Indonesia Nickel Cuts Impact: Palladium & Global Metals Rally

Indonesia's announcement of significant nickel production cuts at several major mining operations has sent shockwaves through global metals markets, with palladium emerging as a key beneficiary. The world's largest nickel producer's decision to reduce output by an estimated 15-20% has triggered supply chain concerns that extend far beyond nickel itself, creating ripple effects across platinum group metals (PGMs) and the broader precious metals complex.

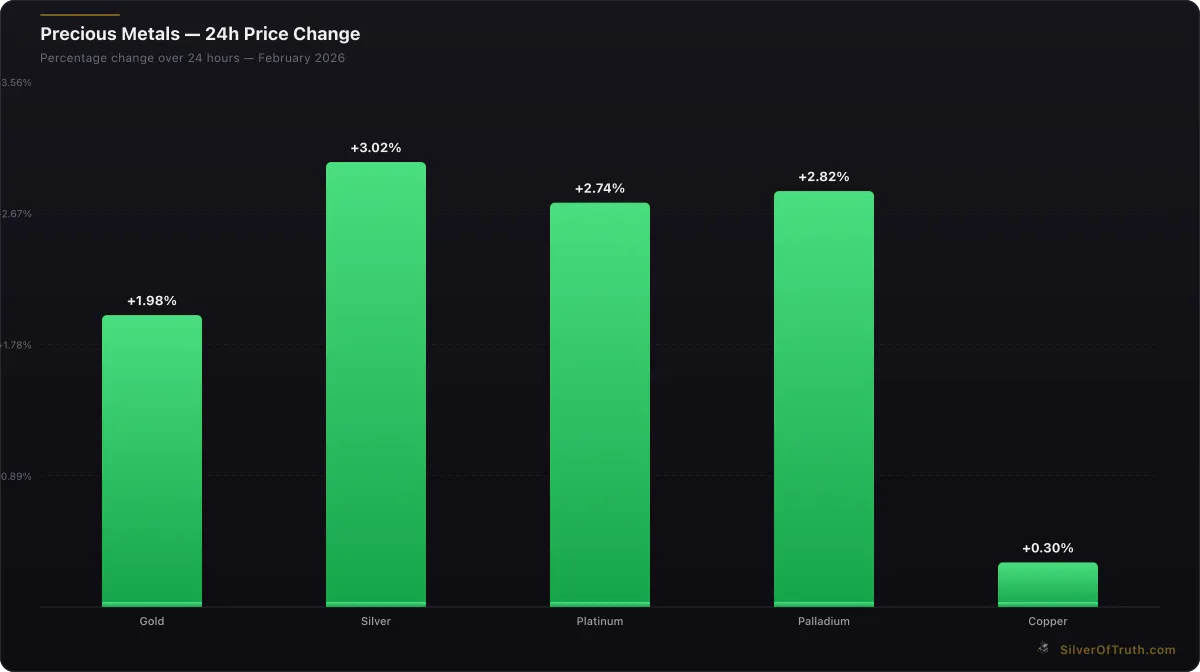

As of February 12, 2026, palladium trades at $1,703 per ounce according to SilverOfTruth data, despite being down 2.24% on the day. This recent volatility masks the metal's underlying strength as markets digest the implications of reduced Indonesian nickel supply on global industrial demand patterns. The interconnected nature of industrial metals markets means that supply disruptions in one critical metal often cascade across the entire complex.

The Indonesia Nickel Context and Global Supply Chain Impact

Indonesia controls approximately 35% of global nickel production, making it the world's dominant supplier of this critical battery metal. The country's nickel mining operations, primarily located in Sulawesi and other eastern islands, have been operating at maximum capacity to meet surging demand from the electric vehicle (EV) battery sector and stainless steel production.

Recent reports indicate that PT Vale Indonesia and other major operators have announced temporary production cuts citing environmental compliance requirements and infrastructure constraints. These cuts, estimated at 200,000-300,000 tons annually, represent roughly 8-12% of global nickel supply according to the International Nickel Study Group.

24-hour precious metals price changes. Source: SilverOfTruth, February 2026

The timing of these Indonesia nickel cuts coincides with already tight global metals markets. London Metal Exchange nickel inventories have fallen 45% over the past six months, while Chinese nickel sulfate premiums have surged to multi-year highs. This supply tightness creates a supportive backdrop for substitute metals and complementary industrial materials.

