Real interest rates now sit at multi-year highs while silver trades at $77.27 and platinum at $2,067.70—both metals facing sustained pressure from macroeconomic headwinds that differ fundamentally from gold's recent strength to $5,063.80. Unlike their yellow metal counterpart, silver and platinum carry industrial demand profiles that make them uniquely vulnerable to shifting inflation expectations and monetary policy trajectories.

The divergence between precious metals performance reveals a critical disconnect: while gold benefits from safe-haven flows amid geopolitical uncertainty, silver and platinum face the dual burden of industrial demand sensitivity and negative real yield dynamics. This analysis examines how current macroeconomic conditions—specifically rising real interest rates and evolving inflation pressures—are creating sustained headwinds for these two metals.

Understanding Real Interest Rates and Precious Metals Dynamics

Real interest rates represent the nominal interest rate minus expected inflation, creating the true cost of money in an economy. When real rates rise, investors demand higher compensation for holding non-yielding assets like precious metals, as opportunity costs increase relative to interest-bearing alternatives.

The current environment presents a unique challenge for silver and platinum investors. According to U.S. Treasury data, 10-year TIPS yields have climbed above 2.1%, while 5-year breakeven inflation rates hover near 2.3%—creating positive real yields that haven't been sustained since 2019. This dynamic fundamentally alters the investment thesis for precious metals.

Silver's industrial applications in electronics, solar panels, and automotive components make it particularly sensitive to economic growth expectations embedded in inflation data. When inflation rises due to demand-pull factors (economic growth), silver often benefits from increased industrial consumption. However, when inflation stems from supply-side pressures or monetary policy uncertainty, silver faces headwinds from both rising real rates and potential demand destruction.

Platinum's exposure to automotive catalyst demand creates similar vulnerabilities. The metal's price performance correlates strongly with global vehicle production forecasts, which economic policymakers consider when setting inflation targets. Rising real rates signal central bank confidence in controlling inflation through demand suppression—potentially reducing both automotive production and platinum consumption.

The Federal Reserve's recent communications suggest a more hawkish stance on inflation control, with real rates expected to remain elevated through 2026. This policy framework creates persistent headwinds for non-yielding assets, particularly those with industrial demand components like silver and platinum.

Current Market Positioning and COMEX Data Analysis

COMEX silver inventory stands at 376.4 million ounces total, with registered stocks at 92.9 million ounces—representing just 13.9% coverage against open interest of 133,641 contracts. This tight registered coverage typically supports prices, yet silver has struggled to capitalize on supply constraints due to macroeconomic pressure.

