Gold's 2.18% surge to $5,056.40 per ounce masks underlying vulnerabilities as Federal Reserve policy signals increasingly challenge the precious metal's traditional safe-haven status. While Wednesday's session produced impressive gains across the metals complex, deeper analysis reveals how shifting monetary policy expectations are fundamentally altering gold's risk-reward profile in ways that could persist through 2026.

The disconnect between current price action and evolving Fed policy creates a complex investment landscape where traditional precious metals drivers face unprecedented headwinds. Understanding these dynamics is crucial for investors navigating what our comprehensive Gold Investing 101 guide identifies as one of the most challenging monetary environments for precious metals in decades.

Quick Answer: Federal Reserve rate policy shifts are creating downward pressure on gold prices by increasing real yields and reducing the opportunity cost of holding non-yielding assets. Despite recent gains, gold faces structural headwinds as higher rates strengthen the dollar and diminish inflation hedging demand.

What Are Current Fed Policy Signals Telling Gold Investors?

The Federal Reserve's evolving stance on interest rates represents the most significant headwind facing gold prices since the 2022 hiking cycle began. Current market dynamics show gold trading at $5,056.40, up 2.18% in the latest session, yet this strength occurs against a backdrop of increasingly hawkish Fed positioning that threatens the metal's fundamental appeal.

Federal Reserve officials have consistently signaled their commitment to maintaining restrictive monetary policy until inflation convincingly returns to the 2% target. Recent Federal Open Market Committee minutes reveal growing concerns about persistent services inflation and wage growth, suggesting the central bank may need to keep rates higher for longer than previously anticipated.

The implications for gold are profound. As our analysis of gold as an inflation hedge demonstrates, the precious metal traditionally benefits from negative real interest rates—when nominal yields fall below inflation rates. However, the current environment increasingly features positive real yields, fundamentally altering gold's investment calculus.

Real yields, calculated as nominal Treasury yields minus inflation expectations, have turned decisively positive across multiple maturities. The 10-year Treasury Inflation-Protected Securities (TIPS) yield has moved from negative territory in early 2021 to positive levels above 2%, creating substantial opportunity costs for holding non-yielding gold.

This shift explains why gold prices face structural pressure despite geopolitical tensions and currency debasement fears that would typically support precious metals. The Fed's commitment to restrictive policy creates a challenging environment where gold must compete against yield-bearing alternatives offering attractive real returns.

How Do Rising Real Interest Rates Impact Gold's Investment Appeal?

Rising real interest rates represent gold's primary nemesis, fundamentally undermining the economic logic of holding non-yielding precious metals. Current market conditions exemplify this relationship, with positive real yields across the Treasury curve creating unprecedented opportunity costs for gold investors.

The mechanism is straightforward yet powerful. When Treasury bonds offer positive real returns—yields above inflation rates—rational investors demand compelling reasons to hold gold, which generates no income and incurs storage costs. This dynamic explains why gold struggled during the 1980s and 1990s when Paul Volcker's Fed maintained high real rates, and why the metal soared during the 2000s when real yields turned deeply negative.

Today's environment increasingly resembles the former period. With the Fed maintaining the federal funds rate in restrictive territory while inflation moderates, real yields have turned positive across multiple maturities. The Bureau of Labor Statistics Consumer Price Index shows inflation trending toward the Fed's 2% target, while nominal yields remain elevated, creating a widening gap that penalizes gold holdings.

Professional portfolio managers face particularly acute pressure to justify gold allocations when 10-year TIPS offer guaranteed real returns above 2%. This institutional selling pressure compounds retail investor hesitation, creating technical headwinds that reinforce the fundamental challenge posed by positive real yields.

The situation is further complicated by the dollar's strength. Higher U.S. real yields attract international capital, strengthening the dollar and making gold more expensive for foreign buyers—a double headwind that our precious metals converter tool helps investors track in real-time.

Historical analysis reveals that gold requires either negative real yields or significant crisis premiums to sustain bullish momentum. Current conditions provide neither, suggesting structural headwinds may persist until the Fed pivots toward easier policy.