Shanghai Futures Exchange data shows nickel prices have rallied 18% since the Indonesian announcements, with ripple effects spreading to other base metals. Copper, which often trades in tandem with industrial demand patterns, has shown resilience at $5.97 per pound, up marginally according to current SilverOfTruth pricing data.

Palladium Price Surge: Industrial Demand Substitution Effects

The connection between Indonesia nickel cuts and palladium's price action lies in the complex web of industrial metal substitution and demand shifting. Palladium, primarily used in automotive catalytic converters, benefits from several key dynamics triggered by nickel supply constraints.

First, reduced nickel availability for stainless steel production increases demand for alternative alloys that often incorporate platinum group metals. Industrial users facing nickel shortages may substitute with palladium-enhanced alloys in certain applications, particularly in chemical processing equipment and high-temperature industrial components.

Second, the electric vehicle supply chain disruption caused by nickel shortages may paradoxically boost traditional automotive demand. If EV battery production faces constraints due to nickel availability, internal combustion engine vehicle production may maintain higher levels than previously projected, sustaining catalytic converter demand and palladium consumption.

Current NYMEX palladium positioning data from the CFTC's latest Commitment of Traders report shows commercial hedgers (typically producers and industrial users) maintaining net short positions of approximately 12,000 contracts, while managed money funds hold net long positions of 8,500 contracts. This positioning suggests ongoing industrial demand concerns are being hedged by end-users, while financial speculators remain moderately bullish on supply fundamentals.

South African palladium mine production, which accounts for roughly 40% of global supply, has shown no signs of increasing output to offset potential demand shifts. Anglo American Platinum and Sibanye-Stillwater have both reported stable production guidance for 2026, meaning any demand increases from Indonesia nickel cuts-related substitution would need to be met from existing inventory or recycled material.

Global Metals Demand Patterns and Cross-Metal Dynamics

The Indonesia nickel cuts illuminate the interconnected nature of global metals demand, with implications extending across the precious metals complex. Current market data reveals these cross-metal relationships in action.

Gold, trading at $5,091 per ounce and down 0.14% according to SilverOfTruth data, has shown resilience despite broader industrial metal volatility. However, gold's role as an inflation hedge becomes more relevant as supply chain disruptions potentially drive input costs higher across manufacturing sectors. The World Gold Council's latest quarterly report indicates central bank gold purchases remain robust at 183 tons in Q4 2025, providing underlying support even as industrial demand dynamics shift.

Silver, at $82.83 per ounce and down 1.30% on the day, faces a more complex situation. As both a precious and industrial metal, silver benefits from the same substitution dynamics affecting palladium, but also faces headwinds from potential economic slowdown concerns if metals supply constraints crimp manufacturing activity. The Silver Institute's preliminary 2026 demand forecast shows industrial silver consumption at 540 million ounces, with electronics and automotive sectors representing key demand drivers that could be impacted by broader supply chain disruptions.

To understand how inventory dynamics play into these market movements, our comprehensive guide to COMEX inventory provides detailed analysis of how physical supply levels influence precious metals pricing. Current COMEX silver inventory shows 381.6 million ounces total, with a concerning coverage ratio of just 53.3% according to SilverOfTruth data, indicating potential supply stress if industrial demand accelerates due to substitution effects.

The current gold-to-silver ratio at 61.47 reflects this relative positioning, with silver's industrial exposure creating both opportunities and risks from the Indonesia nickel cuts scenario. Historical analysis shows that during periods of industrial metal supply stress, silver often outperforms gold as investors position for increased industrial demand and supply chain premium capture.

Mining Sector Implications and Investment Opportunities

Indonesia's nickel production cuts create significant implications for the global mining sector, with ripple effects extending to precious metals miners and related investment opportunities. Companies with diversified portfolios of industrial and precious metals are particularly well-positioned to benefit from these supply-demand imbalances.

First Quantum Minerals, with operations spanning copper, nickel, and gold, exemplifies the type of diversified exposure that benefits from cross-metal substitution effects. The company's Sentinel copper mine in Zambia and nickel operations in Finland position it to capture pricing strength across multiple metals affected by Indonesian supply constraints.

For precious metals-focused companies, the opportunity lies in increased industrial demand and potential margin expansion. Wheaton Precious Metals, with its streaming model across gold, silver, and palladium, benefits from higher palladium prices without operational exposure to supply disruptions. The company's Q4 2025 production report showed palladium attributable production of 75,000 ounces, with cash costs of $285 per ounce providing substantial margins at current pricing levels.

