Can COMEX actually default on precious metals contracts? With silver's registered coverage ratio currently at 13.9% and gold at 43.5%, this question has moved from precious metals forums to mainstream financial discourse. While conspiracy theories abound, the reality of COMEX default risk requires careful examination of exchange mechanics, regulatory safeguards, and historical precedent.

This analysis separates legitimate structural concerns from unfounded speculation, examining the actual mechanisms that could lead to settlement failure and the extensive safeguards designed to prevent it. Understanding COMEX default risk isn't about predicting market collapse—it's about comprehending how the world's largest precious metals futures exchange manages systemic risk in an increasingly complex global market.

What Constitutes COMEX Default Risk

COMEX default risk encompasses several distinct but related scenarios that could disrupt normal contract settlement. Unlike corporate bankruptcy, exchange default involves the inability to fulfill contractual obligations to deliver physical metal against futures contracts at expiration.

Source: SilverOfTruth COMEX data, February 2026

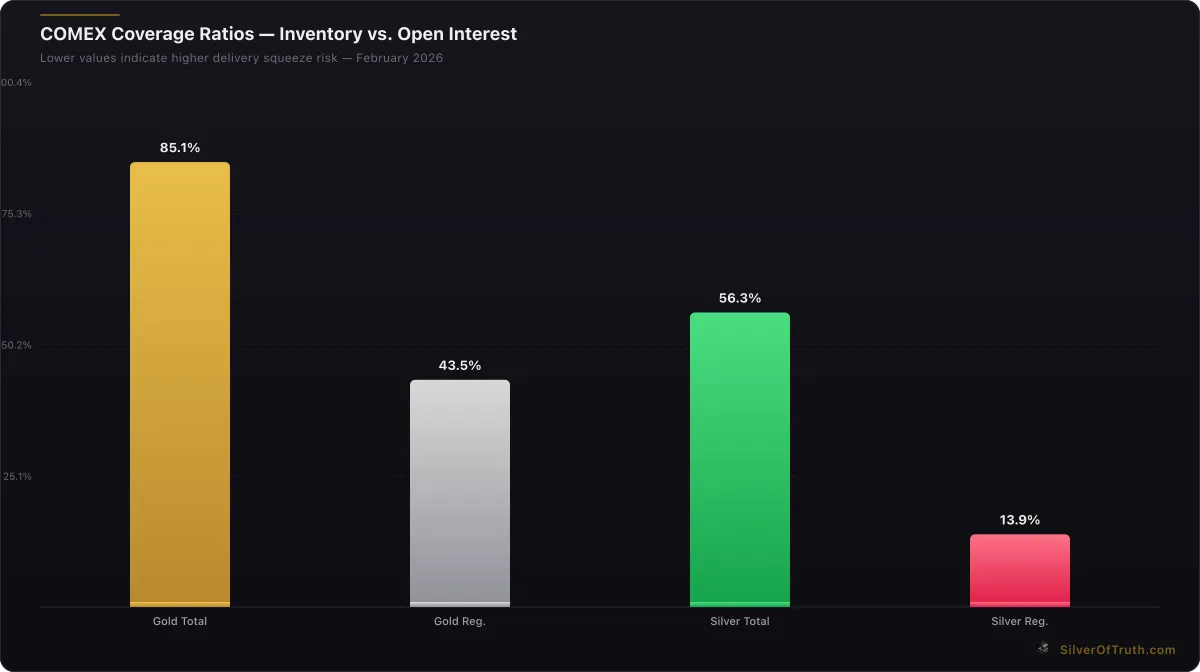

COMEX coverage ratios — lower values indicate higher delivery squeeze risk. Source: SilverOfTruth, February 2026

The most commonly discussed scenario involves physical delivery failure, where insufficient registered inventory exists to satisfy delivery demands. As of February 2026, COMEX silver registered inventory stands at 92.9 million ounces against open interest representing 668.2 million ounces—a coverage ratio of just 13.9%. While not all contracts demand delivery, this ratio indicates potential stress points during heightened physical demand periods.

Cash settlement imposition represents another risk scenario where COMEX might force cash settlement instead of physical delivery due to supply constraints. Though futures contracts legally require physical delivery upon demand, exchange rules contain provisions for emergency cash settlement under extreme circumstances. Such action would fundamentally alter market dynamics and likely trigger significant price disruption.

