Central bank gold buying reached 1,037 tons in 2024 — a 29% surge that marked the second-highest annual total on record according to World Gold Council data. This unprecedented accumulation by monetary authorities worldwide is reshaping gold markets, driving prices to new highs, and signaling a fundamental shift in how nations view monetary reserves.

With gold trading at $5,063.80 per ounce as of February 13, 2026, up 2.33% in the latest session, central bank demand continues to underpin the precious metals complex. But which countries are buying, why are they stockpiling gold at record levels, and what does this mean for the broader precious metals landscape?

This comprehensive analysis examines the central bank gold rush transforming global monetary systems, explores the geopolitical forces driving this accumulation, and reveals how these institutional purchases are creating structural support for gold and silver prices in an increasingly multipolar world.

The Central Bank Gold Rush

Central bank gold purchases have become the dominant force in precious metals markets, representing approximately 23% of total global gold demand in 2024. This institutional buying wave represents more than just portfolio diversification — it reflects a strategic shift toward monetary sovereignty and reduced dependence on dollar-denominated reserves.

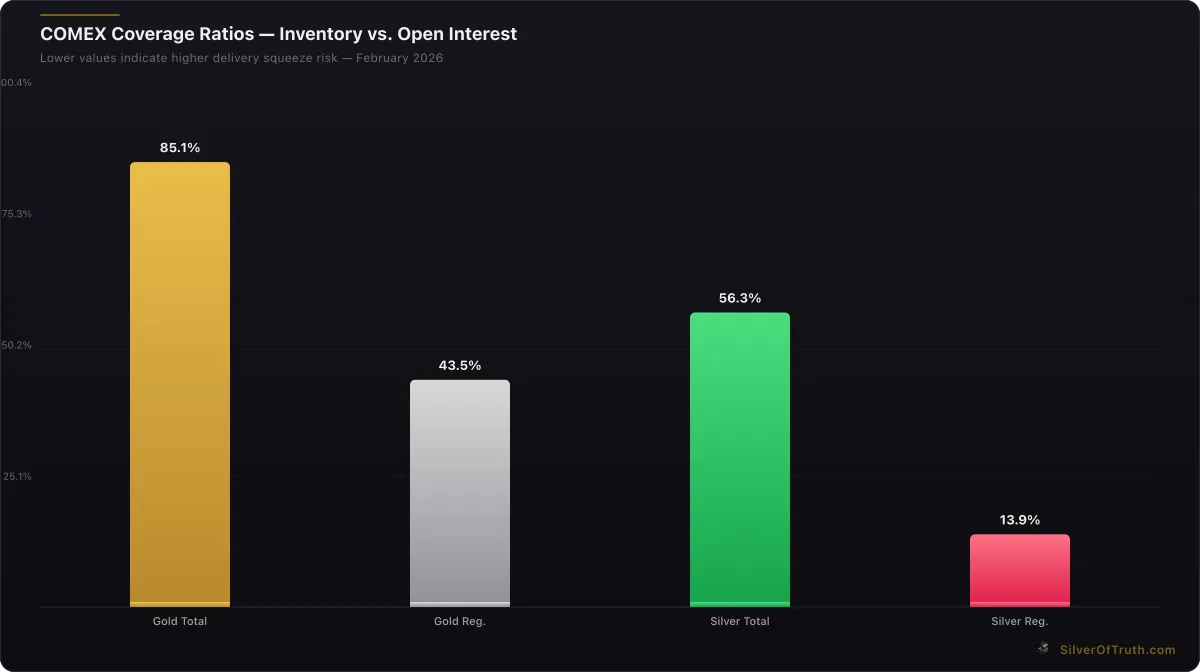

Source: SilverOfTruth COMEX data, February 2026

Record-Breaking Accumulation Patterns

The World Gold Council's latest quarterly report reveals that central bank net purchases have remained above 200 tons per quarter for the past eight consecutive quarters, an unprecedented sustained accumulation period. This consistency demonstrates that central bank buying isn't driven by short-term market opportunism, but rather represents a fundamental reallocation of monetary reserves.

