What began as a modest commodities exchange in New York's financial district has evolved into the world's most influential precious metals marketplace. The history of COMEX spans nearly a century of innovation, crisis, and transformation that shaped how gold and silver are traded globally today.

Understanding COMEX exchange history provides crucial context for modern precious metals investors. From the chaotic open outcry pits of the 1970s to today's sophisticated electronic trading systems handling over $100 billion in annual precious metals contracts, COMEX's evolution mirrors the broader transformation of global financial markets.

This comprehensive guide explores COMEX's origins, pivotal moments, technological revolutions, and current role as the price discovery mechanism for precious metals worldwide. Whether you're tracking COMEX inventory data or analyzing delivery patterns, understanding this exchange's history illuminates why its operations matter so much to modern markets.

The Birth of COMEX: Depression-Era Origins (1933-1939)

The COMEX origin story begins during the Great Depression when commodity trading faced unprecedented challenges. Founded in 1933 as the Commodity Exchange Inc., COMEX emerged from the merger of four smaller New York exchanges: the National Metal Exchange, the Rubber Exchange of New York, the National Raw Silk Exchange, and the Hide and Leather Exchange.

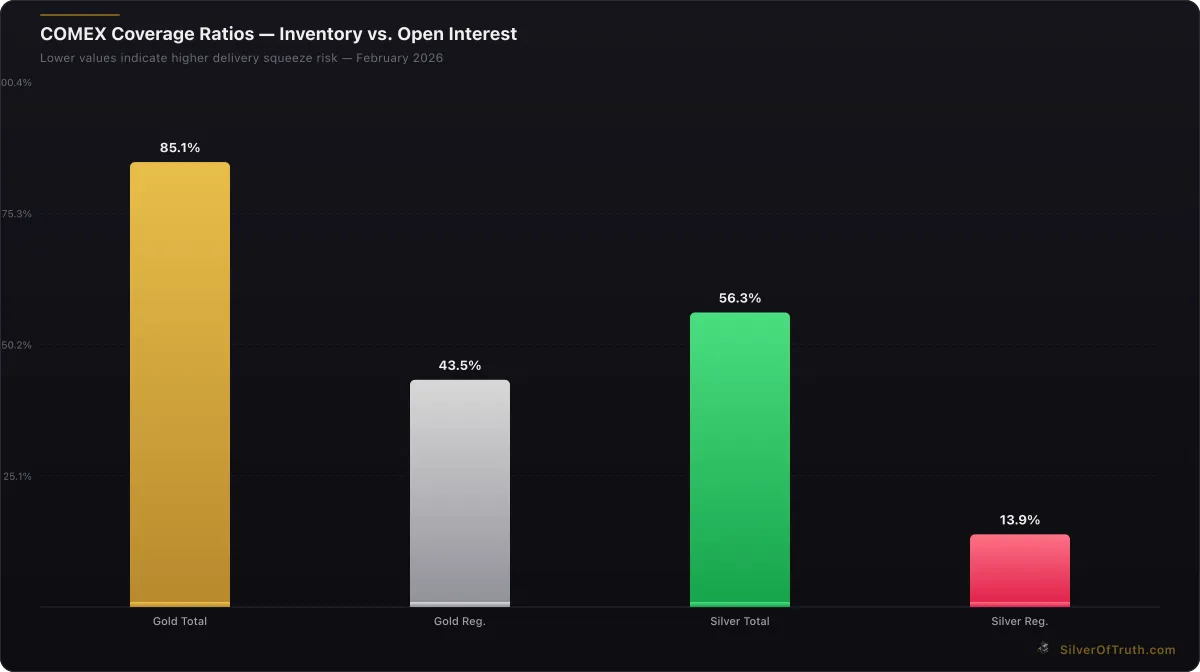

COMEX coverage ratios — lower values indicate higher delivery squeeze risk. Source: SilverOfTruth, February 2026

This consolidation reflected the economic realities of the 1930s. Individual exchanges struggled with declining volumes as global trade contracted by over 30% during the Depression. The merger created economies of scale and concentrated liquidity, essential for survival during the economic crisis.

Early Trading Operations

COMEX's initial operations differed dramatically from today's electronic systems. Floor traders used hand signals and verbal communication in dedicated trading pits. The exchange primarily focused on industrial metals including copper, tin, and zinc, with precious metals playing a secondary role.

