Gold's reaction to Federal Reserve policy signals reveals a fascinating paradox: while the metal sits near record highs at $5,056 per ounce, institutional positioning data suggests investors are quietly retreating from their bullish bets. The latest CFTC Commitment of Traders report shows speculators cutting their net long positions by nearly 40,000 contracts, even as gold prices climbed 2.18% in the past 24 hours. This disconnect between price action and positioning highlights how Fed rate expectations are fundamentally reshaping gold's traditional role as a safe-haven asset.

Understanding how Federal Reserve monetary policy influences precious metals markets is crucial for modern investors. Our comprehensive Gold Investing 101 guide explores these dynamics in detail, but today's market presents unique challenges that demand immediate attention.

Quick Answer: Federal Reserve rate signals are undermining gold's traditional appeal by creating opportunity costs for non-yielding assets. While gold trades at $5,056, speculator positioning shows a -39,792 contract reduction in net longs, indicating institutional money is rotating away from precious metals despite headline price strength.

What Makes Federal Reserve Policy So Crucial for Gold?

The relationship between Fed policy and gold prices operates through multiple channels, each amplifying the metal's sensitivity to interest rate expectations. Unlike dividend-paying stocks or interest-bearing bonds, gold produces no yield, making it particularly vulnerable when opportunity costs rise.

At its core, the Fed's dual mandate of price stability and full employment directly impacts real interest rates—the nominal rate minus inflation expectations. When real rates turn positive, as they have intermittently throughout 2025 and early 2026, gold faces significant headwinds. The Federal Reserve's latest FOMC meeting minutes reveal growing confidence in the central bank's ability to maintain restrictive policy without triggering a recession, a scenario that historically pressures precious metals.

Current market dynamics showcase this sensitivity. Despite gold's 2.18% daily gain to $5,056, the broader positioning picture tells a different story. According to CFTC data, managed money traders—primarily hedge funds and commodity trading advisors—reduced their net long exposure by 26,087 contracts over the past week. This represents a significant unwinding from what was previously an extremely crowded bullish trade.

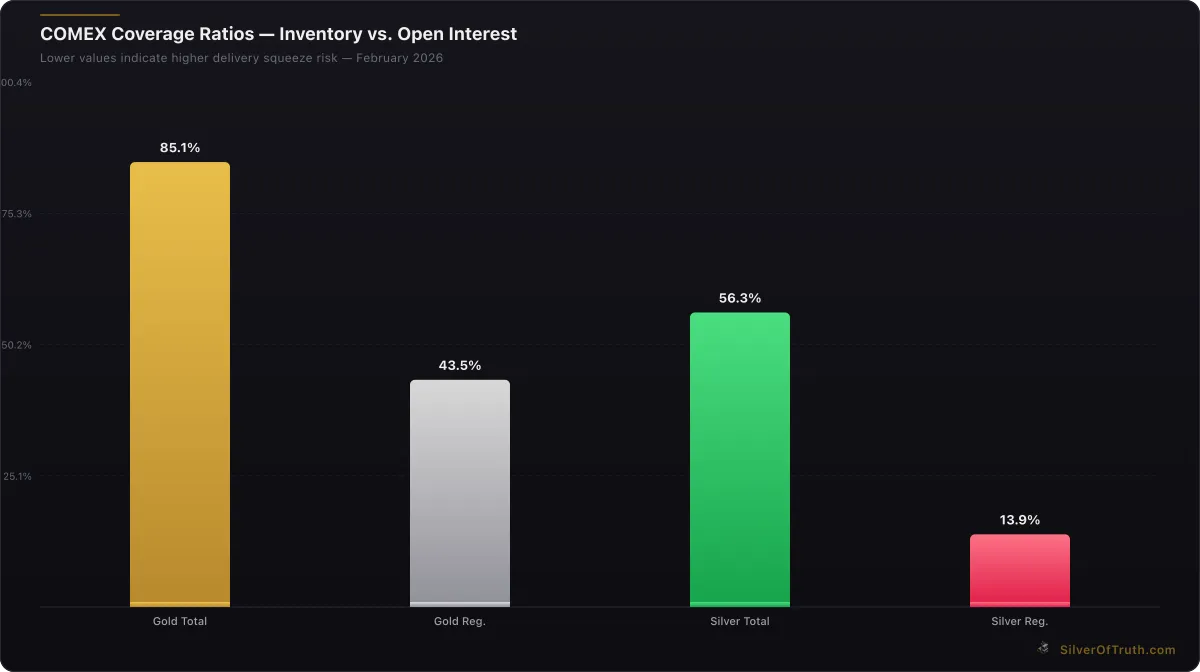

The gold coverage ratio in COMEX warehouses stands at just 84% of open interest, with registered inventory at 17.6 million ounces against 409,694 outstanding contracts. While this suggests potential supply constraints, the reality is more nuanced. Total open interest has plummeted by 78,769 contracts, indicating that rather than creating delivery pressure, investors are simply exiting positions entirely.