Monthly central bank purchases averaged 86.4 tons throughout 2024, compared to the historical average of 42.3 tons dating back to 2010. This doubling of acquisition rates occurred despite gold prices rising 27% year-over-year, indicating price-insensitive institutional demand that prioritizes strategic reserve building over cost optimization.

Geographic Distribution of Purchases

Emerging market central banks accounted for 87% of total official sector purchases in 2024, with developed nation central banks contributing only 13%. This stark divide highlights how monetary authorities in developing economies view gold as essential infrastructure for financial independence, while Western central banks largely maintain existing gold holdings without significant expansion.

Regional breakdown shows Asia-Pacific central banks leading with 445 tons purchased (43% of total), followed by Middle East and Africa at 298 tons (29%), Eastern Europe at 201 tons (19%), and Latin America at 93 tons (9%). This geographic concentration in regions experiencing rapid economic growth and increasing geopolitical tensions underscores gold's role as a hedge against monetary and political instability.

Understanding the mechanics behind these purchases requires examining how central bank gold storage works and the complex infrastructure supporting official sector transactions. The scale of these operations has created bottlenecks in global gold logistics, contributing to periodic supply tightness that amplifies price volatility.

Top Central Bank Gold Buyers

China: The Dominant Accumulator

COMEX coverage ratios — lower values indicate higher delivery squeeze risk. Source: SilverOfTruth, February 2026

The People's Bank of China announced official purchases of 225 tons in 2024, extending an 18-month buying streak that added 435 tons to reserves since November 2022. However, market analysts estimate actual Chinese gold accumulation may exceed 500 tons annually when including unreported state purchases and off-balance-sheet acquisitions through state-owned banks.

China's official gold reserves now stand at 2,264 tons, representing only 4.9% of total foreign exchange reserves — significantly below the global average of 15.6%. This low percentage provides substantial runway for continued accumulation as China works toward reducing dollar dependency and establishing gold as a larger component of monetary reserves.

Chinese gold buying strategy focuses on market dips, with particularly heavy accumulation during Western trading hour weaknesses. This pattern suggests sophisticated timing designed to maximize tonnage acquired while minimizing market impact, allowing sustained accumulation without triggering disruptive price spikes.

Poland: Europe's Aggressive Accumulator

Poland's National Bank purchased 130 tons in 2024, the fourth consecutive year of significant accumulation that has tripled Poland's gold reserves since 2019. Governor Adam Glapiński explicitly stated the goal of reaching 20% gold allocation within total reserves, up from the current 14.2%.

Poland's buying pattern emphasizes repatriation, with 138 tons relocated from foreign vaults to domestic custody in 2024. This physical repatriation trend, mirrored by several Eastern European nations, reflects concerns about potential sanctions or asset freezes that could restrict access to overseas gold holdings during geopolitical conflicts.

The Polish central bank's transparent communication about gold strategy contrasts sharply with most central banks' secretive approach. This transparency includes regular reports on purchase timing, tonnage acquired, and storage location decisions, providing valuable insights into institutional gold accumulation methodologies.

Turkey: Strategic Diversification

Turkey's central bank added 117 tons in 2024, maintaining its position among the world's largest official sector buyers despite domestic economic challenges including 65% inflation rates. Turkey's gold purchases serve dual purposes: monetary reserve diversification and inflation hedging for an economy experiencing severe currency devaluation.

Turkish gold strategy includes accepting gold deposits from commercial banks as reserves, creating a unique mechanism that allows domestic gold holdings to count toward official reserves. This innovation has enabled Turkey to accumulate gold without depleting foreign exchange reserves needed for critical imports.

Turkey's geographical position between Europe and Asia makes its gold accumulation particularly significant for global trade flows. Turkish gold reserves provide strategic flexibility for conducting East-West trade settlements outside traditional dollar-denominated channels, supporting regional de-dollarization initiatives.