The regulatory environment of the 1930s heavily constrained gold trading. President Franklin D. Roosevelt's Executive Order 6102 in 1933 prohibited private gold ownership by U.S. citizens, effectively limiting COMEX gold contracts to commercial and international participants. Silver faced fewer restrictions, establishing COMEX's early reputation in silver futures.

Trading hours were limited to morning sessions, typically 10 AM to 2 PM, reflecting the slower pace of 1930s commerce. Daily volumes rarely exceeded 1,000 contracts across all commodities, microscopic compared to today's hundreds of thousands of daily precious metals contracts.

The War Years and Post-War Expansion (1940-1970)

World War II fundamentally altered COMEX operations as government demand for strategic metals soared. The exchange became crucial for pricing copper, aluminum, and other materials essential to wartime production. Trading volumes increased dramatically, with daily activity rising from hundreds to thousands of contracts.

The Bretton Woods Agreement of 1944 established fixed exchange rates tied to gold at $35 per ounce, creating stability but limiting price discovery. COMEX gold futures remained relatively inactive during this period as the fixed price system reduced hedging needs and speculative interest.

Post-War Infrastructure Development

The 1950s and 1960s witnessed significant infrastructure improvements. COMEX moved to larger facilities at 4 World Trade Center in 1977, but the foundation was laid during the post-war expansion. The exchange invested in better communication systems, standardized contract specifications, and improved clearing mechanisms.

Silver markets began gaining prominence during this period as industrial demand increased. The rise of photography, electronics, and aerospace applications created new hedging needs among manufacturers. COMEX silver futures volume grew from negligible levels in the 1940s to several thousand contracts daily by the late 1960s.

The exchange also established its first international connections during this era. European metal traders began using COMEX contracts for price discovery and risk management, laying the groundwork for COMEX's eventual global dominance in precious metals.

The Golden Age: Open Outcry and the Hunt Brothers (1971-1985)

The collapse of Bretton Woods in 1971 marked COMEX's transformation into a major precious metals exchange. President Nixon's decision to end dollar-gold convertibility unleashed market forces that had been suppressed for decades. Gold and silver prices became free-floating, creating enormous hedging and speculative opportunities.

The Open Outcry Era Flourishes

COMEX's trading floors during the 1970s epitomized financial market chaos and energy. Hundreds of floor traders packed into octagonal trading pits, using elaborate hand signals and shouting matches to execute trades. The cacophony was legendary—visitors needed ear protection in the precious metals pits during active trading.

Gold futures volume exploded from virtually nothing in 1970 to over 100,000 contracts daily by 1980. Silver followed a similar trajectory, establishing COMEX as the world's primary precious metals price discovery venue. The exchange's influence grew so substantial that London Metal Exchange and other global bourses began referencing COMEX prices.

Trading technology remained primitive by modern standards. Floor traders relied on paper order tickets, hand-written position sheets, and telephone communications with off-floor customers. Settlement required physical delivery of certificates and manual reconciliation of trades—a process that often took days to complete.

The Hunt Brothers Silver Corner (1979-1980)

The most dramatic episode in COMEX exchange history occurred when Texas oil heirs Nelson Bunker Hunt and William Herbert Hunt attempted to corner the global silver market. Working with Saudi partners, the Hunt brothers accumulated over 100 million ounces of physical silver and massive COMEX futures positions.

Silver prices skyrocketed from $6 per ounce in early 1979 to over $50 by January 1980. COMEX trading volumes reached unprecedented levels as speculators and commercial users scrambled to manage exposure. Daily silver futures volume exceeded 50,000 contracts, straining the exchange's operational capacity.

COMEX responded by implementing emergency measures including position limits, increased margin requirements, and eventually "liquidation only" trading that prevented new long positions. The exchange's actions, while controversial, demonstrated its regulatory authority and market stabilization capabilities.

The Hunt brothers' empire collapsed in March 1980 when silver prices plummeted from $50 to under $10 within weeks. The crisis nearly bankrupted several major brokerage firms and highlighted the systemic risks of concentrated speculation. However, COMEX emerged with enhanced credibility as a well-regulated exchange capable of managing extreme market stress.