What Role Does Dollar Strength Play in Gold's Current Weakness?

The U.S. dollar's strength, driven largely by Federal Reserve policy expectations, creates a powerful headwind for gold prices that extends beyond simple currency relationships. Higher U.S. interest rates not only increase the opportunity cost of holding gold but also strengthen the dollar through capital flows, creating a compounding effect that amplifies downward pressure on precious metals.

Dollar strength impacts gold through multiple channels. Direct currency effects make gold more expensive for international buyers, reducing demand from major consuming regions including Asia and Europe. The London Bullion Market Association data shows how sterling and euro-denominated gold prices often disconnect from dollar prices during periods of significant currency moves, reflecting this demand destruction.

More importantly, dollar strength reflects broader confidence in U.S. monetary policy and economic resilience. When foreign investors perceive the Federal Reserve as successfully managing inflation without triggering recession, they gravitate toward dollar-denominated assets offering attractive real yields. This capital flow strengthens the dollar while reducing demand for alternative stores of value like gold.

The current environment exemplifies this dynamic. Fed officials' success in bringing inflation down from 9% peaks to near-target levels without triggering severe recession has enhanced dollar credibility. International investors increasingly view U.S. assets as offering both safety and yield—a combination that historically proved challenging for gold.

Technical analysis supports this fundamental view. The Dollar Index (DXY) correlation with gold prices has turned increasingly negative, reaching levels not seen since the early 2000s. This suggests markets view dollar strength and gold weakness as mutually reinforcing trends rather than temporary dislocations.

The implications extend beyond price action. Strong dollar conditions historically persist until the Fed pivots toward easier policy, suggesting gold may face sustained headwinds until monetary policy shifts meaningfully toward accommodation.

How Are COMEX Positioning Dynamics Reflecting Fed Policy Concerns?

COMEX futures positioning data reveals how Fed policy expectations are reshaping professional trader sentiment toward gold, with significant implications for near-term price action. The latest Commitment of Traders (COT) data shows managed money positions unwinding from extreme bullish levels, reflecting growing recognition that higher-for-longer interest rates fundamentally challenge gold's investment thesis.

According to CFTC COT data as of February 3, 2026, speculative positioning shows clear signs of capitulation. Non-commercial traders (speculators) hold 214,508 long contracts versus 48,904 short positions, for a net long position of 165,604 contracts. However, the weekly change reveals massive liquidation, with long positions declining by 37,592 contracts while short positions increased by 2,200 contracts.

This positioning shift reflects institutional recognition that Fed policy creates structural headwinds for precious metals. The 78,769-contract decline in total open interest to 409,694 contracts signals broader disengagement from gold futures as traders reassess the risk-reward profile under higher real yield conditions.

Commercial hedgers provide additional insight into market dynamics. Their net short position of -207,778 contracts reflects continued producer hedging against potential price declines, while the modest weekly covering of 40,507 contracts suggests producers remain cautious about gold's prospects under current monetary conditions.

The concentration data reveals additional risks. Top four traders hold 34.2% of all short positions, compared to just 17.1% of long positions, suggesting potential for accelerated selling if positioning unwinds continue. Our COT dashboard tool tracks these concentration risks in real-time, providing crucial insights for positioning decisions.

Managed money funds, often considered the most sensitive to macro conditions, show particularly bearish positioning changes. Their net long position fell by 26,087 contracts to 92,072, reflecting institutional assessment that Fed policy creates unfavorable conditions for gold speculation.

What Does COMEX Inventory Data Reveal About Physical Demand?

COMEX inventory levels provide crucial insights into physical gold demand dynamics amid Fed policy uncertainty. Current data shows total COMEX gold inventory at 34.42 million ounces, with registered stocks at 17.58 million ounces representing metal available for immediate delivery against futures contracts.