India: Consistent Long-Term Builder

The Reserve Bank of India purchased 77 tons in 2024, continuing a steady accumulation pattern focused on building gold reserves to match India's growing economic scale. India's official holdings of 822 tons represent only 8.7% of total reserves, below the global average despite India's status as the world's largest gold importing nation.

India's central bank buying strategy emphasizes domestic refining and storage, supporting local precious metals infrastructure while reducing dependence on international gold markets. This approach aligns with India's broader "Atmanirbhar Bharat" (self-reliant India) economic policy emphasizing domestic production and reduced import dependence.

Indian gold accumulation timing often coincides with domestic gold demand patterns, with central bank purchases concentrated during traditionally weak consumption periods to avoid competing with retail buyers for limited supplies.

For investors tracking these developments, understanding how to evaluate mining stocks becomes crucial as central bank demand drives exploration and production decisions across the global mining sector.

Why Central Banks Are Buying Gold

Monetary Sovereignty and Reserve Diversification

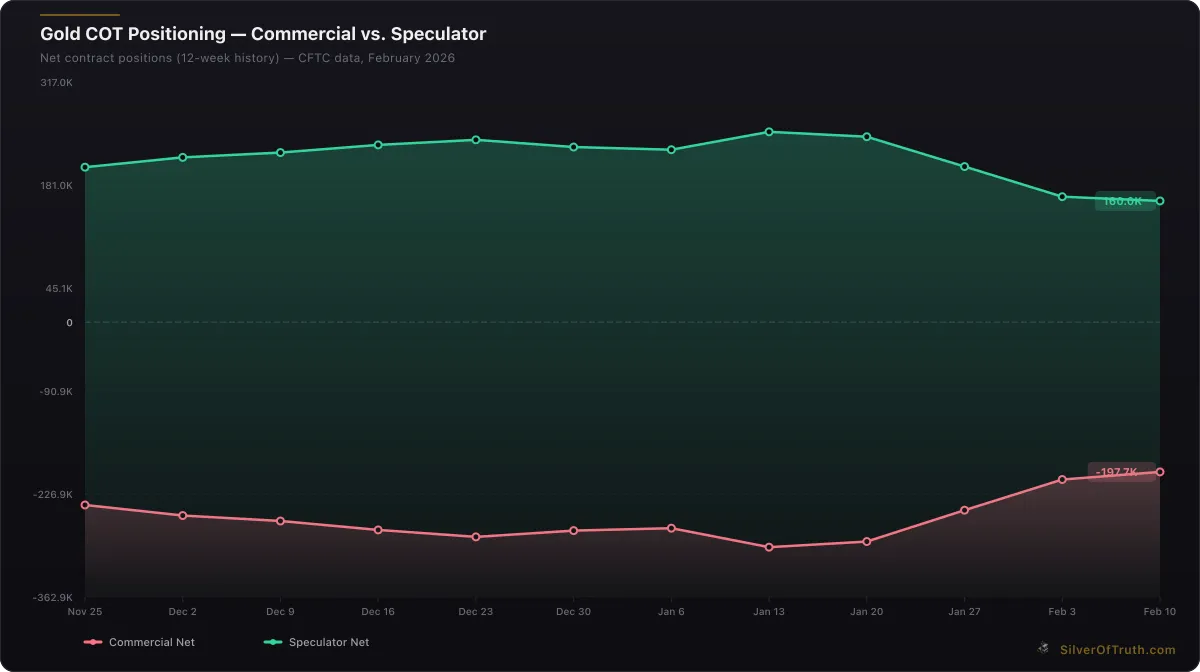

Gold COT positioning: commercial hedgers (red) vs. speculators (green). Source: CFTC via SilverOfTruth, February 2026

Central banks are fundamentally reconsidering reserve portfolio composition in response to unprecedented monetary policy interventions by major central banks since 2008. Quantitative easing programs that expanded G7 central bank balance sheets by $17 trillion created concerns about fiat currency stability, prompting diversification into non-yielding but historically stable gold reserves.