Our detailed analysis in how to evaluate mining stocks provides frameworks for assessing which companies are best positioned to benefit from these supply chain disruptions. Key metrics include all-in sustaining costs (AISC), reserve life, and geographic diversification across multiple metals and jurisdictions.

Junior mining companies with palladium exposure have shown particular strength. Palladium One Mining, Generation Mining, and New Age Metals have all seen increased investor interest as market participants position for sustained PGM strength. However, these smaller companies carry higher execution risks and should be evaluated carefully within the context of overall supply-demand fundamentals.

The broader mining equity complex, as measured by the VanEck Gold Miners ETF (GDX) and Global X Silver Miners ETF (SIL), has shown mixed performance as investors weigh positive commodity price impacts against potential cost inflation from supply chain disruptions. Energy costs, steel prices for equipment, and labor availability all face potential pressure from the same supply chain constraints driving metals prices higher.

Federal Reserve Policy and Macro Economic Context

The Indonesia nickel cuts occur within a complex macroeconomic environment that amplifies their potential impact on precious metals markets. Recent Federal Reserve communications have emphasized data-dependent policy approaches, with particular attention to supply chain inflationary pressures.

As detailed in our analysis of how Federal Reserve job revisions could ignite a precious metals rally, recent labor market data revisions have created uncertainty about the pace of monetary policy normalization. Supply chain disruptions from Indonesia nickel cuts add another layer of complexity to the Fed's inflation outlook.

Core PCE inflation data for January 2026, released last week, showed a 0.3% month-over-month increase, with goods inflation contributing 0.15 percentage points. Analysts project that sustained metals supply chain disruptions could add an additional 0.05-0.10 percentage points to goods inflation over the next two quarters, potentially influencing Fed policy stance.

Current fed funds futures pricing implies a 65% probability of a 25 basis point rate cut by mid-2026, down from 85% prior to the Indonesian supply disruption news. Higher metals prices and associated inflation concerns have reduced market expectations for aggressive Fed easing, creating a more complex backdrop for precious metals performance.

Real interest rates, calculated as nominal Treasury yields minus inflation expectations, remain a key driver of gold performance. Ten-year Treasury yields at 3.85% versus 10-year TIPS breakeven inflation rates of 2.45% yield real rates of approximately 1.40%. If metals supply chain disruptions drive inflation expectations higher while nominal yields remain constrained by growth concerns, real rates could compress, providing additional support for gold and silver.

The dollar index (DXY) at 102.5 reflects this complex macro environment, with metals supply chain strength supporting commodity currencies while Fed policy uncertainty creates dollar volatility. A weaker dollar would provide additional tailwinds for dollar-denominated metals prices, amplifying the effects of fundamental supply-demand improvements.

Technical Analysis and Market Structure Considerations

From a technical perspective, palladium's price action around $1,703 per ounce represents a critical juncture for the metal's longer-term trajectory. The recent 2.24% daily decline on February 12 occurred within the context of a broader consolidation pattern that has characterized palladium trading since early 2026.

Key resistance levels for palladium lie at $1,750 and $1,825 per ounce, representing the 50-day and 200-day moving averages respectively. A sustained break above $1,750 would likely trigger algorithmic buying programs and create momentum for a test of the $1,900 level last seen in late 2025.

Support levels are established at $1,650 and $1,575 per ounce, with the latter representing a 61.8% Fibonacci retracement of the rally from December 2025 lows. Current positioning data suggests that any decline toward these support levels would likely attract fresh buying interest from industrial users seeking price hedges.

The term structure of palladium futures provides additional insight into market expectations. Current data shows the March 2026 contract trading at a $15 premium to the June 2026 contract, indicating near-term supply tightness. This backwardation structure typically supports spot prices and creates incentives for physical inventory holding.

For silver and gold, technical patterns show different characteristics reflecting their distinct fundamental drivers. Silver's decline to $82.83 brings it closer to the key $80 support level, while gold's resilience near $5,091 maintains its position above the psychologically important $5,000 threshold.

Our ongoing silver market analysis provides detailed technical perspectives on precious metals positioning and momentum indicators.

Supply Chain Resilience and Strategic Metal Considerations

The Indonesia nickel cuts highlight broader questions about supply chain resilience in critical metals markets. Government strategic metal reserves, corporate inventory policies, and alternative supply development all play crucial roles in determining how supply disruptions translate into price impacts.

