large-scale 5G deployment.

What happens to silver demand if 5G deployment slows? 5G deployment timelines are driven by competitive pressure between telecommunications carriers and government infrastructure initiatives, making significant slowdowns unlikely. However, even if deployment rates moderate, maintenance and device replacement cycles would sustain silver demand at elevated levels compared to pre-5G consumption.

How do COMEX inventory levels affect industrial silver buyers? Industrial silver users typically purchase through physical markets rather than COMEX futures, but inventory levels signal overall supply tightness. Low COMEX inventories often correlate with higher physical premiums and longer delivery times for industrial buyers, potentially increasing their procurement costs and accelerating buying ahead of anticipated shortages.

Which 5G equipment manufacturers use the most silver? Major telecommunications equipment manufacturers like Ericsson, Nokia, Samsung, and Huawei are the largest 5G-related silver consumers. However, their tier-2 suppliers—antenna manufacturers, PCB fabricators, and component suppliers—often purchase silver directly, making demand more distributed than concentrated among a few major companies.

Sources

- CFTC Commitments of Traders reports: https://www.cftc.gov/dea/futures/other_lf.htm

- CME Group COMEX inventory data: https://www.cmegroup.com/markets/metals.html

- Silver Institute supply and demand data: https://www.silverinstitute.org

- LBMA precious metals market data: https://www.lbma.org.uk/prices-and-data

- Federal Communications Commission 5G deployment statistics

- World Gold Council industrial demand analysis: https://www.gold.org/goldhub/data

Gold COT positioning: commercial hedgers (red) vs. speculators (green). Source: CFTC via SilverOfTruth, February 2026

Silver COT positioning: commercial hedgers (red) vs. speculators (blue). Source: CFTC via SilverOfTruth, February 2026

Conclusion

Silver's integral role in 5G technology creates a compelling structural demand story that intersects with concerning COMEX inventory dynamics to present both opportunity and risk for precious metals investors. With 5G deployment requiring 2-3 times more silver per base station than 4G infrastructure and global rollout plans calling for millions of new installations, telecommunications applications could drive silver consumption growth of 15-20% annually through 2028. This industrial demand surge occurs as COMEX registered inventory provides only 52.6% coverage against current open interest, creating potential supply stress if physical procurement accelerates.

The investment implications extend beyond simple supply-demand arithmetic. 5G represents durable, committed demand that provides price support during market downturns while amplifying upward moves during periods of investment inflows. Unlike speculative demand that can reverse rapidly, industrial 5G procurement follows multi-year infrastructure deployment schedules that create sustained buying pressure. Track how these dynamics unfold with our COMEX inventory tracker to monitor supply conditions as 5G demand accelerates.

For investors seeking exposure to this structural silver demand story, our comprehensive silver investing guide provides detailed strategies for capitalizing on industrial demand trends while managing the unique risks and opportunities that 5G technology creates for precious metals markets.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, investment, or trading advice. Past performance is not indicative of future results. Always conduct your own research and consult with a qualified financial advisor before making investment decisions. SilverOfTruth provides market data and analysis tools — it does not provide personalized financial advice.