Technological Revolution and NYMEX Merger (1986-2008)

The 1980s brought the beginning of COMEX's technological transformation. Electronic order routing systems replaced some manual processes, though floor trading remained dominant. The exchange introduced computerized position monitoring and automated margining systems that improved risk management and operational efficiency.

Electronic Trading Emergence

COMEX launched its first electronic trading system in 1993, though adoption remained limited as floor traders resisted change. The system operated during extended hours when pits were closed, capturing increasing international demand from Asian and European participants. Electronic volume grew slowly but steadily throughout the 1990s.

The technological shift accelerated after the September 11, 2001 attacks. COMEX's World Trade Center location suffered significant damage, forcing temporary relocation and highlighting the vulnerability of floor-based operations. The exchange expedited its transition to electronic systems as a business continuity measure.

The NYMEX Merger (1994)

COMEX's most significant structural change occurred in 1994 when it merged with the New York Mercantile Exchange (NYMEX). This combination created the world's largest physical commodity futures exchange, combining COMEX's metals expertise with NYMEX's energy trading dominance.

The merger brought substantial benefits including shared technology costs, expanded product offerings, and greater capital resources. COMEX metals contracts gained access to NYMEX's growing international customer base, while energy traders could hedge related metals exposure through integrated positions.

Cross-margining between energy and metals products became possible, reducing capital requirements for diversified commodity traders. The combined exchange also achieved greater political influence in Washington, successfully advocating for favorable regulatory treatment of commodity futures.

However, the merger also marked the beginning of COMEX's identity evolution from an independent metals exchange to a division within a larger commodities complex. Some longtime COMEX members worried about diluted focus on precious metals, though trading volumes continued growing throughout the 1990s.

The Modern Era: Digital Dominance and Global Reach (2008-Present)

The 2008 financial crisis accelerated COMEX's final transformation from floor-based to electronic trading. As precious metals prices surged amid banking system instability, trading volumes reached record levels that overwhelmed remaining floor operations. By 2012, over 95% of COMEX precious metals trading occurred electronically.

CME Group Acquisition and Integration

CME Group's acquisition of NYMEX (including COMEX) in 2008 represented another pivotal moment in COMEX history. The $8.9 billion transaction integrated COMEX into the world's largest derivatives marketplace, providing access to advanced technology platforms and global distribution networks.

The integration brought immediate benefits including 24-hour electronic trading, improved liquidity through cross-margining, and enhanced risk management systems. COMEX precious metals contracts became accessible through CME's Globex platform, expanding international participation significantly.

Current COMEX operations bear little resemblance to the exchange's open outcry origins. Trading occurs continuously across global time zones, with peak activity during Asian and European business hours when New York markets are closed. Daily volume regularly exceeds 300,000 gold contracts and 100,000 silver contracts, representing over $30 billion in notional value.

Warehouse and Delivery System Evolution

COMEX's physical delivery infrastructure evolved dramatically to support increased trading volumes and international participation. The exchange's approved depository network expanded from a handful of New York area warehouses to global facilities in Chicago, Los Angeles, and other major cities.

Modern COMEX warehouses utilize sophisticated inventory management systems that track individual bars through electronic databases. Daily warehouse reports provide real-time transparency into registered versus eligible inventory levels, enabling precise analysis of delivery squeeze risks.

As of February 2026, COMEX gold inventory stands at 34.42 million ounces with registered stocks at 17.58 million ounces, according to CME Group warehouse data. Silver inventory totals 376.43 million ounces with 92.90 million registered. These levels represent the culmination of decades of infrastructure development supporting the world's largest precious metals trading complex.

COMEX's Impact on Global Precious Metals Markets

Today's COMEX serves as the global price discovery mechanism for gold and silver, with futures prices referenced by dealers, miners, central banks, and investors worldwide. The exchange's influence extends far beyond U.S. borders through electronic access and international arbitrage relationships.

Price Discovery and Reference Rates

COMEX futures prices serve as the primary reference for spot gold and silver quotes globally. London Bullion Market Association (LBMA) prices, Shanghai Gold Exchange premiums, and retail dealer markups all reference COMEX as the underlying benchmark according to LBMA pricing data.

The exchange's continuous trading model provides real-time price discovery 23 hours per day, with only a one-hour break for system maintenance. This near-continuous operation ensures that precious metals prices reflect global news flow, central bank policies, and supply-demand developments immediately.