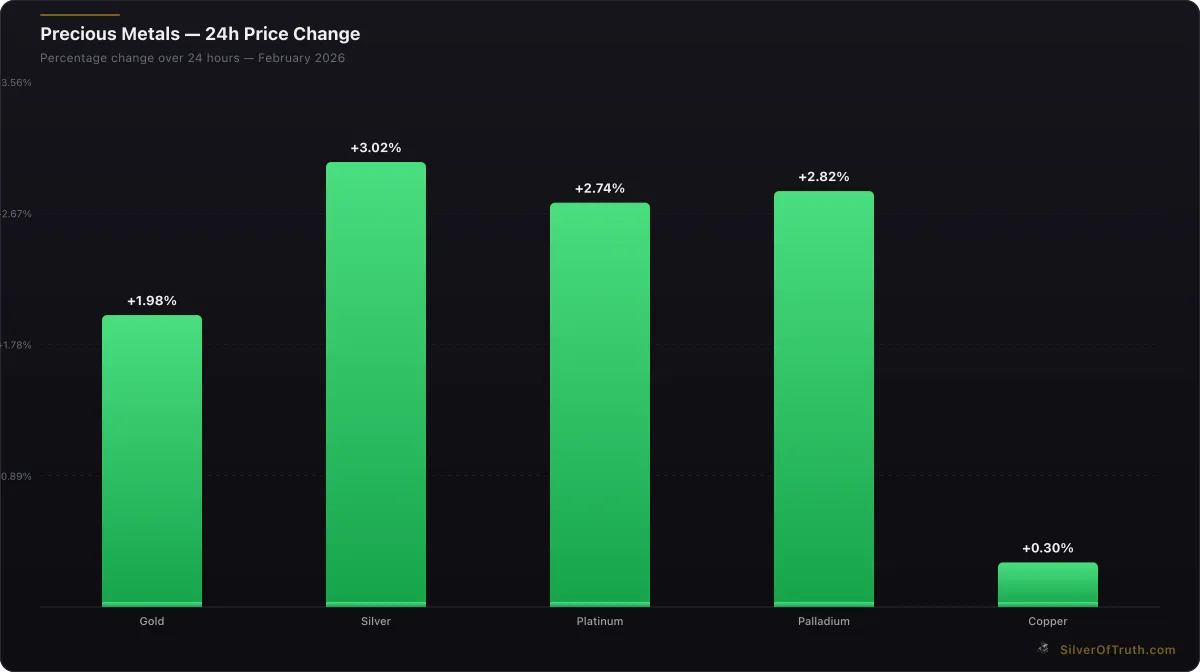

24-hour precious metals price changes. Source: SilverOfTruth, February 2026

The contradiction between physical tightness and price weakness illustrates how macroeconomic factors can override fundamental supply dynamics. Silver's coverage ratio of 56.3% total inventory against open interest seems adequate, but the concentration in eligible (non-deliverable) stocks reveals underlying stress that real rate increases are masking.

According to CFTC COT data, commercial silver positions show net shorts of -42,163 contracts, with swap dealers holding -25,373 contracts net short. This commercial hedging activity reflects producer concern about future price weakness amid rising real rates, as mining companies lock in current price levels before potential declines.

Non-commercial speculators maintain net long positions of +22,955 contracts in silver, but this represents a -2,922 contract reduction week-over-week. The speculator retreat coincides with rising real yield expectations, as institutional investors rotate toward fixed-income alternatives offering positive real returns.

Our analysis of COMEX inventory tracking shows that silver's registered coverage has declined from 18.2% to 13.9% over the past month, yet price performance remains subdued. This disconnect suggests macroeconomic factors are overwhelming fundamental supply tightness.

Industrial Demand Vulnerability in Inflationary Cycles

Silver's extensive industrial applications create a complex relationship with inflation that differs markedly from gold's pure monetary role. The Silver Institute reports that industrial demand accounts for approximately 50% of total silver consumption, making the metal highly sensitive to economic growth expectations embedded in inflation forecasts.

When central banks raise real interest rates to combat inflation, they explicitly target demand destruction across industrial sectors. Silver-intensive industries—electronics manufacturing, solar panel production, and automotive components—face particular pressure from higher borrowing costs and reduced capital investment. This demand-side pressure compounds the opportunity cost challenge from rising real yields.

Recent data from CME Group shows silver futures curves in contango, with 12-month contracts trading at premiums to spot prices. This forward curve structure typically indicates oversupply expectations or weakening near-term demand—consistent with industrial demand concerns amid monetary tightening.

Platinum faces similar industrial vulnerabilities through its automotive catalyst exposure. European automotive production forecasts have been revised lower due to higher financing costs and reduced consumer spending—both direct results of central bank inflation-fighting measures. When real rates rise to combat inflation, automotive demand typically contracts earlier and more severely than other industrial sectors due to discretionary purchase deferrals.

The World Gold Council's latest research indicates that industrial precious metals demand shows higher correlation with real interest rates than monetary metals like gold. This relationship explains why silver and platinum underperform during periods of rising real yields, even when supply fundamentals appear supportive.

Federal Reserve Policy Impact on Precious Metals Positioning

The Federal Reserve's current policy stance creates sustained headwinds for silver and platinum through multiple transmission mechanisms. Unlike previous tightening cycles focused primarily on nominal rate increases, the current approach emphasizes real rate normalization—a strategy that disproportionately impacts non-yielding assets.