Clearing member failure poses systemic risk through the interconnected nature of exchange operations. Major clearing members like JPMorgan Chase or Goldman Sachs facilitate most COMEX transactions. Their financial distress could cascade through settlement systems, particularly during volatile periods when margin calls and delivery demands spike simultaneously.

According to the CFTC's risk management guidelines, exchanges must maintain adequate financial resources to complete settlement even if their largest clearing member defaults. However, multiple simultaneous failures could exceed these safeguards, creating systemic settlement risk across all COMEX metals.

Historical Precedents and Near-Miss Events

COMEX has never experienced complete default in its 154-year history, but several episodes illustrate system stress points and adaptive mechanisms. The March 1980 silver crisis remains the closest historical parallel to current inventory concerns, when silver prices spiked from $6 to $50 per ounce in four months.

During this period, COMEX registered inventory fell to approximately 40 million ounces while open interest exceeded 200,000 contracts (1 billion ounces). The exchange responded by implementing liquidation-only trading on January 21, 1980, preventing new long positions while allowing shorts to cover. This unprecedented action effectively capped silver's rise and prevented potential delivery squeeze, though it sparked lawsuits alleging market manipulation.

The 2008 financial crisis tested COMEX's risk management systems without causing default. Despite massive volatility and credit stress affecting major clearing members, the exchange maintained normal operations through enhanced margin requirements and regulatory coordination. Gold and silver inventories actually increased during this period as investors sought physical safe havens.

More recently, the March 2020 COVID-19 market disruption created brief settlement concerns when transportation restrictions complicated delivery logistics. COMEX temporarily modified delivery specifications to include additional vault locations and extended delivery windows. While controversial among physical metals advocates, these adaptations prevented settlement failure during extraordinary circumstances.

Learn more about these mechanisms in our complete guide to how COMEX delivery works, which details the exchange's adaptive responses during crisis periods.

Current Risk Assessment Framework

Evaluating present-day COMEX default risk requires systematic analysis across multiple risk vectors. Coverage ratios provide the primary metric, measuring registered inventory against open interest. Current ratios of 13.9% for silver and 43.5% for gold represent different risk profiles requiring separate assessment.

Silver's extremely low coverage ratio indicates elevated structural risk. Historical analysis shows coverage below 20% correlates with increased delivery activity and potential supply stress. However, the majority of futures contracts—typically 95-98%—settle financially rather than through physical delivery, suggesting current inventory might accommodate realistic delivery demand.

Delivery flow analysis offers additional insight into actual physical demand patterns. February 2026 month-to-date delivery data shows balanced activity with issues matching stops, indicating orderly settlement without acute stress signals. Dramatic increases in delivery notices or stopped contracts would signal growing physical demand potentially exceeding registered supply.

Concentration risk metrics reveal vulnerability to large-position holders demanding delivery. According to CFTC concentration data, the top four traders control 33.7% of silver short positions and 20.2% of long positions. Coordinated delivery demands from major longs could quickly exceed available registered inventory, particularly if combined with reduced commercial short covering.

Our analysis of delivery squeeze risks provides detailed methodology for assessing these concentration effects and their potential impact on settlement capacity.

Exchange Risk Management Mechanisms

COMEX employs multiple layers of risk management designed to prevent default scenarios while maintaining market function. Daily marking-to-market ensures all positions reflect current prices with variation margin collected immediately, reducing counterparty risk compared to forward contracts or over-the-counter arrangements.

Progressive margin increases represent the first line of defense against delivery squeeze scenarios. As volatility or open interest increases, COMEX raises initial and maintenance margin requirements, naturally reducing speculative positioning while preserving legitimate hedging activity. During extreme periods, margins can increase 300-500% from baseline levels.

Position limits and accountability levels prevent excessive concentration that could facilitate market manipulation or overwhelm physical supply. Large traders must report positions exceeding specified thresholds and may face restrictions on further accumulation. Federal position limits, implemented under Dodd-Frank regulations, provide additional concentration controls.

Emergency powers grant COMEX broad authority during crisis situations. These include suspension of trading, modification of contract specifications, and imposition of liquidation-only periods. While controversial, such measures prevent systemic breakdown during extreme stress. The exchange can also coordinate with the CME Group's broader risk management framework to ensure adequate financial resources.