Regulatory Framework and Market Integrity

COMEX operates under Commodity Futures Trading Commission (CFTC) oversight, providing regulatory transparency through weekly Commitments of Traders reports. These COT reports reveal positioning by commercial hedgers, large speculators, and small traders, offering unique insight into market sentiment and potential price movements.

The exchange maintains strict position limits, margin requirements, and surveillance systems designed to prevent market manipulation. While controversial episodes like the Hunt Brothers silver corner highlighted regulatory challenges, COMEX's current oversight framework reflects decades of refinement and strengthening.

Key Milestones in COMEX Development

| Year | Milestone | Impact | |------|-----------|---------| | 1933 | COMEX founded through merger | Consolidated NY commodity exchanges | | 1971 | Gold price decontrolled | Enabled precious metals futures growth | | 1979-80 | Hunt Brothers silver corner | Demonstrated exchange crisis management | | 1994 | NYMEX merger | Created world's largest commodity exchange | | 2001 | Post-9/11 electronic transition | Accelerated technology adoption | | 2008 | CME Group acquisition | Integrated into global derivatives leader | | 2012 | Floor trading ends | Completed electronic transformation |

The Warehouse System: Physical Foundation of Paper Markets

COMEX's physical delivery system remains crucial despite electronic trading dominance. The exchange's approved depositories provide the link between paper futures and physical metal markets, ensuring contract integrity and enabling arbitrage opportunities.

Source: SilverOfTruth COMEX data, February 2026

Depository Network Structure

Current COMEX depositories include major facilities operated by Delaware Depository Service Company, HSBC Bank USA, JPMorgan Chase Bank, and other approved institutions. These warehouses maintain segregated storage for eligible and registered metal, with daily reporting requirements to ensure transparency.

Eligible inventory consists of metal that meets COMEX specifications but isn't currently warrant-backed for delivery. Registered metal has associated warehouse receipts that can satisfy futures contract obligations. The distinction impacts delivery dynamics and coverage ratio calculations that indicate potential squeeze risks.

Delivery Process and Settlement

COMEX delivery involves transferring warehouse receipts rather than physical metal movement in most cases. Contract holders receiving delivery obtain warrants representing specific bars stored in approved facilities. This system enables efficient settlement while maintaining physical market connections.

The delivery process typically peaks during contract expiration months, with June and December historically showing the highest activity. Recent delivery patterns indicate growing physical demand, with some months seeing delivery rates exceeding 20% of open interest—well above historical averages of 2-3%.

COMEX in the Digital Age: Technology and Innovation

Modern COMEX operations rely on sophisticated technology infrastructure that would be unrecognizable to floor traders from the open outcry era. The exchange processes millions of price quotes and trade messages daily while maintaining microsecond response times for electronic order matching.

Globex Platform Integration

CME's Globex electronic trading platform handles all COMEX precious metals trading with order matching algorithms that prioritize price-time priority. The system supports complex order types including stop-losses, market-on-close, and spread strategies that were impossible during floor trading.

Globex connectivity extends to over 150 countries through internet-based access and dedicated telecommunications lines. This global reach enables 24-hour trading participation from major financial centers in Asia, Europe, and the Americas, creating truly international markets.

Data and Analytics Revolution

COMEX generates enormous amounts of market data including real-time prices, volume statistics, and open interest levels. This information feeds into analysis tools that track positioning trends, delivery patterns, and inventory dynamics with unprecedented detail.

Modern precious metals investors can access COMEX inventory tracking, COT analysis, and delivery monitoring that provides insights unavailable during the exchange's first 70 years. Applications like SilverOfTruth consolidate this data into user-friendly interfaces for retail and institutional investors.

Challenges and Criticisms in COMEX History

Despite its success, COMEX has faced recurring criticisms regarding market manipulation, concentrated positions, and the relationship between paper and physical markets. These challenges reflect broader debates about financialization's impact on commodity markets.

Manipulation Allegations and Enforcement

The Hunt Brothers episode established a pattern of manipulation allegations that continue today. Critics argue that large financial institutions use concentrated short positions to suppress precious metals prices, while COMEX defends its surveillance and position limit systems.