The freezing of Russian central bank reserves following the 2022 Ukraine invasion demonstrated how foreign exchange reserves can become political tools, accelerating demand for assets beyond potential sanction reach. Gold stored in domestic vaults cannot be frozen or confiscated by foreign governments, making physical gold accumulation a sovereignty protection mechanism.

Modern central banking theory increasingly recognizes gold's role as a "tier 1" asset under Basel III banking regulations, allowing banks to hold gold reserves without additional risk weighting. This regulatory framework treats gold as equivalent to cash or government bonds, removing traditional barriers to gold accumulation that previously limited central bank purchasing.

Inflation Hedging and Real Asset Allocation

Central bank gold buying serves as institutional acknowledgment that prolonged monetary accommodation may produce persistent inflation requiring real asset hedges. Gold's historical correlation with inflation expectations makes it an effective portfolio hedge against scenarios where traditional bonds lose purchasing power.

The relationship between gold and real interest rates remains strongly negative, with gold prices rising when inflation exceeds bond yields. Central banks recognize this mathematical relationship and position gold reserves as inflation insurance protecting against scenarios where monetary policy loses effectiveness.

Unlike other inflation hedges such as commodities or real estate, gold offers central banks liquidity and transportability advantages. Gold reserves can be mobilized quickly for international transactions or currency support operations without the complexity of divesting illiquid real assets.

Currency System Hedging and Geopolitical Insurance

Central bank gold accumulation reflects hedging against potential dollar system disruptions that could impair international trade settlement mechanisms. While the dollar remains the dominant reserve currency, central banks are preparing for potential multipolar monetary systems where gold could serve as an international settlement asset.

Historical analysis shows that gold accumulation accelerates during periods of currency system transition. The current environment shares characteristics with the 1970s breakdown of Bretton Woods, suggesting central banks may be positioning for another fundamental monetary system reorganization.

Understanding these dynamics requires examining the broader de-dollarization trends that are reshaping international monetary architecture and creating structural demand for alternative reserve assets like gold.