Clearing and Settlement Safeguards

The Central Counterparty (CCP) model places CME Clearing between all trades, eliminating direct counterparty risk between market participants. CME Clearing becomes the buyer to every seller and seller to every buyer, backed by robust financial resources including clearing member guaranty funds and CME Group's own capital.

Waterfall default procedures ensure continuity even if major clearing members fail. Initial margin covers normal price movements, while clearing member guaranty funds provide additional resources. If these prove insufficient, CME Clearing can assess remaining clearing members or utilize its own capital reserves. Final backstop includes voluntary cash settlement authority under extreme circumstances.

Regulatory oversight from the CFTC provides additional safeguards through ongoing supervision, risk monitoring, and enforcement authority. The Commission conducts regular examinations of exchange risk management systems and can mandate corrective action if deficiencies emerge. Coordination with banking regulators ensures clearing member financial stability remains adequate for settlement obligations.

Physical delivery infrastructure maintains capacity for actual metal transfer when demanded. COMEX-approved depositories include major vault facilities operated by Brink's, Delaware Depository, and JPMorgan Chase. While inventory levels fluctuate, total storage capacity exceeds current registered holdings by substantial margins, allowing for inventory rebuilding if supply conditions improve.

Understanding these safeguards requires examining the difference between registered and eligible inventory, as only registered metal can fulfill delivery obligations while eligible inventory provides potential supply buffer.

Regulatory Framework and Government Backstops

Federal regulation creates multiple layers of protection against COMEX default scenarios. The Commodity Exchange Act grants the CFTC broad authority to ensure market integrity and prevent manipulation that could trigger artificial shortages. This includes emergency powers to suspend trading, modify position limits, or mandate cash settlement during crisis periods.

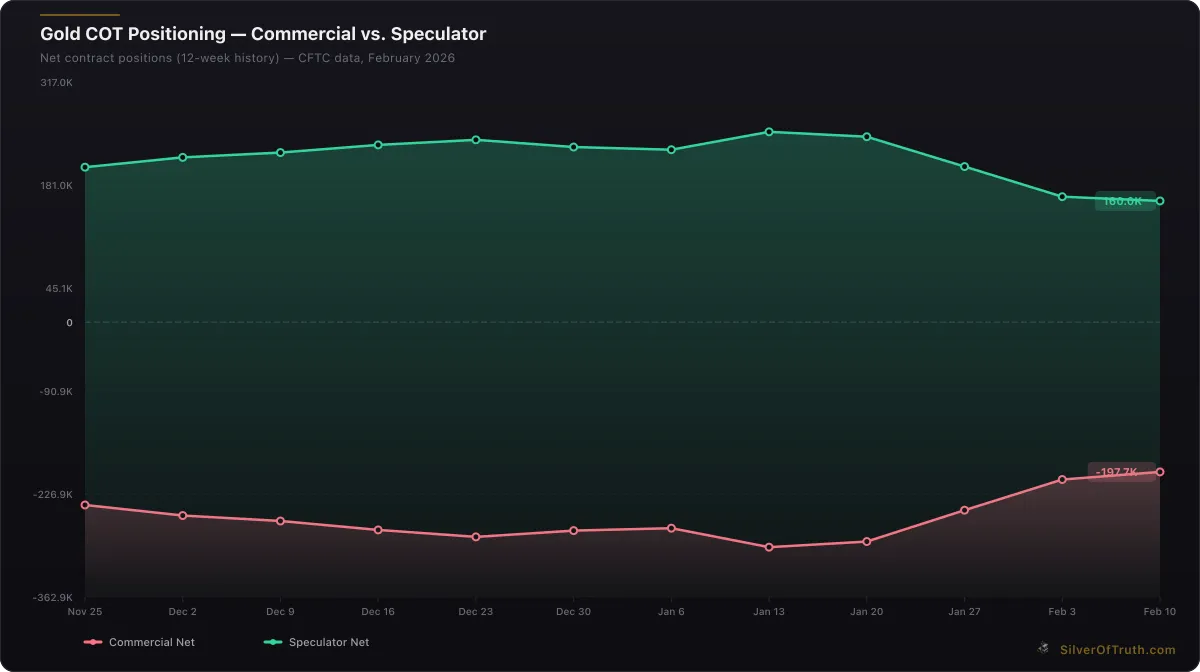

Gold COT positioning: commercial hedgers (red) vs. speculators (green). Source: CFTC via SilverOfTruth, February 2026