Recent CFTC enforcement actions against JPMorgan Chase and other major banks for spoofing precious metals futures highlighted ongoing manipulation concerns. However, these cases also demonstrated regulatory oversight effectiveness and the exchange's cooperation with enforcement efforts.

Paper vs Physical Market Dynamics

The ratio of COMEX open interest to available physical inventory generates ongoing controversy. Critics argue that excessive paper leverage artificially suppresses prices and creates systemic risks if delivery demands exceed warehouse supplies.

Current silver open interest of 668.2 million ounces exceeds total COMEX inventory of 376.4 million ounces, creating a coverage ratio of 56.3% that indicates potential delivery stress. However, historically similar ratios haven't prevented normal market functioning due to contract rolling and cash settlement options.

The Future of COMEX: Trends and Developments

COMEX continues evolving to meet changing market needs including increased retail participation, ESG considerations, and competition from alternative trading venues. The exchange's next chapter will likely feature further technological innovation and expanded global integration.

Retail Access and Democratization

Electronic trading and reduced transaction costs have democratized precious metals futures access for retail investors. Online brokers now offer COMEX futures alongside stocks and bonds, expanding the exchange's customer base beyond traditional commercial and institutional participants.

Micro contracts for gold and silver, launched in recent years, enable smaller position sizes suitable for individual investors. These products lower barriers to entry while maintaining exposure to COMEX price discovery and settlement mechanisms.

Environmental and Social Considerations

Growing ESG awareness impacts COMEX through responsible sourcing requirements and sustainability metrics. The exchange collaborates with industry initiatives promoting ethical mining practices and supply chain transparency.

Future developments may include carbon footprint tracking for delivered metal and preferential treatment for certified sustainable production. These changes would align COMEX with broader financial industry ESG trends while maintaining market integrity.

Frequently Asked Questions

What does COMEX stand for and when was it founded?

COMEX stands for Commodity Exchange Inc., founded in 1933 through the merger of four New York commodity exchanges during the Great Depression. The exchange was created to consolidate trading and improve liquidity during challenging economic conditions.

When did COMEX stop floor trading and go fully electronic?

COMEX gradually transitioned from open outcry floor trading to electronic systems between 1993-2012. While electronic trading began in 1993, floor operations continued until 2012 when the exchange completed its transition to the CME Globex electronic platform.

How did the Hunt Brothers affect COMEX silver trading?

The Hunt Brothers attempted to corner the silver market in 1979-1980, driving prices from $6 to over $50 per ounce. COMEX responded with emergency measures including position limits and liquidation-only trading, demonstrating the exchange's regulatory authority and crisis management capabilities.

What is the relationship between COMEX and CME Group?

CME Group acquired COMEX's parent company NYMEX in 2008 for $8.9 billion. COMEX now operates as a division of CME Group, the world's largest derivatives marketplace, providing access to global trading platforms and enhanced technology infrastructure.

How does COMEX inventory relate to futures contract delivery?

COMEX maintains approved depositories storing eligible and registered precious metals. Registered inventory can satisfy futures contract deliveries, while eligible metal meets specifications but lacks delivery warrants. The ratio of open interest to registered inventory indicates potential delivery squeeze risks.

Conclusion: COMEX's Enduring Legacy

From its Depression-era origins to today's electronic global marketplace, COMEX history represents the evolution of modern commodity trading. The exchange's transformation from chaotic open outcry pits to sophisticated digital systems mirrors broader changes in financial markets over nearly a century.

Understanding this history provides crucial context for analyzing current precious metals markets. Whether tracking COT positioning trends or monitoring delivery patterns, COMEX's past illuminates the forces shaping today's gold and silver prices.

As precious metals continue playing vital roles in investment portfolios and global monetary systems, COMEX's influence will likely grow. The exchange's ability to adapt—from surviving the Hunt Brothers crisis to embracing electronic trading—demonstrates resilience that should serve it well in future challenges and opportunities.

Monitor COMEX's continuing evolution through real-time inventory tracking, positioning analysis, and delivery monitoring in the SilverOfTruth app — available on the App Store for comprehensive precious metals market intelligence.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, investment, or trading advice. Past performance is not indicative of future results. Always conduct your own research and consult with a qualified financial advisor before making investment decisions. SilverOfTruth provides market data and analysis tools — it does not provide personalized financial advice.