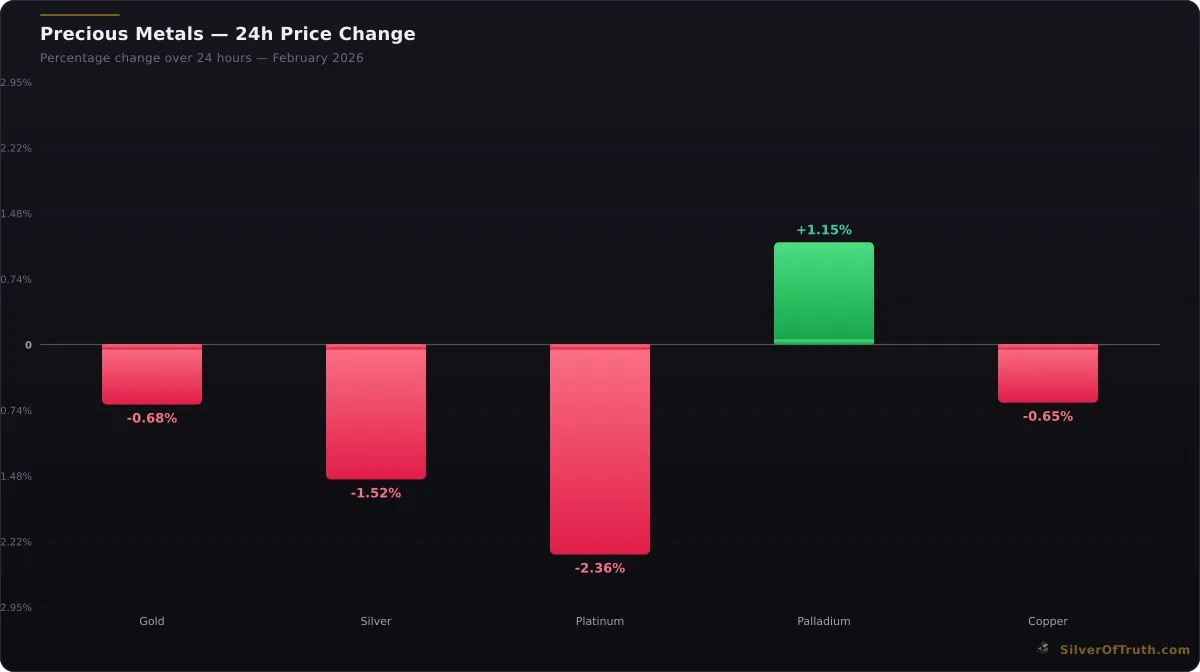

Real interest rates just delivered another blow to precious metals, with gold tumbling 0.68% to $5,012 and silver plunging 1.52% to $76.78. This marks a continuation of the pressure campaign that's been building as inflation expectations moderate while nominal rates hold elevated levels.

The mathematics are simple but brutal for metals investors. When real interest rates climb above zero, precious metals lose their competitive edge against yield-bearing assets. Today's decline reinforces this dynamic as markets digest the latest economic data and Federal Reserve positioning signals.

Understanding this relationship is crucial for precious metals investors navigating the current environment. The interplay between inflation expectations, nominal interest rates, and their combined impact on real yields drives much of the precious metals price action we're witnessing.

Current Real Interest Rate Environment

Real interest rates represent the difference between nominal interest rates and expected inflation. When this calculation turns positive, it creates opportunity cost for holding non-yielding assets like gold and silver.

The recent Federal Reserve's interest rate signals suggest policymakers remain committed to keeping rates elevated until inflation demonstrates sustained progress toward the 2% target. According to the latest FOMC minutes, several voting members expressed concern about premature easing that could reignite inflationary pressures.

This hawkish stance coincides with moderating inflation expectations. Treasury Inflation-Protected Securities (TIPS) spreads have compressed over recent weeks, suggesting market participants expect inflation to continue declining from current levels. The combination creates an increasingly positive real rate environment that penalizes precious metals holdings.

Current Treasury yields paint a clear picture of this dynamic. The 10-year Treasury note yields approximately 4.2%, while 10-year TIPS breakevens trade around 2.3%. This generates a real yield of roughly 1.9%, significantly above the zero threshold that typically supports precious metals demand.

Our analysis of rising real interest rates shows this environment creating sustained headwinds for gold and silver. The opportunity cost calculation favors assets that provide current income over those that rely solely on capital appreciation potential.