The inventory dynamics reveal a market in balance rather than stress. Total inventory declined just 0.09% according to the latest data, suggesting neither aggressive accumulation nor desperate liquidation. This stability contrasts with the dramatic inventory swings seen during crisis periods, indicating that current Fed policy concerns haven't yet triggered panic physical buying.

More telling is the relationship between inventory and open interest. With 409,694 contracts representing 40.97 million ounces of potential delivery demand, the coverage ratio stands at 84%—a comfortable level that suggests no immediate delivery pressure. Our COMEX inventory tracker monitors these ratios continuously, providing real-time assessment of potential squeeze risks.

The registered versus eligible breakdown offers additional insights. Registered inventory at 17.58 million ounces represents metal immediately available for delivery, while eligible stocks provide a buffer of stored metal that could convert to registered status if needed. The current balance suggests adequate supply to meet potential delivery demands without stress.

However, the inventory data also reveals limited physical buying interest. Unlike previous periods when Fed policy uncertainty drove aggressive vault accumulation, current levels suggest professional traders aren't viewing physical gold as particularly compelling under higher real yield conditions.

This dynamic reflects a fundamental shift in how market participants view gold's role during periods of monetary policy tightening. Whereas past episodes often triggered flight-to-quality physical buying, current conditions see traders increasingly focused on yield-bearing alternatives.

Why Isn't Geopolitical Uncertainty Supporting Gold Prices?

Traditional geopolitical risk premiums appear notably absent from current gold pricing, highlighting how Federal Reserve policy expectations now dominate precious metals markets more than classic safe-haven demand drivers. This represents a significant shift from historical patterns where international tensions reliably supported gold prices regardless of monetary policy conditions.

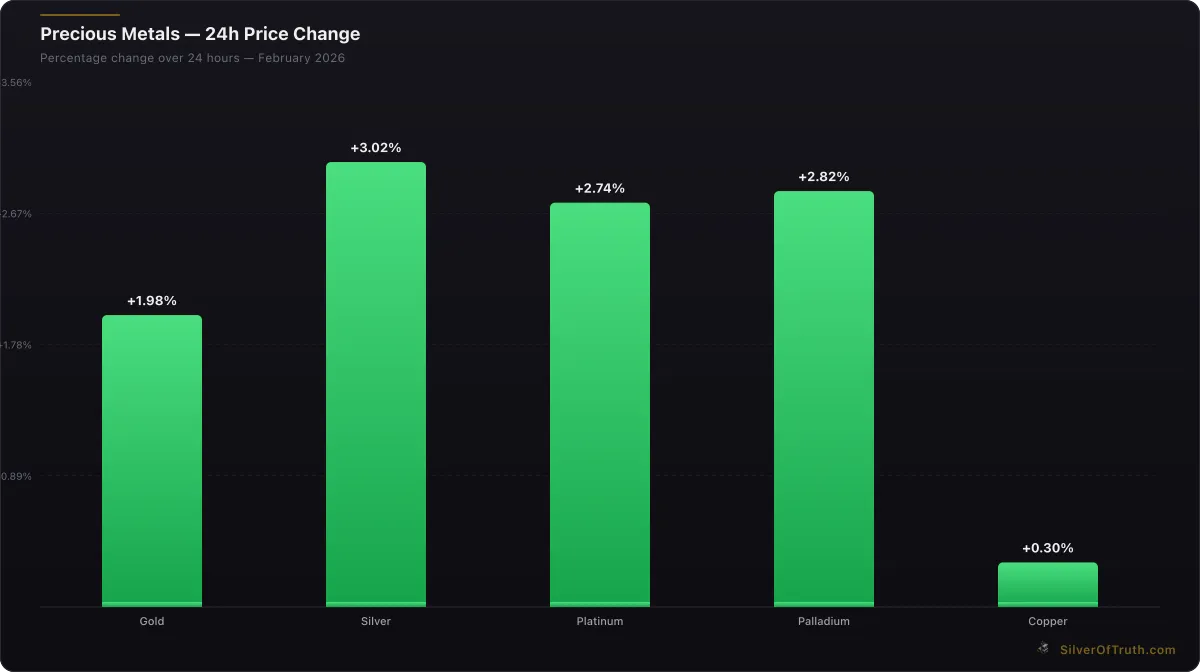

24-hour precious metals price changes. Source: SilverOfTruth, February 2026

Several factors explain this phenomenon. First, the magnitude of real yield changes has overwhelmed traditional risk premiums. When Treasury bonds offer real returns above 2%, geopolitical insurance premiums must compete against guaranteed positive real yields—a challenging comparison that historically favors bonds over gold.