The United States National Defense Stockpile includes palladium reserves of approximately 1.2 million ounces, equivalent to roughly 15% of annual U.S. consumption. However, these reserves are designated for national defense purposes and are unlikely to be released for commercial market stabilization unless supply disruptions reach crisis levels.

China's strategic metal reserves, while less transparent, are estimated to include substantial palladium holdings accumulated during the 2020-2022 period when prices reached historic highs above $3,000 per ounce. Chinese industrial demand for palladium in chemical processing and electronics manufacturing has grown 25% annually over the past three years, making any strategic reserve releases unlikely given domestic consumption requirements.

Corporate inventory management strategies have evolved significantly since the supply chain disruptions of 2020-2022. Major automotive manufacturers including Ford, General Motors, and Stellantis have increased their typical palladium inventory holdings from 30-45 days of production to 60-90 days, providing buffer against short-term supply disruptions but also reducing the responsiveness of industrial demand to price signals.

Alternative supply development faces significant time constraints. New palladium mining projects typically require 7-10 years from discovery to production, while recycling infrastructure expansion can be implemented within 2-3 years but requires sustained high prices to incentivize investment.

The Russia-South Africa duopoly in palladium production creates additional supply concentration risks beyond the immediate Indonesia nickel situation. Sanctions and political instability in Russia, combined with labor disputes and power shortages in South Africa, mean that any additional supply disruptions could have amplified effects on global palladium availability.

FAQ

How do Indonesia nickel cuts directly affect palladium prices?

Indonesia nickel cuts affect palladium through industrial substitution effects and automotive demand patterns. Reduced nickel availability for stainless steel and battery production increases demand for alternative alloys containing palladium, while potential delays in electric vehicle production may sustain traditional automotive catalytic converter demand longer than previously expected.

What is the current palladium supply-demand balance?

Global palladium supply totals approximately 6.8 million ounces annually, with South Africa producing 40% and Russia 25%. Demand from automotive catalytic converters represents 80% of consumption, with industrial applications accounting for the remainder. Current fundamentals show a modest 150,000-ounce annual deficit, which Indonesia nickel cuts-related demand increases could expand significantly.

How should investors position for ongoing metals supply chain disruptions?

Investors can consider diversified exposure through mining stocks with multi-metal portfolios, physical precious metals holdings, and ETFs focused on industrial metals. Companies like Wheaton Precious Metals provide leveraged exposure to palladium price increases, while broad-based precious metals allocations offer portfolio diversification benefits during supply chain volatility.

What are the key risk factors for sustained palladium strength?

Primary risks include economic slowdown reducing automotive demand, resolution of Indonesia nickel supply issues, increased recycling rates at higher prices, and potential strategic reserve releases by major consuming countries. Additionally, substitution of palladium with platinum in certain catalytic converter applications could limit sustained price increases.

How do Federal Reserve policies interact with metals supply chain disruptions?

Supply chain-driven inflation from metals shortages could influence Federal Reserve policy decisions, potentially slowing the pace of interest rate cuts. However, if supply disruptions contribute to economic slowdown concerns, this could accelerate policy easing. The net effect on precious metals depends on whether real interest rates rise or fall as a result of this policy interaction.

Conclusion

Indonesia's nickel production cuts represent a significant catalyst for global metals markets, with palladium emerging as a key beneficiary through complex industrial substitution effects and automotive demand dynamics. Current pricing at $1,703 per ounce reflects market recognition of these fundamental shifts, while broader precious metals markets navigate the intersection of supply chain disruptions and macroeconomic policy uncertainty.

The interconnected nature of global metals markets means that Indonesia nickel cuts create opportunities across multiple segments of the precious metals complex. From direct palladium exposure to indirect effects on gold and silver through inflation expectations and industrial demand patterns, investors have numerous ways to position for continued supply chain volatility.

Strategic positioning in diversified mining companies, physical metals allocations, and careful attention to Federal Reserve policy responses provide the best framework for navigating this evolving landscape. Track real-time palladium prices and global metals demand indicators with the SilverOfTruth app — available on the App Store for comprehensive precious metals market intelligence.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, investment, or trading advice. Past performance is not indicative of future results. Always conduct your own research and consult with a qualified financial advisor before making investment decisions. SilverOfTruth provides market data and analysis tools — it does not provide personalized financial advice.