The De-Dollarization Connection

Dollar Dominance Challenges

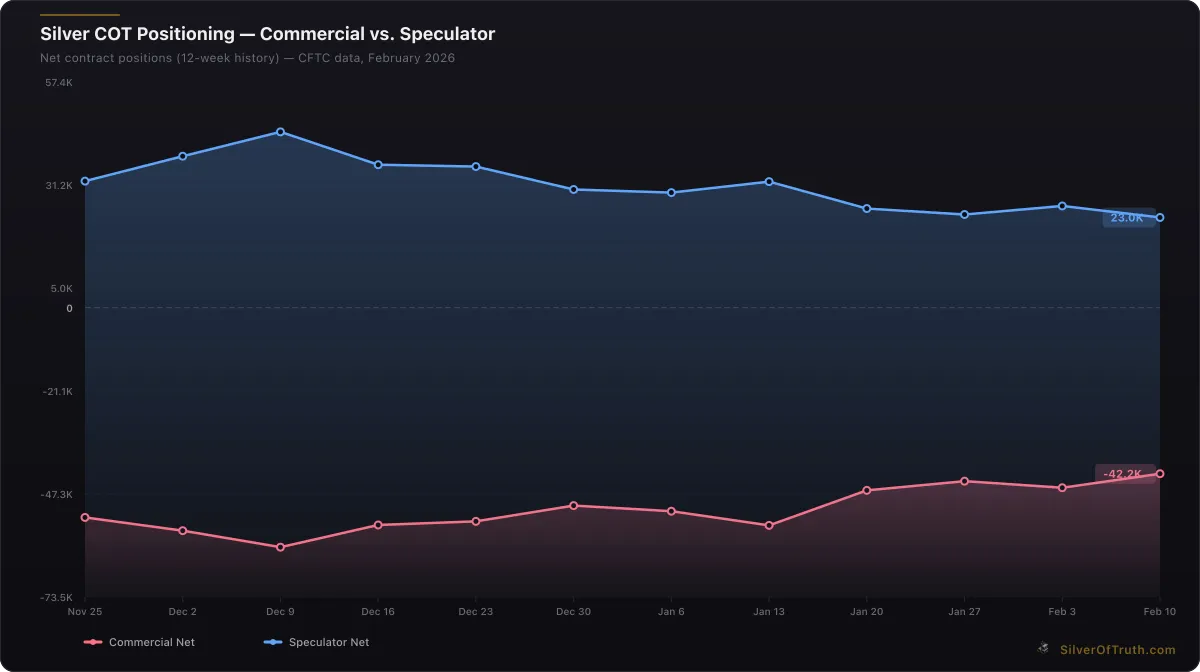

Silver COT positioning: commercial hedgers (red) vs. speculators (blue). Source: CFTC via SilverOfTruth, February 2026

The U.S. dollar's share of global foreign exchange reserves declined to 59.2% in 2024, down from 71.5% in 2000, according to International Monetary Fund data. This gradual erosion accelerated following sanctions against Russia, as central banks questioned the long-term stability of dollar-based reserve systems.

Central bank gold buying correlates strongly with de-dollarization efforts, with the highest-purchasing nations also leading bilateral trade settlement initiatives that bypass dollar clearing systems. China's yuan-denominated oil contracts, Russia's ruble-based gas sales, and India's rupee trade arrangements all coincide with aggressive gold accumulation by these nations' central banks.

The mathematical relationship is compelling: every 1% decline in dollar reserve share historically corresponds to approximately 15% increases in central bank gold demand. If current de-dollarization trends continue, extrapolating this relationship suggests central bank gold purchases could reach 1,500-2,000 tons annually by 2027-2028.

BRICS Currency Architecture

The expanded BRICS alliance (Brazil, Russia, India, China, South Africa, plus six new members) represents 45% of global population and 35% of global GDP. BRICS nations are actively developing alternative payment systems and discussing commodity-backed currency arrangements where gold could serve as a partial reserve backing.

While a formal BRICS gold standard remains speculative, member nations' combined central bank gold purchases exceeded 650 tons in 2024, representing 63% of total official sector demand. This concentration suggests coordinated strategy rather than coincidental timing, particularly given the geopolitical tensions driving BRICS expansion.

BRICS central banks are also investing heavily in domestic gold production capabilities, reducing dependence on Western mining companies and bullion markets. China, Russia, and South Africa rank among the world's largest gold producers, providing BRICS nations with potential supply chain independence for continued accumulation.

Regional Settlement Systems

Central bank gold accumulation is enabling new trade settlement mechanisms that reduce dollar dependency. The Shanghai Cooperation Organization has established gold-backed trade financing facilities, while the Eurasian Economic Union is exploring gold-denominated clearing systems for member nation transactions.

These regional systems require substantial gold reserves to provide settlement liquidity, creating additional institutional demand beyond traditional monetary reserve functions. Early estimates suggest regional settlement systems could generate 200-400 tons of additional annual gold demand as they mature and expand geographically.

Impact on Gold Prices

Structural Price Support Mechanisms

Central bank gold demand provides what analysts call "price floors" — institutional buying that emerges during market weakness, limiting downside price movements. Historical analysis shows that gold corrections rarely exceed 15-20% when central bank buying exceeds 800 tons annually, compared to 30-40% corrections during periods of minimal official sector demand.

The price-insensitive nature of central bank purchases creates market dynamics fundamentally different from speculative trading. While hedge funds and retail investors may sell during price declines, central banks often increase purchases during weakness, creating natural stabilization mechanisms that reduce volatility and support longer-term price trends.