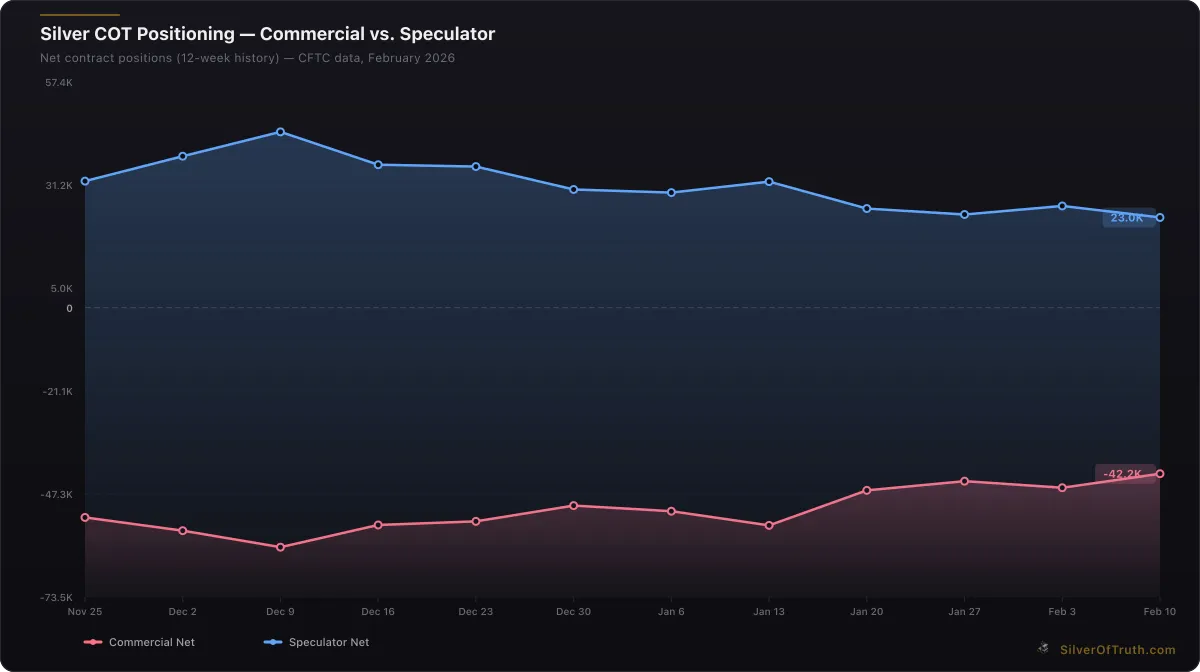

Silver COT positioning: commercial hedgers (red) vs. speculators (blue). Source: CFTC via SilverOfTruth, February 2026

Systemically Important Financial Market Utilities (SIFMU) designation provides additional regulatory oversight and potential government support. While COMEX itself hasn't received SIFMU status, CME Clearing's designation ensures heightened supervision and access to Federal Reserve liquidity facilities if needed during extreme stress.

Bank partnership arrangements connect COMEX operations to traditional banking safeguards. Major clearing members are typically large banks subject to Federal Reserve supervision, creating additional stability through diversified revenue sources and regulatory capital requirements. Their participation ensures COMEX maintains connection to broader financial system resources.

Strategic Petroleum Reserve precedent illustrates government willingness to intervene in commodity markets during supply emergencies. While no equivalent exists for precious metals, federal gold reserves at Fort Knox and West Point provide potential intervention capacity if COMEX default threatened broader financial stability.

International coordination through organizations like the Financial Stability Board and International Organization of Securities Commissions creates frameworks for cross-border assistance during global financial stress. Given precious metals' role as monetary assets, international cooperation could provide additional backstops beyond domestic regulatory resources.