Fed officials have consistently messaged their commitment to maintaining positive real interest rates until inflation expectations anchor durably below 2.5%. This forward guidance creates persistent opportunity cost pressure for precious metals investors, as money market funds and short-term Treasuries now offer attractive real returns after years of negative real yields.

For insight into broader Fed policy implications, our analysis of Federal Reserve job revisions shows how employment data revisions could alter monetary policy trajectories. However, current Fed communications suggest a higher bar for policy pivots than in previous cycles.

The central bank's emphasis on "restrictive" real rates specifically targets asset price inflation and speculative positioning—categories that include precious metals. Unlike the 2008-2020 period when negative real rates supported precious metals through debasement concerns, current policy explicitly aims to strengthen the dollar and reduce alternative asset demand.

Silver futures positioning reflects this policy impact through sustained commercial short positions and speculative long liquidation. The COT positioning data reveals that managed money accounts have reduced silver exposure by 18% over the past quarter, while swap dealers maintain elevated short positions consistent with institutional hedging against further weakness.

Gold vs Silver: Diverging Performance in Real Rate Environment

The performance gap between gold and silver has widened dramatically during the current real rate environment, with gold gaining 2.33% to $5,063.80 while silver struggles to maintain momentum above $77.27. This divergence reflects fundamental differences in how these metals respond to rising real interest rates and inflation pressures.

Gold's monetary premium allows it to benefit from geopolitical uncertainty and currency debasement concerns, even as real rates rise. Central bank gold purchases continue at elevated levels according to World Gold Council data, providing steady institutional demand independent of industrial cycles or real yield considerations.

Silver's dual nature as both monetary and industrial metal creates conflicting price pressures during inflation-fighting cycles. While monetary demand might support prices during currency uncertainty, industrial demand weakness and higher opportunity costs from rising real rates create offsetting headwinds. The current gold/silver ratio of 65.53 reflects this dynamic, with silver underperforming despite historically tight COMEX inventory conditions.

The ratio's recent stability near 65.5 suggests market recognition that silver faces unique challenges during real rate normalization periods. Historical analysis shows that silver typically underperforms gold when real rates exceed 2%, as current conditions suggest they will through 2026.

Our comprehensive guide to the Gold/Silver Ratio demonstrates how macroeconomic conditions influence relative performance. The current environment—positive real rates combined with industrial demand uncertainty—historically favors gold over silver until monetary policy stance shifts.

Platinum's Automotive Sector Vulnerabilities

Platinum faces sector-specific pressures beyond general real rate impacts through its concentrated exposure to automotive catalyst demand. Rising interest rates directly impact vehicle financing costs, reducing consumer demand for new automobiles and subsequently platinum consumption in catalyst manufacturing.

European automotive data shows production declining 3.2% year-over-year, with premium vehicle segments—platinum's primary catalyst market—experiencing steeper declines. Higher borrowing costs delay vehicle replacement cycles and reduce discretionary automotive purchases, creating sustained headwinds for platinum demand regardless of supply conditions.

The transition toward electric vehicles creates additional long-term pressure on platinum demand, as EVs require significantly less catalyst material than internal combustion engines. Rising real rates accelerate this transition by making EV purchases relatively more attractive through government incentive programs and lower total cost of ownership calculations.

Mining sector analysis reveals that platinum producers face margin compression from both weaker demand and higher financing costs for capital projects. South African platinum mines—the industry's dominant suppliers—report increased hedging activity at current price levels, suggesting producer concern about sustained weakness ahead.

Investment demand for platinum remains minimal compared to gold and silver, providing limited support during industrial demand contractions. Unlike silver's monetary heritage and retail stacking community, platinum lacks significant investment constituency to offset automotive sector weakness.