How Do Rising Rate Expectations Impact Gold Demand?

Rising interest rate expectations create a cascade of effects that systematically erode gold's investment appeal across multiple investor categories. The mechanism begins with opportunity cost calculations—when Treasury yields offer attractive real returns, the appeal of holding non-yielding gold diminishes proportionally.

Professional money managers have been particularly responsive to these dynamics. The latest COT data reveals that swap dealers, often representing institutional hedging activity, maintain a massive net short position of -183,144 contracts. This positioning reflects sophisticated institutions' belief that current gold prices are unsustainable given evolving monetary policy expectations.

The World Gold Council's latest data shows central bank gold purchases remained robust in 2025, but early 2026 signals suggest this trend may be moderating. When even official sector buyers—traditionally the most price-insensitive participants—begin to show restraint, it indicates fundamental shifts in gold's relative attractiveness.

Market microstructure provides additional evidence of waning demand. COMEX gold futures have seen consistently declining open interest, with the current 409,694 contracts representing a multi-week low. This isn't merely profit-taking after a bull run—it represents a structural shift in how investors view gold's risk-reward profile in a higher-rate environment.

The impact extends beyond futures markets into physical demand indicators. Although comprehensive retail data isn't yet available for February 2026, preliminary U.S. Mint sales figures suggest American Eagle gold coin purchases have moderated from their 2025 peaks, consistent with the broader theme of reduced investment demand.

Why Are Investors Rotating Away from Precious Metals?

The current investor rotation away from precious metals reflects both cyclical and structural factors that extend far beyond simple interest rate arithmetic. Portfolio managers face increasingly complex allocation decisions as multiple asset classes compete for capital in a dynamic monetary policy environment.

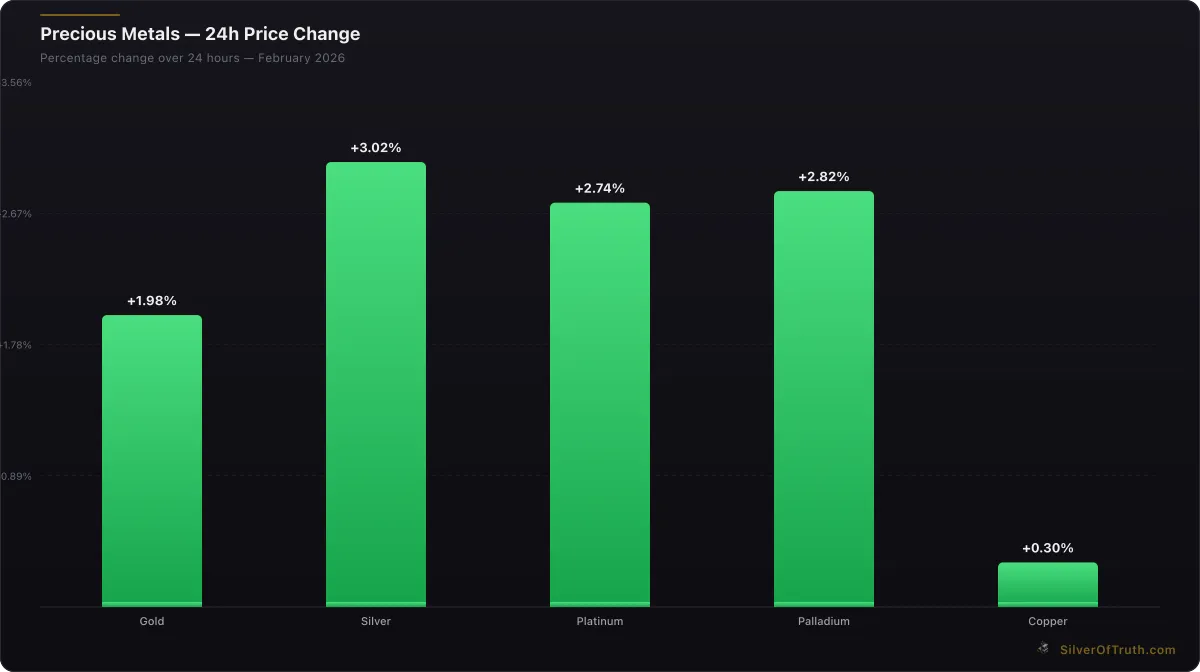

24-hour precious metals price changes. Source: SilverOfTruth, February 2026

Technology stocks, particularly those benefiting from artificial intelligence developments, have captured significant institutional attention throughout late 2025 and early 2026. The Nasdaq's performance has consistently outpaced precious metals, creating a relative performance gap that pressures fund managers focused on short-term returns. When gold struggles to keep pace with equity markets despite geopolitical tensions and inflation concerns, it signals a fundamental shift in risk perception.