Potential Default Scenarios and Consequences

Gradual inventory depletion represents the most probable stress scenario rather than sudden default. Continued physical demand exceeding mine production and scrap recycling could slowly drain COMEX registered inventories over months or years. Such depletion would likely trigger graduated exchange responses including higher margins, position limits, and delivery specification modifications before reaching actual default.

Simultaneous delivery demands during contract expiration periods could overwhelm available registered inventory despite adequate coverage ratios. If multiple large position holders simultaneously demand delivery—whether for legitimate business needs or market manipulation—registered supply could prove insufficient even with financial settlement preferences among most participants.

Force majeure events affecting delivery infrastructure could create settlement failures despite adequate inventory levels. Transportation strikes, natural disasters affecting approved depositories, or cyber attacks on clearing systems could prevent physical delivery even when metal remains available. Recent experience with COVID-19 logistics disruptions illustrates such vulnerabilities.

Consequences of actual default would likely include immediate trading suspension, forced cash settlement of outstanding contracts, and significant price volatility as markets adjust to altered supply dynamics. Legal challenges from affected parties would create prolonged uncertainty, while regulatory investigations could result in structural market changes affecting future operations.

The "paper to physical" price convergence theory suggests default would cause spot physical prices to decouple dramatically from futures, potentially trading at substantial premiums to cash-settled contract values. However, this assumes limited alternative physical markets, ignoring substantial over-the-counter trading, London Bullion Market Association operations, and other global platforms detailed in our COMEX vs LBMA comparison.

Probability Assessment Based on Current Data

Objective risk assessment requires careful evaluation of current data against historical patterns and regulatory safeguards. Silver presents elevated but manageable risk given its 13.9% registered coverage ratio and concentrated positioning. While this level historically correlates with increased stress, robust risk management systems and regulatory oversight provide substantial buffers against actual default.

Gold shows lower immediate risk with 43.5% registered coverage providing adequate cushion for normal delivery demand. The current COT positioning shows speculator reduction and commercial covering, reducing concentration pressure that could overwhelm physical supply. Month-to-date delivery activity remains balanced without stress indicators.

Probability estimation suggests actual COMEX default remains low-probability but higher than historical norms due to structural inventory changes and concentrated positioning. Conservative assessment places default probability at 2-5% over the next 12 months for silver, versus less than 1% for gold, compared to historical baselines near zero.

Risk factors increasing probability include further inventory depletion, growing delivery demand from large position holders, or external shocks affecting clearing member stability. Conversely, factors reducing risk include regulatory intervention capability, exchange emergency powers, and alternative market mechanisms providing pressure relief valves.

Market pricing appears to incorporate modest default risk premium, particularly in silver, where physical premiums over futures remain elevated compared to historical norms. This suggests sophisticated market participants recognize structural changes while maintaining confidence in system stability overall.

Alternative Market Mechanisms and Spillover Effects

London Bullion Market Association (LBMA) operations provide crucial alternative to COMEX futures for large-scale precious metals trading. Daily LBMA clearing volumes often exceed COMEX, creating natural arbitrage mechanisms that could absorb demand if COMEX encountered settlement difficulties. However, LBMA focuses on wholesale transactions rather than standardized futures contracts, limiting direct substitution.