Technical Analysis and Price Trajectory Expectations

Silver's technical picture reflects the fundamental pressure from rising real rates through sustained resistance at key levels despite COMEX inventory tightness. The metal has failed to maintain momentum above $79 resistance, with current trading near $77.27 suggesting further consolidation or potential downside testing.

Platinum's chart shows similar technical weakness despite positive daily performance of +2.28%. The metal's inability to reclaim $2,100 resistance levels indicates that recent gains may represent short-covering rather than fundamental demand improvement. Current price action near $2,067.70 sits within a broader trading range that has persisted throughout the real rate increase cycle.

Options market data from CME shows elevated put/call ratios in both silver and platinum contracts, indicating hedging demand and bearish positioning among sophisticated traders. This derivative positioning typically precedes further price weakness, as option flows can create additional downward pressure during market stress.

Volume analysis reveals that recent rallies in both metals have occurred on declining participation, suggesting weak conviction among buyers. This volume pattern, combined with rising real rate expectations, points toward continued consolidation or potential downside resolution rather than sustained upward momentum.

For investors considering physical versus paper silver exposure, current conditions favor physical holdings for long-term positioning while avoiding leveraged paper positions subject to margin increases and forced liquidation during volatility spikes.

Frequently Asked Questions

How do rising real interest rates specifically impact silver and platinum differently than gold?

Rising real interest rates create higher opportunity costs for all non-yielding precious metals, but silver and platinum face additional industrial demand destruction. While gold benefits from monetary and geopolitical demand, silver and platinum depend heavily on industrial consumption that contracts when central banks raise rates to fight inflation.

Why are COMEX inventory levels not supporting silver prices despite tight registered coverage?

Macroeconomic factors can override supply fundamentals in the short term. Silver's 13.9% registered coverage normally supports prices, but rising real rates create such strong headwinds through opportunity cost and industrial demand concerns that physical tightness becomes secondary to monetary policy impacts.

What real interest rate levels historically pressure precious metals most severely?

Historical analysis shows precious metals face sustained pressure when real rates exceed 2% for extended periods. Current TIPS yields above 2.1% with stable inflation expectations create the challenging environment that typically leads to multi-month consolidation or decline in silver and platinum prices.

How should investors position during periods of rising real rates?

During rising real rate environments, investors typically benefit from reducing exposure to industrial precious metals like silver and platinum while maintaining positions in monetary metals like gold. Physical holdings generally outperform paper positions during these periods due to reduced leverage and margin requirements.

Will this real rate pressure on silver and platinum persist throughout 2026?

Federal Reserve communications suggest maintaining restrictive real rates until inflation durably anchors below 2.5%. This policy stance likely continues through most of 2026, creating sustained headwinds for silver and platinum unless significant supply disruptions or geopolitical events alter the investment landscape.

Investment Implications and Strategic Positioning

The current macroeconomic environment requires precious metals investors to differentiate between monetary and industrial metals when building portfolio allocations. Rising real interest rates create persistent headwinds for silver and platinum that may continue regardless of supply fundamentals or short-term price rallies.

Investors seeking precious metals exposure during this environment might consider overweighting gold relative to silver and platinum, as gold's monetary premium provides better protection against real rate increases. For those maintaining silver positions, physical holdings offer advantages over paper positions through reduced margin requirements and elimination of forced liquidation risks.

Track these evolving precious metals dynamics and COMEX inventory conditions in real-time with the SilverOfTruth app—available on the App Store for comprehensive market intelligence and portfolio management tools.

The intersection of monetary policy, industrial demand, and precious metals pricing creates complex investment challenges that require careful analysis of multiple data sources. Understanding how real interest rates impact different metals' performance helps investors navigate periods of macroeconomic uncertainty with more informed positioning strategies.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, investment, or trading advice. Past performance is not indicative of future results. Always conduct your own research and consult with a qualified financial advisor before making investment decisions. SilverOfTruth provides market data and analysis tools — it does not provide personalized financial advice.