Central bank purchasing also affects gold market microstructure by reducing available supply. When central banks remove 1,000+ tons annually from tradeable supply, it represents approximately 25% of annual mine production, creating supply tightness that amplifies price responses to incremental demand changes.

Forward Price Discovery Impact

Gold futures markets must now price in sustained central bank demand when establishing forward curves and options pricing. Market makers recognize that central bank buying provides a "bid underneath" current prices, reducing the probability of severe price collapses and supporting premium structures in options markets.

The latest COT positioning data shows commercial traders (often acting as central bank intermediaries) maintaining historically large short positions that partially reflect central bank purchasing flows. These commercial shorts represent hedging of physical gold sales to official sector buyers, creating technical support levels in futures markets.

Central bank transparency about future purchasing intentions also affects price discovery. When central banks announce multi-year accumulation targets, markets incorporate this future demand into current pricing, creating what economists call "announcement effects" that can drive prices higher before actual purchases occur.

Cross-Asset Implications

Central bank gold buying affects broader precious metals markets through portfolio rebalancing effects and supply chain competition. When institutional buyers compete for available gold refining capacity, it can create bottlenecks affecting silver and platinum processing, supporting prices across the precious metals complex.

The success of gold as a central bank reserve asset is also increasing institutional interest in silver as a potential monetary metal. Several smaller central banks have begun modest silver accumulation programs, inspired by gold's performance and seeking exposure to silver's industrial demand dynamics.

Understanding how central bank demand affects the gold/silver ratio helps investors position across precious metals markets as institutional flows influence relative price movements between different metals.

What This Means for Silver

Spillover Effects from Gold Demand

Central bank gold accumulation creates positive spillover effects for silver through several transmission mechanisms. Mining companies responding to strong gold demand often increase overall precious metals production, including silver as a byproduct of gold mining operations. This increased focus on precious metals mining benefits silver through improved infrastructure and investment flows.

Refining capacity constraints from heavy gold demand also support silver prices, as precious metals refiners often process both metals using similar facilities and expertise. When gold demand strains refining capacity, silver processing can experience delays and bottlenecks that support pricing despite lower institutional demand.

The psychological impact of central bank gold buying on retail precious metals investors cannot be understated. Retail buyers inspired by institutional accumulation often diversify across both gold and silver, creating cascading demand effects that benefit the entire precious metals complex.

Silver's Industrial vs Monetary Dynamics

Unlike gold, silver faces limited central bank demand due to storage and transport challenges associated with silver's lower value density. However, silver benefits from unique industrial demand that gold lacks, particularly in solar panel manufacturing and electric vehicle production.

Central bank gold buying indirectly supports silver by legitimizing precious metals as portfolio diversification tools for institutions. As central banks demonstrate the value of physical metal ownership, pension funds, insurance companies, and sovereign wealth funds may begin exploring silver allocation as a complement to gold holdings.

The current gold/silver ratio of 65.53 remains elevated by historical standards, suggesting potential mean reversion opportunities as precious metals gain institutional acceptance. If central bank gold accumulation triggers broader institutional precious metals adoption, silver could outperform gold during ratio normalization periods.

Investment Strategy Implications

For investors, central bank gold buying provides a fundamental backdrop supporting long-term precious metals allocation strategies. The predictable nature of official sector demand creates a foundation for portfolio construction that treats precious metals as strategic rather than tactical holdings.

Those interested in precious metals exposure should consider how to start silver stacking as a complement to gold holdings, taking advantage of silver's more accessible entry points while benefiting from the same macroeconomic forces driving central bank gold accumulation.

The infrastructure supporting central bank gold flows also creates opportunities in mining stock investments, as companies serving institutional demand often enjoy more stable, long-term customer relationships than those dependent on retail or speculative demand.

Market Outlook and Investment Implications

Projected Central Bank Demand

Forward-looking analysis suggests central bank gold purchases will remain elevated through 2026-2027, driven by ongoing geopolitical tensions and de-dollarization initiatives. Conservative estimates project annual official sector demand of 900-1,200 tons, while aggressive scenarios considering rapid BRICS expansion could see demand reach 1,500+ tons.