Second, the nature of current geopolitical risks differs from traditional gold-supportive scenarios. Cold War tensions or currency crises that previously drove gold buying often involved questions about the dollar's stability or U.S. policy credibility. Current tensions, while significant, occur alongside demonstrated Fed policy effectiveness and dollar strength, reducing gold's appeal as a dollar alternative.

Market structure changes also play a role. Modern portfolio management increasingly relies on diversified strategies that can provide geopolitical hedging through multiple assets rather than concentrating risk in gold. Currency hedging, inflation-protected securities, and commodity exposure offer alternatives that didn't exist during gold's heyday as the primary crisis hedge.

Professional money managers face institutional pressures that further complicate gold allocations during geopolitical stress. Explaining gold underperformance becomes difficult when clients observe Treasury bonds providing both safety and yield during uncertain periods. This dynamic creates selling pressure even when geopolitical logic might support gold buying.

The implications suggest that geopolitical premiums may not return to gold until Fed policy creates conditions where traditional safe-haven assets offer negative or minimal real returns. Until then, gold must compete on pure investment merit against attractive alternatives.

How Should Investors Position for Continued Fed Policy Impacts?

Navigating gold investments under continued Federal Reserve policy pressure requires recognizing that traditional precious metals strategies may prove inadequate in higher real yield environments. Successful positioning must account for structural changes in how gold competes against alternative assets while maintaining exposure to potential policy pivot opportunities.

Strategic considerations begin with timeline expectations. Fed policy cycles typically persist longer than market participants initially expect, suggesting current headwinds could continue through 2026 and beyond. Investors betting on rapid Fed pivots may face extended periods of opportunity cost as gold underperforms yield-bearing alternatives.

Portfolio allocation approaches should reflect these realities. Rather than traditional gold allocations based on inflation hedging or crisis insurance, investors might consider tactical approaches that recognize gold's sensitivity to real yield changes. This suggests smaller core positions supplemented by tactical additions during periods when Fed policy signals shift toward accommodation.

Technical analysis provides additional guidance. Gold's correlation with real yields has strengthened significantly, suggesting investors can monitor 10-year TIPS yields as leading indicators for precious metals performance. Rising real yields typically pressure gold, while declining real yields provide tailwinds.

Currency hedging becomes particularly relevant for international investors. Dollar strength driven by Fed policy creates dual headwinds through both higher real yields and currency appreciation. European or Asian investors might consider currency-hedged gold exposure to isolate precious metals performance from dollar movements.

Mining equity strategies may offer superior risk-adjusted returns during higher real yield periods. Quality gold producers with strong balance sheets and low production costs can potentially outperform physical gold when margins remain healthy despite price pressure. Our mining stock screener helps identify candidates with favorable cost profiles.

What Economic Indicators Should Gold Investors Monitor?

Federal Reserve policy evolution depends on key economic indicators that gold investors must track to anticipate potential monetary policy shifts. Understanding these data points provides crucial insights into when current headwinds might ease and traditional gold-supportive conditions might return.

Inflation metrics remain paramount. The Consumer Price Index and core PCE deflator drive Fed policy decisions more than any other indicators. Sustained inflation declines toward the 2% target support continued restrictive policy, while inflation resurging above target could force even more hawkish positions. Gold investors should monitor not just headline numbers but underlying components, particularly services inflation that has proven most persistent.

Employment data provides equally important signals. The Bureau of Labor Statistics employment reports influence Fed policy through both employment mandate considerations and wage inflation concerns. Softening labor markets typically presage Fed policy pivots, while continued strength supports higher-for-longer positioning.