Credit markets offer another compelling alternative. High-grade corporate bonds now yield attractive real returns for the first time in several years, providing income-hungry institutions with yield-generating alternatives to gold's store-of-value proposition. The LBMA's latest survey data indicates that even traditional gold bulls are diversifying into fixed-income securities.

Currency dynamics add another layer of complexity. The U.S. dollar's strength against major trading partners has created headwinds for dollar-denominated commodities, including gold. When overseas investors face currency conversion costs that exceed gold's potential returns, demand naturally weakens. This factor has been particularly pronounced in European and Asian markets, where local currency gold prices have underperformed dollar-denominated returns.

Ethereum and Bitcoin's institutional acceptance has also diverted some "digital gold" investment flows. While cryptocurrencies remain volatile and speculative, their inclusion in major institutional portfolios represents competition for gold's role as a non-correlated asset. Younger portfolio managers, in particular, show greater comfort with cryptocurrency allocations than traditional precious metals exposure.

What Does COMEX Positioning Data Reveal About Gold's Future?

COMEX positioning data provides the most granular view of institutional sentiment toward gold, and the current picture suggests significant downside risks despite recent price strength. The concentration of short positions among the top eight commercial traders—representing 53.8% of total open interest—indicates sophisticated market participants expect lower prices.

Source: SilverOfTruth COMEX data, February 2026

COMEX coverage ratios — lower values indicate higher delivery squeeze risk. Source: SilverOfTruth, February 2026

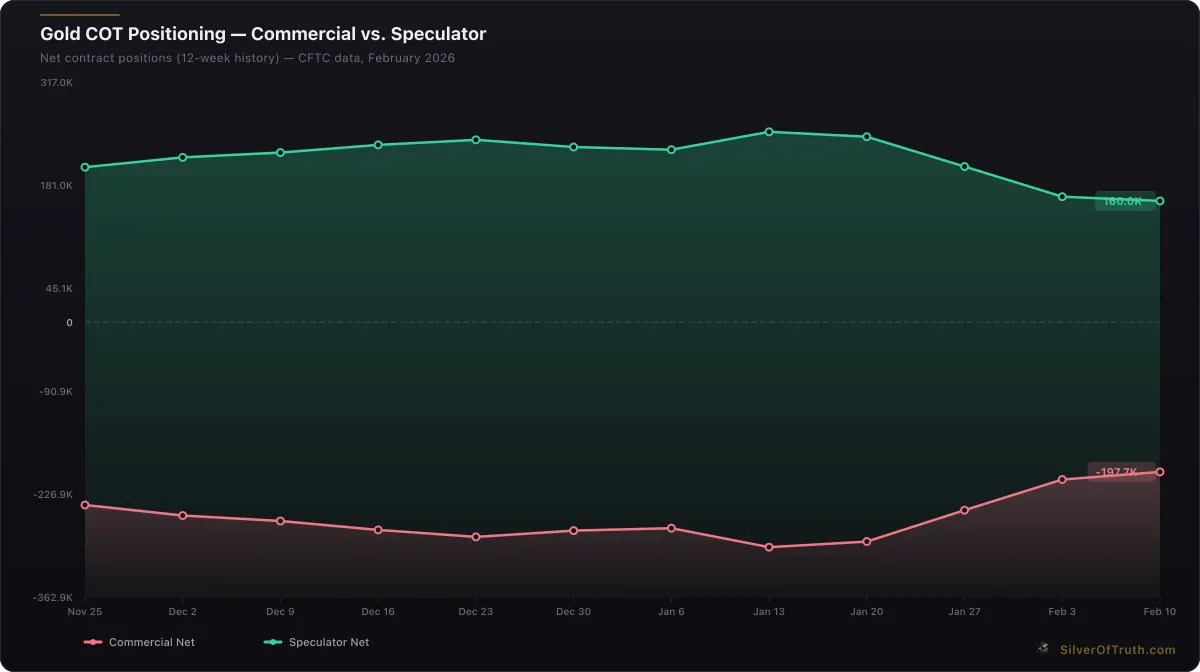

Gold COT positioning: commercial hedgers (red) vs. speculators (green). Source: CFTC via SilverOfTruth, February 2026