The pipeline of potential new buyers remains robust, with several African and Latin American central banks reportedly considering gold accumulation programs. These emerging market central banks collectively hold less than 5% of reserves in gold, compared to developed nation averages of 15-20%, providing substantial catch-up potential.

Central bank buying seasonality typically shows strength during Q4 and Q1, aligning with budget cycles and strategic planning periods. This pattern suggests continued buying pressure through early 2026, particularly if current geopolitical tensions persist or escalate.

Price Implications and Risk Factors

Central bank demand provides fundamental support for gold prices in the $4,800-$5,200 range, based on current accumulation rates and supply dynamics. However, prices could face pressure if major central banks pause purchasing programs or if developed nation central banks begin reducing holdings to fund fiscal operations.

The primary risk to central bank demand lies in potential resolution of geopolitical tensions that reduce hedging needs, though such resolutions appear unlikely given structural competition between major powers. Economic recession could also temporarily reduce purchasing as central banks prioritize currency support over reserve diversification.

For those monitoring these developments, tools like the SilverOfTruth app provide real-time tracking of precious metals flows and institutional positioning that can help investors understand how central bank activities affect broader market dynamics.

FAQ

How much gold do central banks buy each year?

Central banks purchased 1,037 tons of gold in 2024, marking the second-highest annual total on record. Monthly purchases averaged 86.4 tons, double the historical average of 42.3 tons since 2010. This represents approximately 23% of total global gold demand.

Which countries are buying the most gold?

China leads with 225 tons in official purchases (likely 500+ tons including unreported buying), followed by Poland (130 tons), Turkey (117 tons), and India (77 tons). Emerging market central banks account for 87% of total official sector purchases.

Why are central banks buying gold instead of holding dollars?

Central banks are diversifying away from dollar-denominated reserves due to concerns about currency debasement from quantitative easing, potential sanctions (as seen with Russia), and desire for monetary sovereignty. Gold provides inflation hedging and geopolitical insurance that traditional reserves cannot offer.

Does central bank gold buying affect silver prices?

Yes, through spillover effects including mining investment increases, refining capacity constraints, and psychological impacts on retail precious metals buyers. While central banks don't directly buy silver, their gold accumulation legitimizes precious metals as portfolio diversification tools.

How long will central bank gold buying continue?

Analysts expect elevated central bank demand through 2026-2027, driven by ongoing de-dollarization trends and geopolitical tensions. Conservative estimates project 900-1,200 tons annually, with potential for 1,500+ tons if BRICS expansion accelerates.

Conclusion

Central bank gold buying represents one of the most significant structural shifts in precious metals markets in decades, with 1,037 tons purchased in 2024 reflecting institutional recognition of gold's role in monetary sovereignty and portfolio diversification. The concentration of purchases among emerging market central banks, particularly China, Poland, Turkey, and India, signals a fundamental reallocation away from dollar-dependent reserve systems toward precious metals-backed monetary independence.

The de-dollarization implications extend beyond simple portfolio rebalancing, encompassing the development of alternative trade settlement systems and potential commodity-backed currencies that could reshape international monetary architecture. With BRICS nations accounting for 63% of central bank gold demand while representing 45% of global population, the geopolitical dimensions of this accumulation cannot be ignored.

For precious metals investors, central bank buying provides structural price support while creating spillover effects that benefit silver and the broader mining sector. The predictable nature of institutional demand offers a foundation for long-term strategic allocation rather than tactical trading approaches.

Track live precious metals flows and central bank positioning data in the SilverOfTruth app, available on the App Store, to stay informed about institutional trends shaping precious metals markets.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, investment, or trading advice. Past performance is not indicative of future results. Always conduct your own research and consult with a qualified financial advisor before making investment decisions. SilverOfTruth provides market data and analysis tools — it does not provide personalized financial advice.