Treasury yield curves offer real-time policy expectation updates. The relationship between 2-year and 10-year yields reflects market expectations for Fed policy paths, while TIPS breakevens provide inflation expectation insights. Yield curve inversions or steepening provide leading indicators for potential policy shifts that could benefit gold.

Financial conditions indices synthesize multiple indicators into single measures that Fed officials monitor closely. The Goldman Sachs Financial Conditions Index and Chicago Fed National Financial Conditions Index provide weekly updates on whether financial conditions are tightening or easing, influencing Fed policy flexibility.

International indicators also matter as Fed policy increasingly considers global spillover effects. European Central Bank policy divergence, China growth indicators, and emerging market currency stress can all influence Fed decision-making and create conditions where gold regains safe-haven appeal.

Our inflation calculator tool helps investors track real return calculations that drive gold's fundamental attractiveness, while the live gold price tracker provides real-time monitoring of how these indicators translate into precious metals performance.

What Are the Long-Term Implications for Gold Investment Strategy?

The current Federal Reserve policy regime suggests fundamental changes in gold's investment profile that may persist well beyond the immediate cycle. These structural shifts require investors to reconsider traditional precious metals strategies and develop approaches suited to potentially prolonged higher real yield environments.

Historical analysis reveals that gold performance closely correlates with real interest rate regimes rather than short-term policy moves. The 1980s and 1990s saw sustained gold weakness during periods of positive real yields, while the 2000s produced spectacular gains when real yields turned negative. Current conditions increasingly resemble the former period, suggesting structural rather than cyclical headwinds.

Demographic and institutional changes compound these challenges. Modern portfolio management emphasizes risk-adjusted returns and diversification strategies that reduce reliance on single assets like gold for portfolio protection. Inflation-protected securities, commodity funds, and currency hedging provide alternatives that didn't exist during gold's historical prominence.

Central bank policy coordination also creates new dynamics. Unlike previous eras when Fed policy diverged significantly from other major central banks, current conditions feature more synchronized tightening cycles. This reduces currency volatility and crisis premiums that traditionally supported gold during monetary policy uncertainty.

However, long-term factors continue supporting gold's role in diversified portfolios. Fiscal sustainability concerns, currency debasement risks, and geopolitical fragmentation create potential scenarios where traditional safe-haven demand could resurface powerfully. The key is recognizing that such scenarios may require more extreme conditions than historically necessary.

Investment implications suggest tactical rather than strategic approaches may prove most effective. Rather than large permanent allocations, investors might consider smaller core positions supplemented by opportunistic additions during periods when real yield conditions turn favorable or crisis premiums emerge.

The evolution continues highlighting precious metals' role as portfolio insurance rather than investment growth drivers. This perspective aligns gold allocations with traditional insurance principles—paying premiums for protection against low-probability, high-impact scenarios rather than expecting consistent positive returns.

For comprehensive precious metals education and strategies adapted to modern market conditions, explore our Gold Investing 101 hub, which provides detailed analysis of how monetary policy shapes precious metals performance across different economic cycles.

Sources

- Federal Reserve FOMC Meeting Minutes and Statements: https://www.federalreserve.gov/monetarypolicy/fomccalendars.htm

- Bureau of Labor Statistics Consumer Price Index Reports: https://www.bls.gov/cpi/

- CFTC Commitments of Traders Reports: https://www.cftc.gov/dea/futures/other_lf.htm

- London Bullion Market Association Price Data: https://www.lbma.org.uk/prices-and-data

- U.S. Treasury TIPS Market Data: https://www.treasurydirect.gov/marketable-securities/tips/

- Bureau of Labor Statistics Employment Situation Reports: https://www.bls.gov/news.release/empsit.toc.htm

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, investment, or trading advice. Past performance is not indicative of future results. Always conduct your own research and consult with a qualified financial advisor before making investment decisions. SilverOfTruth provides market data and analysis tools — it does not provide personalized financial advice.