Precious Metals Performance Under Pressure

Today's declines reflect the growing weight of real interest rate pressures across the precious metals complex. Gold's 0.68% drop extends its recent weakness, while silver's 1.52% decline demonstrates the heightened sensitivity of the white metal to macroeconomic conditions.

The gold/silver ratio expanded to 65.28, up 0.86% for the day. This widening spread typically signals risk-off sentiment, as silver's industrial demand components make it more vulnerable to economic uncertainty than gold's monetary role.

Platinum suffered the steepest losses, falling 2.36% to $2,028. The automotive-linked metal faces dual pressures from both rising real rates and concerns about global economic growth. Palladium bucked the trend with a 1.15% gain to $1,723, supported by supply constraints that override macro headwinds.

The performance divergence illustrates how different precious metals respond to varying demand drivers. While monetary metals like gold and silver face direct pressure from rising real rates, industrial metals contend with additional supply-demand fundamentals that can either amplify or offset rate-driven weakness.

COMEX positioning data reveals the challenges facing precious metals bulls. Silver's coverage ratio stands at 0.56, indicating high delivery risk, yet prices continue declining as macro factors override supply tightness concerns. This disconnect between physical fundamentals and price action exemplifies the powerful influence of real interest rate dynamics.

Our comprehensive analysis of COMEX inventory shows how macro pressures can overwhelm even supportive physical market conditions in the near term.

Federal Reserve Policy Impact Analysis

The Federal Reserve's current policy stance represents a fundamental shift from the ultra-accommodative environment that supported precious metals during the pandemic era. Real interest rates spent nearly two years in deeply negative territory, providing powerful tailwinds for gold and silver investments.

Recent Fed communications signal policymakers' determination to maintain restrictive monetary conditions until inflation returns durably to the 2% target. This patience reflects lessons learned from the 1970s experience, when premature easing allowed inflation to resurge with devastating economic consequences.

The central bank's preferred inflation measure, core Personal Consumption Expenditures (PCE), remains above the target despite recent moderation. Fed officials express particular concern about services inflation, which has proven more persistent than goods price increases.

This cautious approach creates an extended period of elevated real interest rates. Unlike previous cycles where Fed pivots provided relief for precious metals, the current environment suggests higher rates for longer. The policy framework prioritizes inflation control over asset price support.

Financial markets have begun pricing this reality into precious metals valuations. The inflation pressures analysis we published earlier highlighted how changing inflation expectations combine with steady nominal rates to pressure metals prices.

The implications extend beyond current positioning. If the Fed succeeds in anchoring inflation expectations around 2% while maintaining policy rates near current levels, real yields could remain elevated for an extended period. This scenario would create persistent headwinds for precious metals investment demand.

Global Economic Context and Inflation Dynamics

The global economic landscape adds complexity to the real interest rate picture affecting precious metals. Central banks worldwide are grappling with similar inflation challenges, though at different stages of their respective tightening cycles.

The European Central Bank continues its battle against persistent inflation, with services prices proving particularly stubborn. Recent ECB communications suggest policymakers remain committed to additional tightening despite growing recession risks. This coordinated global approach to inflation fighting reinforces the high real rate environment.

China presents a different dynamic, with the People's Bank of China maintaining accommodative policies to support economic growth. However, Chinese gold demand patterns suggest domestic investors are increasingly focused on real assets as hedges against currency depreciation rather than pure inflation protection.

The Shanghai gold premium analysis reveals how regional monetary policies create arbitrage opportunities that can offset global real rate pressures in specific markets. Yet these localized effects rarely override broader global trends for extended periods.

Inflation expectations across developed markets have moderated from peak levels, contributing to the real rate increases pressuring precious metals. Market-based measures like 5-year, 5-year forward inflation expectations have declined as central bank credibility improves.

The commodity complex broadly reflects this shifting inflation landscape. Energy prices have stabilized after initial supply shock impacts, while food inflation has begun moderating as supply chain disruptions resolve. These developments support the case for sustained disinflation that could keep real rates elevated.

Industrial metals face additional pressure from China's economic slowdown and global manufacturing weakness. Copper's 0.65% decline today reflects these dual pressures of higher real rates and weakening demand fundamentals.

Market Positioning and Investor Sentiment

Commitment of Traders (COT) data reveals how rising real interest rates are reshaping precious metals positioning across different investor categories. Speculative long positions in gold have declined as the opportunity cost of holding non-yielding assets increases.