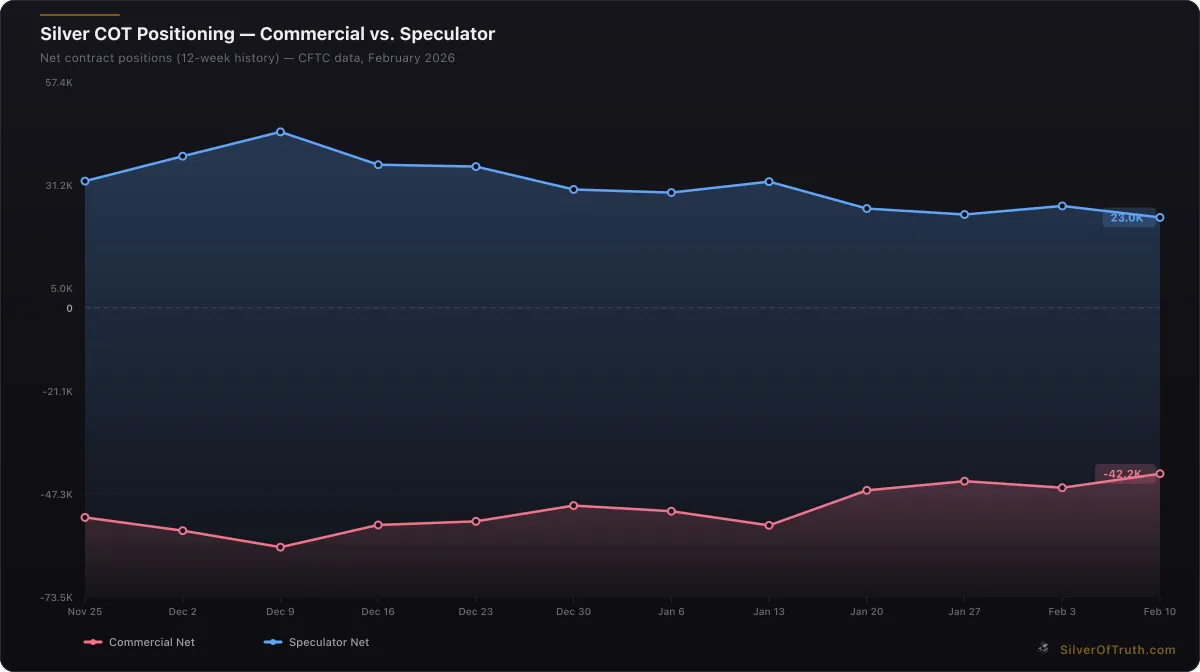

Silver COT positioning: commercial hedgers (red) vs. speculators (blue). Source: CFTC via SilverOfTruth, February 2026

Commercial traders, who typically include mining companies, refiners, and bullion dealers, maintain their heaviest short positioning in months at -207,778 net contracts. This group's hedging activities often provide reliable contrarian signals, as their operational knowledge of supply-demand fundamentals gives them informational advantages over purely financial speculators.

The decline in total open interest to 409,694 contracts—down 78,769 in just one week—represents one of the most significant position liquidations in recent memory. Unlike typical consolidation periods where open interest remains stable while prices fluctuate, this data suggests genuine disengagement from gold futures markets rather than temporary profit-taking.

Track these positioning changes live with our COMEX Inventory Tracker, which provides real-time updates on warehouse activity and open interest data that often precedes major price movements by several days or weeks.

Non-reportable traders, representing smaller speculators and individual investors, have also reduced their net long exposure to 42,174 contracts, down 715 from the previous week. While this change appears modest in absolute terms, it represents a broad-based reduction in bullish sentiment across all participant categories—a concerning sign for gold bulls.

The managed money category, which includes hedge funds and CTAs, shows the most dramatic positioning shift with a -26,087 contract reduction in net length. These traders often drive momentum in commodity markets, and their retreat suggests algorithmic trading systems may be generating sell signals based on technical and fundamental factors.

How Might Fed Policy Evolution Shape Gold's Path Forward?

Federal Reserve policy evolution through 2026 will likely determine whether gold's current weakness represents a temporary correction or the beginning of a more sustained bear market. Multiple scenarios warrant consideration based on current economic data and Fed communications.

The base case scenario assumes the Fed maintains its restrictive policy stance through at least the first half of 2026, with potential rate cuts delayed until clear evidence emerges of economic softening or inflation falling significantly below the 2% target. Under this scenario, gold faces continued pressure as real interest rates remain elevated and opportunity costs favor yielding assets.