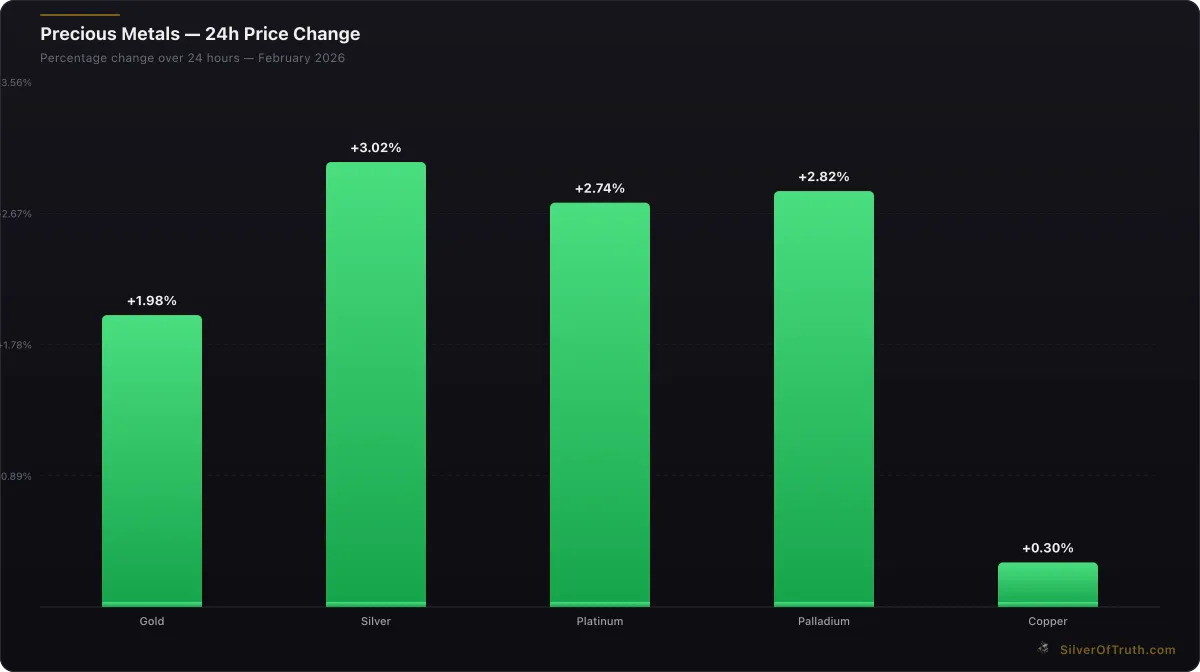

24-hour precious metals price changes. Source: SilverOfTruth, February 2026

Exchange-traded funds (ETFs) like SPDR Gold Trust (GLD) and iShares Silver Trust (SLV) hold substantial physical inventories backing their shares. Combined ETF holdings often exceed COMEX registered inventories, providing alternative exposure mechanisms for investors seeking precious metals allocation. ETF redemption mechanisms could theoretically provide additional physical supply during COMEX stress, though practical and regulatory constraints limit this channel.

Over-the-counter markets facilitate substantial precious metals trading outside exchange systems. Major banks and bullion dealers maintain inventory and trading relationships supporting large transactions without exchange intermediation. These markets could expand rapidly if COMEX encountered difficulties, though potentially at wider bid-ask spreads and with different credit risk profiles.

Regional exchanges including Shanghai Gold Exchange offer additional trading venues, particularly for Asian market participants. While contract specifications and delivery mechanisms differ from COMEX, these platforms provide partial substitutes that could limit global supply disruption if COMEX experienced settlement problems.

Long-Term Structural Changes and Trends

Mine production constraints create underlying physical supply pressures affecting all precious metals markets. Silver mine production has declined approximately 15% since 2016 while industrial demand continues growing, creating structural deficits that strain exchange inventory systems regardless of financial market dynamics.

Central bank purchasing patterns show sustained demand for gold reserves, with 2023 marking record annual purchases according to World Gold Council data. This institutional demand competes with exchange inventory accumulation, potentially constraining supplies available for futures market backing over time.

Regulatory evolution continues adapting to modern market structures and risk profiles. Proposed changes to position limits, delivery specifications, and clearing requirements could alter default risk calculations while potentially creating new vulnerabilities during transition periods.

Technology integration affects both risk management capabilities and potential failure modes. Enhanced monitoring and automated risk controls reduce operational risk while creating new cyber security vulnerabilities that could disrupt settlement systems even with adequate physical inventories.

Geopolitical factors increasingly influence precious metals markets as monetary policies diverge and trade relationships evolve. Sanctions, export restrictions, or currency crises could affect international delivery networks supporting COMEX operations, creating supply chain risks beyond traditional financial considerations.

Understanding these trends requires monitoring both supply fundamentals and positioning dynamics, as covered in our comprehensive COMEX inventory analysis.

Investment Implications and Risk Mitigation

Portfolio diversification across different precious metals exposure methods reduces COMEX-specific risk while maintaining overall precious metals allocation. Combining futures positions with physical holdings, ETF shares, and mining equity provides multiple paths to precious metals returns while avoiding concentration in single settlement mechanisms.

Physical allocation considerations become more important during periods of elevated COMEX risk. Direct physical ownership through allocated storage or personal possession eliminates counterparty risk but introduces storage, insurance, and liquidity considerations. The optimal balance depends on individual risk tolerance and investment objectives.