24-hour precious metals price changes. Source: SilverOfTruth, February 2026

According to the latest CFTC COT report, managed money positions in gold show net long exposure of 92,022 contracts, down modestly by 50 contracts from the previous week. However, the broader trend shows speculative interest waning as real yields rise.

Commercial hedgers maintain substantial short positions, with gold commercials holding net shorts of 197,738 contracts. This positioning reflects producer hedging activity as mining companies lock in favorable prices amid operational cost pressures. The commercial short position serves as a natural stabilizer but indicates limited near-term buying support.

Silver positioning shows greater balance, with speculators holding net long positions of 22,955 contracts. The smaller speculative commitment compared to gold suggests silver may face less pressure from position liquidation, though its higher volatility amplifies any selling pressure that does emerge.

Our detailed COT analysis explains how positioning data provides insight into market structure and potential price direction. The current setup shows vulnerable speculative positioning that could amplify downward pressure if real rates continue rising.

Exchange-traded fund (ETF) flows provide another lens into investor sentiment. Gold ETF holdings have experienced modest outflows as investors rotate toward yield-bearing alternatives. The GLD and IAU funds, which hold physical gold to back their shares, reflect this shift in investment preferences.

Silver ETFs show similar patterns, with the large SLV fund experiencing periodic redemptions. Our comparison of PSLV vs SLV highlights how different fund structures respond to changing market conditions and investor preferences.

Historical Context and Precedent Analysis

Historical analysis reveals clear patterns in how precious metals respond to rising real interest rate environments. The early 1980s provide the most instructive parallel, when Fed Chairman Paul Volcker's aggressive interest rate increases created deeply positive real yields.

During that period, gold prices declined from peak levels above $850 per ounce to below $300 as real interest rates soared above 5%. Silver experienced even steeper declines, falling from nearly $50 per ounce to single digits. The magnitude of these moves illustrates the power of real interest rate dynamics over precious metals.

The key difference between then and now lies in the starting point for both nominal rates and inflation. Current policy rates, while elevated by recent standards, remain below historical norms. Similarly, inflation levels, though concerning, haven't reached the double-digit peaks of the late 1970s.

This suggests the current real rate pressure on precious metals may be less severe than historical precedents, but the directional impact remains consistent. As our gold/silver ratio analysis shows, the relationship between the metals often reflects these broader macro pressures.

The 1990s provide another useful comparison period. During that decade, generally positive real interest rates coincided with extended precious metals weakness. Gold traded in a range between $300-$400 for most of the decade, while silver struggled below $10 per ounce.

However, that period also featured unique factors including central bank gold sales and the emergence of new financial instruments that provided alternatives to precious metals for portfolio diversification. The current environment differs significantly in terms of central bank behavior and financial market structure.

More recent history offers mixed signals. The 2013 "taper tantrum" demonstrated how quickly precious metals can decline when real rates rise unexpectedly. Gold fell nearly 30% that year as markets repriced Fed policy expectations. Yet the decline proved temporary as actual policy tightening proceeded more gradually than initially feared.

Supply and Demand Fundamental Analysis

Despite macro headwinds from rising real interest rates, precious metals supply and demand fundamentals present a complex picture that could influence the medium-term outlook. Physical market conditions often diverge from paper market pricing during periods of macro stress.

COMEX inventory data reveals ongoing tightness in deliverable supplies. Silver registered stocks have declined to 92.9 million ounces, supporting a coverage ratio of just 0.56 against open interest. This high-risk level typically indicates potential delivery stress, though macro pressures are currently overwhelming these supportive physical factors.

Our COMEX inventory analysis details how physical tightness can create upward price pressure once macro headwinds moderate. The current disconnect between physical fundamentals and pricing may resolve in favor of physical reality over time.

Gold inventory shows similar patterns, with registered stocks at 17.6 million ounces providing moderate coverage against 404,391 contracts of open interest. The 0.43 coverage ratio indicates medium risk levels that warrant monitoring but don't signal immediate delivery stress.

Mine supply continues facing challenges from rising production costs, environmental regulations, and permitting delays. According to data from the World Gold Council, global gold mine production has plateaued in recent years despite higher prices incentivizing expanded output.

Silver mine supply faces additional constraints from its byproduct nature. Approximately 70% of silver production comes as a byproduct of base metal mining, limiting the supply response to higher silver prices. The Silver Institute reports ongoing supply deficits that could support prices once macro pressures ease.