Market-based inflation expectations, as reflected in Treasury Inflation-Protected Securities (TIPS) spreads, currently suggest investors anticipate the Fed's success in achieving its inflation mandate. When inflation expectations remain anchored near the Fed's 2% target, gold's traditional inflation hedge appeal diminishes significantly.

An alternative scenario involves economic data deteriorating more rapidly than currently anticipated, forcing the Fed into earlier and more aggressive rate cuts. Such a development would likely restore gold's appeal, but current economic indicators—including robust employment data and consumer spending—suggest this outcome remains less probable in the near term.

Geopolitical developments could also override Fed policy considerations. Military tensions in Eastern Europe and the Middle East have historically driven safe-haven demand for gold, but recent price action suggests even geopolitical premium may be insufficient to overcome monetary policy headwinds.

The wild card remains potential changes in Fed leadership or policy framework. While current Fed officials maintain hawkish stances, political pressures or unexpected economic developments could shift the central bank's approach more dramatically than markets currently anticipate.

What Should Investors Consider for Portfolio Positioning?

Investment strategy in the current environment requires careful balance between gold's long-term diversification benefits and near-term monetary policy headwinds. Professional portfolio managers increasingly view gold exposure as a tactical rather than strategic allocation, adjusting positions based on relative value considerations.

The gold-to-silver ratio at 64.98 provides one framework for precious metals positioning decisions. While this ratio remains below its long-term average, silver's greater industrial demand sensitivity makes it particularly vulnerable to economic slowdown concerns. Investors seeking precious metals exposure might consider waiting for more attractive entry points as positioning unwinds continue.

Calculate optimal allocation ratios with our Gold/Silver Ratio Calculator, which incorporates historical mean reversion patterns and current market dynamics to suggest tactical positioning adjustments.

Mining stocks present alternative exposure to precious metals trends while offering potential leverage to any eventual price recovery. However, the sector faces its own challenges from rising production costs and capital allocation concerns. Companies with strong balance sheets and low all-in sustaining costs (AISC) may outperform during any gold price weakness, as explored in our comprehensive mining stocks analysis.

International diversification within precious metals allocations may provide some protection against U.S.-specific monetary policy impacts. Gold priced in other currencies has shown different performance patterns, although currency hedging costs can offset potential benefits.

The timing of any portfolio adjustments remains crucial. Technical analysis suggests gold may find support near $4,900-$5,000 levels, but fundamental factors including Fed policy evolution will ultimately determine longer-term direction.

For comprehensive precious metals market education and strategy development, our Gold Investing 101 hub provides essential frameworks for navigating complex monetary policy environments. Understanding these dynamics becomes increasingly important as traditional correlations between assets shift in response to evolving central bank policies.

FAQ

How do Fed rate hikes specifically impact gold prices? Fed rate hikes increase the opportunity cost of holding non-yielding gold by making interest-bearing alternatives more attractive. Additionally, higher rates typically strengthen the U.S. dollar, making gold more expensive for international buyers and reducing demand.

Why is gold still rising despite bearish positioning data? Current gold price strength appears driven by external momentum and technical factors rather than fundamental demand. The disconnect between price and positioning often resolves with prices moving toward positioning trends, suggesting potential downside risk.

Should investors avoid gold entirely during Fed tightening cycles? Not necessarily. Gold can still serve portfolio diversification purposes, but investors should consider reducing tactical allocations during periods of rising real interest rates. Long-term strategic holdings may be maintained while avoiding overconcentration.

What Fed signals should gold investors monitor most closely? Key signals include FOMC meeting minutes, Fed officials' speeches regarding policy outlook, dot plot projections for future rate paths, and economic data that influences Fed decision-making such as employment and inflation reports.

How long might Fed policy continue pressuring gold? The duration depends on economic conditions and inflation trends. Historically, Fed tightening cycles last 12-24 months, but current cycle dynamics suggest extended restrictive policy is possible if inflation remains above target or economic growth stays resilient.

Sources

- Federal Reserve FOMC Meeting Minutes - https://www.federalreserve.gov/monetarypolicy/fomccalendars.htm

- CFTC Commitments of Traders Reports - https://www.cftc.gov/dea/futures/other_lf.htm

- World Gold Council Market Data - https://www.gold.org/goldhub/data

- LBMA Precious Metals Data - https://www.lbma.org.uk/prices-and-data

- U.S. Mint Production and Sales Figures - https://www.usmint.gov/about/production-sales-figures

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, investment, or trading advice. Past performance is not indicative of future results. Always conduct your own research and consult with a qualified financial advisor before making investment decisions. SilverOfTruth provides market data and analysis tools — it does not provide personalized financial advice.