Timing and positioning strategies can help navigate periods of elevated default risk. Monitoring coverage ratios, delivery flows, and COT positioning provides early warning indicators for potential stress periods. Reducing futures exposure during low coverage ratio periods while maintaining physical allocation could optimize risk-adjusted returns.

Alternative venue utilization diversifies settlement risk across multiple market mechanisms. Using LBMA-backed ETFs alongside COMEX futures, or trading London forward markets instead of New York futures, reduces dependence on single exchange systems while maintaining precious metals exposure.

For beginning investors, our guide on how to start silver stacking with $100 provides practical approaches to physical precious metals ownership that sidestep exchange-related risks entirely.

Monitoring and Early Warning Systems

Real-time inventory tracking provides crucial visibility into COMEX supply conditions. Daily warehouse reports show registered and eligible inventory changes, while monthly trends reveal longer-term depletion or accumulation patterns. Sudden inventory drops or persistent depletion warrant increased attention to default risk development.

Coverage ratio analysis offers standardized metrics for comparing current conditions to historical stress periods. Ratios below 20% for silver or 40% for gold historically correlate with increased delivery activity and potential supply stress, though actual default requires additional risk factors alignment.

Delivery monitoring reveals actual physical demand patterns beyond open interest statistics. Sharp increases in delivery notices, stopped contracts, or delivery delays signal growing physical demand that could strain available supply. Month-to-date tracking provides early indication of developing stress before contract expiration.

COT positioning surveillance identifies concentration risk from large speculative positions that could demand delivery. Unusual positioning patterns, particularly large long accumulation combined with commercial short covering, may indicate preparations for delivery squeeze attempts requiring enhanced monitoring.

The SilverOfTruth app provides comprehensive COMEX monitoring tools combining inventory tracking, coverage ratio analysis, and COT positioning data in real-time dashboards designed specifically for precious metals investors concerned about settlement risk.

FAQ

What would happen to my COMEX futures contracts if the exchange defaulted? In a true default scenario, outstanding contracts would likely be closed out through emergency cash settlement procedures at prevailing market prices. However, extensive regulatory safeguards and exchange emergency powers make actual default extremely unlikely. More probable scenarios involve temporary trading suspensions, modified delivery specifications, or enhanced margin requirements designed to prevent default while maintaining market function.

How does COMEX default risk compare to other commodity exchanges? COMEX generally maintains stronger risk management systems and deeper financial resources than smaller commodity exchanges due to its parent CME Group's size and regulatory oversight. However, precious metals' unique characteristics as monetary assets and store of value create different risk profiles compared to agricultural or energy commodities. Physical supply constraints and concentrated positioning can create stress patterns uncommon in other commodity markets.

Would COMEX default cause gold and silver prices to skyrocket? Default would likely cause significant short-term volatility and potential price spikes as markets adjust to altered settlement mechanisms. However, alternative trading venues including LBMA, ETFs, and over-the-counter markets would continue operating, potentially limiting sustained price disruption. Long-term price effects would depend primarily on underlying supply-demand fundamentals rather than settlement mechanism changes.

Can individual investors protect themselves from COMEX default risk? Diversification across multiple precious metals exposure methods provides the best protection. Combining futures positions with physical holdings, ETF shares, and mining stocks reduces dependence on any single settlement mechanism while maintaining precious metals allocation. Direct physical ownership eliminates counterparty risk entirely but introduces storage and liquidity considerations requiring careful evaluation.

Has any major commodity exchange ever actually defaulted? While no major modern commodity exchange has experienced complete default, several have implemented emergency measures during extreme stress. The London Metal Exchange's nickel trading suspension in March 2022 and COMEX's 1980 silver liquidation-only order demonstrate how exchanges use emergency powers to prevent default rather than allowing system breakdown. These precedents suggest regulatory authorities prioritize market stability over strict contract enforcement during crisis periods.

Track COMEX inventory levels, coverage ratios, and delivery flows in real-time with the SilverOfTruth app — available on the App Store.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, investment, or trading advice. Past performance is not indicative of future results. Always conduct your own research and consult with a qualified financial advisor before making investment decisions. SilverOfTruth provides market data and analysis tools — it does not provide personalized financial advice.