Industrial demand for silver remains robust despite economic headwinds. Solar panel installations continue driving significant silver consumption, while emerging technologies like 5G networks and electric vehicles add new demand sources. Our analysis of silver in 5G technology explores these evolving demand patterns.

Investment Strategy Implications

The current environment of rising real interest rates creates specific challenges for precious metals investors that require strategic adjustments to traditional approaches. Simple buy-and-hold strategies may underperform during extended periods of positive real yields.

Dollar-cost averaging remains a viable approach for long-term investors who view precious metals as portfolio insurance rather than speculative investments. This strategy helps smooth out volatility during macro-driven sell-offs while maintaining exposure to potential upside when conditions improve.

Tactical allocation adjustments may benefit from focusing on physical metals over financial derivatives during high real rate environments. Physical holdings avoid the carrying costs and margin requirements that amplify pressure on leveraged positions when markets move against precious metals.

The opportunity cost calculation suggests considering yield-bearing alternatives for portions of portfolios traditionally allocated to precious metals. Treasury Inflation-Protected Securities (TIPS) provide inflation protection with current income, potentially offering better risk-adjusted returns during high real rate periods.

Our guide on when to buy silver vs gold provides framework for making allocation decisions between different precious metals based on macroeconomic conditions and risk tolerance.

Mining stocks present both opportunities and risks in the current environment. While rising real rates pressure all equity valuations, well-positioned miners with low costs and strong balance sheets may outperform the underlying metals during transitional periods. Our comprehensive guide on how to evaluate mining stocks offers tools for identifying quality opportunities.

International diversification may provide some relief from domestic real rate pressures. Precious metals priced in currencies with lower real rates may outperform dollar-denominated holdings, though currency hedging costs could offset these benefits.

Frequently Asked Questions

What are real interest rates and why do they matter for precious metals?

Real interest rates equal nominal interest rates minus expected inflation. When real rates are positive, they create opportunity cost for holding non-yielding assets like gold and silver. Higher real rates make bonds and other income-producing investments more attractive relative to precious metals.

How long might rising real interest rates pressure precious metals?

The duration depends on Federal Reserve policy and inflation trends. If the Fed maintains current rates while inflation continues moderating, real rates could remain elevated for 12-18 months or longer. Historical precedents suggest precious metals can face extended pressure during such periods.

Should investors avoid precious metals entirely during high real rate environments?

Complete avoidance isn't necessary, but allocation adjustments may be prudent. Reducing precious metals exposure while maintaining some portfolio insurance makes sense. Focus on physical holdings over leveraged positions and consider dollar-cost averaging to manage timing risks.

Which precious metals perform better when real interest rates rise?

Gold typically shows more resilience than silver due to its monetary role. Silver's industrial demand and higher volatility can amplify declines. Platinum and palladium face additional supply-demand factors that can override macro influences in either direction.

How can investors track real interest rates effectively?

Monitor 10-year Treasury yields minus 10-year TIPS breakeven rates for a market-based real rate measure. Also watch Fed communications and inflation data releases. The SilverOfTruth app provides integrated macro analysis to help investors understand these relationships.

Conclusion

Rising real interest rates are delivering sustained pressure on precious metals, with today's declines in gold (-0.68%) and silver (-1.52%) reinforcing this macro-driven weakness. The combination of maintained Fed hawkishness and moderating inflation expectations creates an environment where non-yielding assets face persistent headwinds.

The mathematical reality is straightforward: when Treasury bonds offer real yields approaching 2%, precious metals must compete on appreciation potential alone. Historical analysis shows this challenge can persist for extended periods, suggesting investors should adjust expectations and strategies accordingly.

Yet physical market fundamentals remain supportive beneath the macro pressure. COMEX inventory tightness and ongoing supply constraints could reassert influence once real rate pressures moderate. The key lies in understanding when macro conditions might shift in favor of precious metals again.

For investors seeking comprehensive precious metals market intelligence, including real-time data on inventory levels, positioning changes, and macro factor analysis, the SilverOfTruth app provides the tools needed to navigate complex market conditions. Available on the App Store, it combines institutional-grade data with AI-powered analysis to help investors make informed decisions.

The precious metals story isn't over, but the current chapter is being written by real interest rate dynamics that deserve careful attention and strategic response.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, investment, or trading advice. Past performance is not indicative of future results. Always conduct your own research and consult with a qualified financial advisor before making investment decisions. SilverOfTruth provides market data and analysis tools. It does not provide personalized financial advice.